one thing i failed to mention was that when calculating your 2 to 1 minumum ratio calculate it from the retracement level to the 100% level not the 161.8. So the numbers i have calculated only apply to getting back to the 100% level

{quote} How about this (idea borrowed from someone else): put on a position, when in profit add to your position (at an appropriate point, ideally a setup in and of itself) risking your usual risk plus the entire "paper" profits of the initial position. SL will stop out your entire position. If stopped out on this new position you lose your usual risk (1R), if the trade goes in your favour you have a much larger position on. And you can do this multiple times over the course of a single overall "position", e.g. in a swing trade. That's aggressive...

Ignored

here is a bit more details

I load first position in a falling knife style method. Wining trades typically enter near the extreme (high or low). I double up on these, where would one normally enter first load, ie when price shows signs of reversal. Trying to keep total risk constant. If trade does not behave, no additions. It works well. So I have risk 5% of account but effective position as if 10% risk. Then pray to any god that listens.

Tried to exit then reenter, never worked.

Once you load such a large position and moves away from stop I am very reluctant to move stop as now have actually opportunity to milk the position and make serious money.

This is swing trading, shortterm may be different ....

Remember that your stoploss is how you calculate your lot size according to how much money you have in your account.

Ignored

This is one possibility. Not necessarily the best btw. You're mix and matching risk managment and money management. The effectiveness of a position management must be independent of the MM. Only pips of reward per pips of risk matter. MM applies after.

with 1% risk and a smaller stop the second trade size is larger than the first and the third would be larger than the second.

Ignored

I completely agree with 2+2=4ex that each entry must be a trade on its own. I can absolutely not understand how you can have smaller and smaller SL. If you could really do this why not only enter the 3rd position? Your RR would be 4 instead of 3 (9%/3%).

I load first position in a falling knife style method. Wining trades typically enter near the extreme (high or low). I double up on these, where would one normally enter first load, ie when price shows signs of reversal. Trying to keep total risk constant. If trade does not behave, no additions. It works well. So I have risk 5% of account but effective position as if 10% risk. Then pray to any god that listens.

Ignored

The R:R and, more importantly the expectancy, only increase if it is safe to trail the SL to BE. Too early and you risk getting a loser and a BE instead of a winner. Too late and it defeats the idea of doubling the lot size. The problem is that if the 2nd entry is stopped out the R:R decreases by one unit and the result is worse than "set and forget" your trade. Because you will always have such losers from time to time, the average R:R decreases by something between 0 and 1 (the probability of this event to happen). This would not be much of a problem if I could convince myself that the probability of getting a winner is greater at the time of the add-in than it was at the time of the 1st entry. I mean the conditional probability of winning given we are ready to add-in compared to the marginal probability of the system. If this is not true, the pyramid is a hidden over leverage, if it is true this is a really powerful tool.

I hope Rag2RichesFX will post soon. This is the thread I'm the most interested in.

hi pip me up. this would only apply to this type of trading as you really dont know how far the market will retrace 1st or 3rd entry, it may retrace all the way and stop you out. you see the stop loss stays the same and the entry changes. thus 1% equals a larger calculated position not necessarily double. As in the example i posted we would have only hit the first entry.

{quote} The R:R and, more importantly the expectancy, only increase if it is safe to trail the SL to BE. Too early and you risk getting a loser and a BE instead of a winner. Too late and it defeats the idea of doubling the lot size. The problem is that if the 2nd entry is stopped out the R:R decreases by one unit and the result is worse than "set and forget" your trade. Because you will always have such losers from time to time, the average R:R decreases by something between 0 and 1 (the probability of this event to happen).

As has been discussed in other threads, pyramiding is nothing more than a collection of individual trades. Stacking another trade on top of an already existing trade does not change the dynamics of your exposure as opposed to closing original trade and opening a new trade of larger position size. In a hypothetical scenario of all things being equal, risk is proportional to reward.

Ignored

Nothing more to add. I could not explain it better. Pyramiding and Martingaling is useless - as long you use it as this type of market entry cause EVERY ENTRY is an individual position. I just tested the "myth" of pyramiding and "big" gains. Yes, it happens BUT:

Imagine this:

Entry LONG:

13000

13010

13020

13030

13040 ->avg. 13020, you trail SL to 13020 for BE. Well...the problem is that you know get statistically more stopped out as BE would be at 13000 (original entry) and guess what ?... The amount of get stopped out at BE equals ALL "big" gains... cause you lose lots of little gains (here: e.g. 13000 ->13040 return to 13010 and goes to 13100 for example. If pyramided you are at BE, else 100 TP profit with one position).

You can use pyramiding and martingaling but different to the meaning. It's called building up a position...that's what I do and if you are clever you get market edge out of it. I think 2+2=4x or PipMeUp can add more in Detail.

