Hi Beyon thanks for sharing that. The problem you mention I just read about on Old dog's thread, preventing spurious regression by using non-correlated pairings:

http://www.forexfactory.com/showthre...83#post4221983

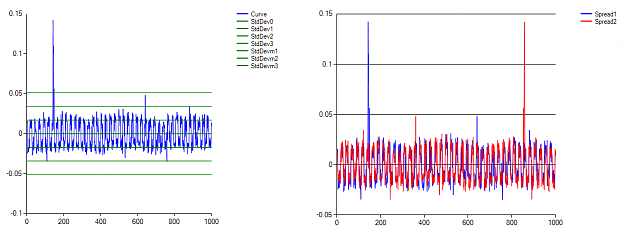

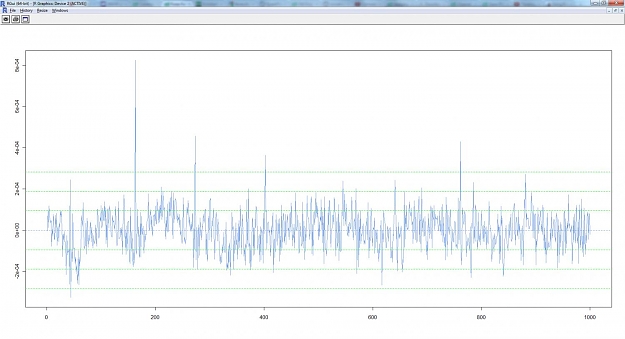

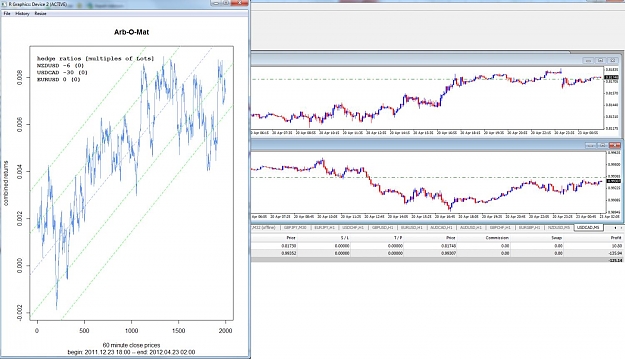

We are forming these baskets by linear regression of a set of currency pairs, either onto a straight line (in the case of the Trend-O-Mat etc) or onto another pair.

The problem is multi-colinearity.

The problem we have here is one of spurious regression when there are linear relationships among the regressors. As is well known, currency pairs are correlated [Note 1] (and there are a number of websites dedicated to calculating these correlations hourly, daily etc). If the data is correlated, then the regression can be suspect.

This is what is happening here. It is trivial to compute a basket and the associated weights. The basket will "look nice" when plotted. But it harbours a dangerous secret in its heart!!

In order to be safely tradable, the basket must also be cointegrated (so it is stationary) as I have already explained at some length.

If we have multicolinearity, we cannot believe the statistics as we have a "rubbish in, rubbish out" situation.

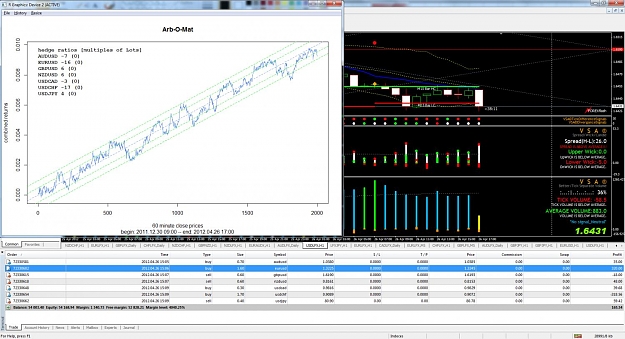

The way to solve this is only to construct baskets from pairs with low correlations. So for example, EU and GU are too close to have in the same basket. Likewise, EU and UC are too close (but negative).

I have now constructed several baskets from pairs with very low correlations (<0.3) and have worked around the problem.

BE CAREFUL!!

Very best regards,

Old Dog

http://www.forexfactory.com/showthre...83#post4221983

We are forming these baskets by linear regression of a set of currency pairs, either onto a straight line (in the case of the Trend-O-Mat etc) or onto another pair.

The problem is multi-colinearity.

The problem we have here is one of spurious regression when there are linear relationships among the regressors. As is well known, currency pairs are correlated [Note 1] (and there are a number of websites dedicated to calculating these correlations hourly, daily etc). If the data is correlated, then the regression can be suspect.

This is what is happening here. It is trivial to compute a basket and the associated weights. The basket will "look nice" when plotted. But it harbours a dangerous secret in its heart!!

In order to be safely tradable, the basket must also be cointegrated (so it is stationary) as I have already explained at some length.

If we have multicolinearity, we cannot believe the statistics as we have a "rubbish in, rubbish out" situation.

The way to solve this is only to construct baskets from pairs with low correlations. So for example, EU and GU are too close to have in the same basket. Likewise, EU and UC are too close (but negative).

I have now constructed several baskets from pairs with very low correlations (<0.3) and have worked around the problem.

BE CAREFUL!!

Very best regards,

Old Dog

DislikedI'm currently implementing a quite similar approach in JForex with Dukascopy and a R connection to Java.

My findings at today are as follows:

1) Don't integrate pairs with ultra-high correlation like say EURUSD/USDCHF. Any type of regression on one of these pairs will give a 1-1 regression. Thus the coefficients are almost the same and we really trade then EUR/CHF because we've cancelled the USD exposure out. This is useless since we pay the spread twice.

2) All combination of pairs will generate very similar spread plots for some basket...Ignored

Skype: heliosphan187