Hi,

I'd like to share my last test. Hope it is of some help.

All the best!

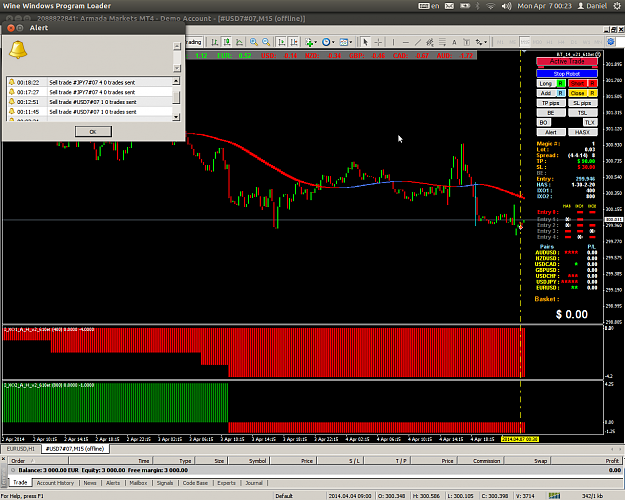

Two weeks (March 24 to April 4) test of seller9 v20: JPY7, M15, Entry 2/3, lot 0.1

Why these choices?

Best results in previous tests (EUR7, GBP6, C5, C14, JPY7 for 15 and 60 minutes).

Common main problem: for ranging periods the equity was negative

Objectives:

Testing different combinations of HAS, IXO and Exit strategies

Identify some useful filters (for ranging periods): Volumes and ADX

All combinations of ...

Has 2-6

IXO1=IXO2=300 vs. IXO1=300 and IXO2=500

Exit: has x / ts+sl 15 / ts+sl 20 / ts+sl 25

Results:

After two weeks all 4 accounts are in loss:

Exit has x -20.000

ts+sl 15 -12.000

ts+sl 20 -2.000

ts+sl 25 -1.500

Average loss / transaction is around -3 USD, except the last account (-21 USD).

Some conclusions:

No difference: Has size (2-6), IXO1=IXO2 or IXO2 larger

TS with SL seems to be better than HAS X (in condition „no ADX filter”)

A 15 pips / pair SL seems to be a little bit better than 20 or 25 (if one is looking at number of w/l)

A 20 pips / pair SL seems to be a little bit better than 15 or 25 (if one is looking at amount w/l)

If t-1 bar has a smaller volume than t bar (when the trade is taken) profit amount is still negative but a lot of bad trades are filtered. Same is true if last two bars are indicating a volume increase.

For some values of ADX, if t-1 bar has a smaller ADX than t bar (when the trade is taken) average profit becomes positive. Same is true if last two bars are indicating an increase of ADX.

Possible improuvements for the EA:

Add an option to filter for volume size and dynamic: t bar is at least x volume, t bar has larger volume than t-1 bar with x%. The same could be done considering the last three bars. Not a priority but can be tested.

Add an option to filter for ADX (with the possibility to chose the period) size and dynamic: t bar has an ADX of at least x, t bar has larger ADX than t-1 bar with x%. The same could be done considering the last three bars. I think it’s a must.

The best combination (at this stage and for the conditions mentioned above)

“HAS X + NO SL” EXIT + ENTRY filtered by ADX (ADXt > ADXt-1 by 10%) (ADX period at least 14).

See more in the files attached.

I'd like to share my last test. Hope it is of some help.

All the best!

Two weeks (March 24 to April 4) test of seller9 v20: JPY7, M15, Entry 2/3, lot 0.1

Why these choices?

Best results in previous tests (EUR7, GBP6, C5, C14, JPY7 for 15 and 60 minutes).

Common main problem: for ranging periods the equity was negative

Objectives:

Testing different combinations of HAS, IXO and Exit strategies

Identify some useful filters (for ranging periods): Volumes and ADX

All combinations of ...

Has 2-6

IXO1=IXO2=300 vs. IXO1=300 and IXO2=500

Exit: has x / ts+sl 15 / ts+sl 20 / ts+sl 25

Results:

After two weeks all 4 accounts are in loss:

Exit has x -20.000

ts+sl 15 -12.000

ts+sl 20 -2.000

ts+sl 25 -1.500

Average loss / transaction is around -3 USD, except the last account (-21 USD).

Some conclusions:

No difference: Has size (2-6), IXO1=IXO2 or IXO2 larger

TS with SL seems to be better than HAS X (in condition „no ADX filter”)

A 15 pips / pair SL seems to be a little bit better than 20 or 25 (if one is looking at number of w/l)

A 20 pips / pair SL seems to be a little bit better than 15 or 25 (if one is looking at amount w/l)

If t-1 bar has a smaller volume than t bar (when the trade is taken) profit amount is still negative but a lot of bad trades are filtered. Same is true if last two bars are indicating a volume increase.

For some values of ADX, if t-1 bar has a smaller ADX than t bar (when the trade is taken) average profit becomes positive. Same is true if last two bars are indicating an increase of ADX.

Possible improuvements for the EA:

Add an option to filter for volume size and dynamic: t bar is at least x volume, t bar has larger volume than t-1 bar with x%. The same could be done considering the last three bars. Not a priority but can be tested.

Add an option to filter for ADX (with the possibility to chose the period) size and dynamic: t bar has an ADX of at least x, t bar has larger ADX than t-1 bar with x%. The same could be done considering the last three bars. I think it’s a must.

The best combination (at this stage and for the conditions mentioned above)

“HAS X + NO SL” EXIT + ENTRY filtered by ADX (ADXt > ADXt-1 by 10%) (ADX period at least 14).

See more in the files attached.

Attached File(s)