2 things i really love about FF:

a) OP starts a thread before he's ready and then simply leaves it hanging

b) thread replies start flowing and then random charts are posted in spite of the OP not actually laying down wot he wants to discuss

2 things i really love about FF: a) OP starts a thread before he's ready and then simply leaves it hanging b) thread replies start flowing and then random charts are posted in spite of the OP not actually laying down wot he wants to discuss

Ignored

The best part was after posting "Look to this thread sometime this weekend" (meaning last weekend), he comes back and posts "Don't think I forgot about this!! Working on it right now". That last one was over 2 days ago. He either forgot about it or his next post is going to be the longest, most comprehensive post in the history of mankind.

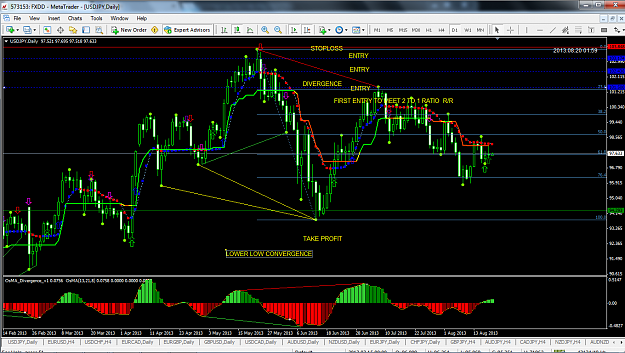

{image} this is the most recent clear example of how it works

Ignored

If feel really ashame posting this request but... may you please post a naked chart? There are lines and arrows all over the place and I'm totally unable to see where and when the entries have been open/closed. I'd like to see the price AND the time with original SL, and TP if the trade is closed.

I agree with your post right after I really depends on all the possible scenarii and their unknown probabilities. This is why it is very hard to objectively validate if it is a good idea or not.

{quote} {quote} Nothing more to add. I could not explain it better. Pyramiding and Martingaling is useless - as long you use it as this type of market entry cause EVERY ENTRY is an individual position. I just tested the "myth" of pyramiding and "big" gains. Yes, it happens BUT: Imagine this: Entry LONG: 13000 13010 13020 13030 13040 ->avg. 13020, you trail SL to 13020 for BE. Well...the problem is that you know get statistically more stopped out as BE would be at 13000 (original entry) and guess what ?... The amount of get stopped out at BE...

Ignored

Don't throw the baby with the bath water. Gridding every 10 pips is clearly wrong because the positions are all almost at the same price and the BE point follows you too tight. But buying the dips of an up trend perfectly works. What I don't know is whether it is better or worse than opening one single position. Is it better to add and wait the target or let only the 1st trade run and take profit on each subsequent inner swings?

Which one is (statistically) the best plan given that you cannot know beforehand that the trend will indeed be a trend? (if you can please start a thread!!)

{quote} The R:R and, more importantly the expectancy, only increase if it is safe to trail the SL to BE. Too early and you risk getting a loser and a BE instead of a winner. Too late and it defeats the idea of doubling the lot size. The problem is that if the 2nd entry is stopped out the R:R decreases by one unit and the result is worse than "set and forget" your trade. Because you will always have such losers from time to time, the average R:R decreases by something between 0 and 1 (the probability of this event to happen). This would not be...

Ignored

your view which is typically associated with entries that have expectation <75% at 1:1 RR. I did find 2 hq entries in life of a position and see no reason not to use both. I sure tried to load more but doesn't work for me. In my world, trading energy is finite and is only worth spending it on THE BEST setups. So when I trail winning position I make sure it is worth it my time and size according.

{quote} If feel really ashame posting this request but... may you please post a naked chart? There are lines and arrows all over the place and I'm totally unable to see where and when the entries have been open/closed. I'd like to see the price AND the time with original SL, and TP if the trade is closed. I agree with your post right after I really depends on all the possible scenarii and their unknown probabilities. This is why it is very hard to objectively validate if it is a good idea or not.

Ignored

THANKS MAN !! THIS is what I always think on lots of "systems" here. SHOW A BACKTEST result. Sit down and make at least 2 month backtest. Why always lots of people throw something in here not backtesting it ?... If I do then (backtesting) so 95% of methods here dont work. Jsut tested one more here in Forum last day...cause all thought it's "profitable". Guess what PipMeUp... W/L ration was 0.72... . They don't even test it back more than one month usually or make huge flaws (not regarding slippage, higher spreads, taking only longs / shorts (although system is not dependend on one side) and so on....

It would really help to have a "system" developer page here on FForum where you could select members only showing systems up with a backtest in FIRST POST.

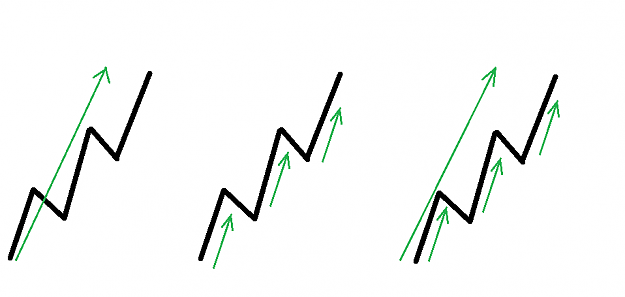

{quote} Don't throw the baby with the bath water. Gridding every 10 pips is clearly wrong because the positions are all almost at the same price and the BE point follows you too tight. But buying the dips of an up trend .... Is it better to add and wait the target or let only the 1st trade run and take profit on each subsequent inner swings? Which one is (statistically) the best plan given that you cannot know beforehand that the trend will indeed be a trend? (if you can please start a thread!!) {image}

Ignored

Thanks for the hint. Yes, you are right I always test it only on gridding in...(used different grids of pips). I will take a look on backtest using this entry method of waiting for consolidation - but it's harder to program.

Is it better to add and wait...or only 1st trade ?

Well, you or another made (yes, it was 2+2=4ex) just answered it before. It depens on expecancy on every single trade. If you take all dips, too then you just average all expectancies of all different entrys. If you only take initial position you only get this expectancy - but you know that - was this the question ?

first try went down with 2k loss. 2% of the acc.

Unfortunately today i was away cause my wife was interned for surgical operation. I ll get back with this asap.

But first things first.

take care everyone

I've got a problem with the backtests. How to backtest a strategy based on support/resistance or on trend line breakout? To find the S/R I have an algo that is barely satisfying (http://www.forexfactory.com/showthre...28#post6898628). My japanese candlesticks patterns recognizing algo is very bad. Today I cannot backtest entries like "long when a pin bar is just above a support, SL=10 pips below the pin TP at next daily S/R".

BTW there are a lot of systems in FF you can prove wrong with no backtest.

{quote} Thanks for the hint. Yes, you are right I always test it only on gridding in...(used different grids of pips).

Ignored

For the forward grid, I show in Expectancy Management that it is very probably lesser than opening one single trade "set and forget". The bigger profit only comes from the bigger risk but the expectancy decreases (aka over-leverage).

Is it better to add and wait...or only 1st trade ? Well, you or another made (yes, it was 2+2=4ex) just answered it before. It depens on expecancy on every single trade. If you take all dips, too then you just average all expectancies of all different entrys. If you only take initial position you only get this expectancy - but you know that - was this the question ?

Ignored

The problem is that this assumption that the expectancies sum up (not average) only holds if the systems aren't correlated. Adding a swing trading method within a trend following position (add-in by buying the dips) makes the two trades strongly correlated through the existance and persistance of this trend. If you join a scalping method and a daily swing method it is ok. Actually it is better than simply doubling the size of the best of the two (see Systematic trading by Mikkom).

The win/loss ratio is meaningless by itself you need to factor the R:R. See the awful "Daytrading/scalping with high leverage - my proven strategy"

I bothered backtesting the marginal probability of winning (aka win/loss ratio). To do so I generated millions of trades for each and every tick during the very nice market condition of a one month uptrend on Cable. A lot of longs did hit the huge SL dispite the up trend. Result: the w/l ratio is around 97%. Yet this system is a bleeding loser! Guess what? this thread has over one million views. Scary.

I have a question to you and in particular Rags2Riches as he mentioned a Grid / Martingale system before.

I finetuned one of these breakout strategies that was being discussed previously on these forums, but still don't have an EA as all the threads relating to the original idea are very old. So now I'm looking for a developer to finetune the Grid / Martingale idea, or just to have a look into an existing script if one is still being shared and updated...

As has been discussed in other threads, pyramiding is nothing more than a collection of individual trades. Stacking another trade on top of an already existing trade does not change the dynamics of your exposure as opposed to closing original trade and opening a new trade of larger position size. In a hypothetical scenario of all things being equal, risk is proportional to reward. Of course not all things are equal in the real market. Your success will depend on finding these inequalities (also known as inefficiencies) and then exploiting them....

Ignored

who cares what you call the trades: point is that in a well established trend it is very smart to open a new position after each meaningful retrace and the trend resuming.

with the older positions at least @ BE under the last swing, you have only 1 trade at risk, 1 @ BE and the other positions in profit should price hit the stop.

ofcourse the exit price is relative to the average entry price, but if I have 10-15 positions in a good trend, the profit can be quite large.