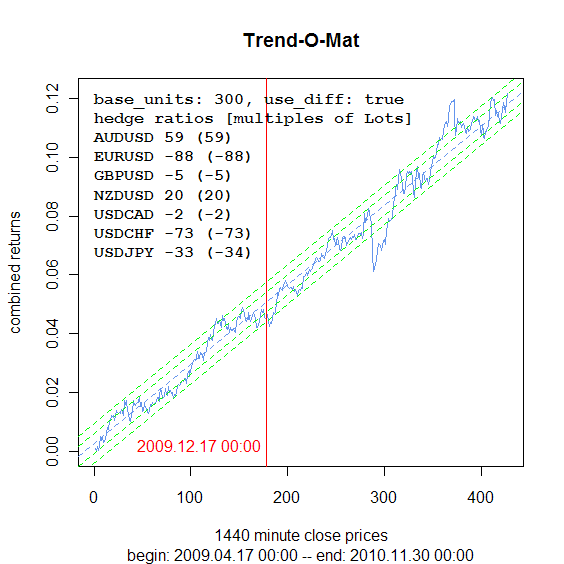

Like in many other strategies too the longer timeframes always seem to be more rewarding / easier to trade. I am currently riding the last upswing on this chart since a few days :-)

Yes, I just changed the filename and removed some experimental stuff that did not work. You should get the same results (plusminus minor differences due to different brokers quotes or candle times) with arbomat if you use the same settings and the same dates for the "back" and "now" lines.

thank you very much for the latest final version. i have good expirience within the last weeks.

what i like to see is a linegraph with the coefficients in the past. i took the algorithm in the OnOpen()-routine and put it in an indicator. it works perfectly but take so much calculationtime for every currencypair (and i only use three with 480 backcandles). because i have to calculate every coef for every candle in the past with x-back variable. Is there another way to do this directly in R with a subwindow or subgraph? with this coef-graph of every pair in the past i think you could trade better, cause you know which pair will have a floating loss.

for example i opend a basket in EURUSD (SHORT) vs. GBPUSD (SHORT) & USDCHF (LONG). USDCHF is the pair which produce the profits against the lossing positions EURUSD & GBPUSD. with the coef-graph you know this before you open your trades which one are the lossing pairs. if you know this you could trade with counter position. in my example i could trade EURUSD and GBPUSD LONG and leave USDCHF LONG. you'll see this if the coefgraph for a pair is raising or falling. if it is above or below zero.

what i like to see is a linegraph with the coefficients in the past.

Ignored

You could run it in the backtester and record the coefficients. I think trendomat contains some code for this. It creates a matrix (in R) in the init() function:

Inserted Code

if(IsTesting()){

// make a matrix that will record some things during a backtest

Ri("pairs", pairs);

RAssignStringVector(hR, "tmp", symb, pairs);

Rx("testhistory <- matrix(nrow=0, ncol=pairs*2)");

Rx("colnames(testhistory) <- c(paste('c', tmp), tmp)");

}

(the first seven columns are meant for the coefficients and the next seven columns the close prices)

and in every bar after the regression it will append a row to that matrix:

Inserted Code

if(IsTesting()){

// record some data during a backtest for later analysis

Rx("testhistory <- rbind(testhistory, c(coef(model), regressors[now+1,])) ");

}

and at the end in deinit() I save the whole R workspace image:

Inserted Code

if (IsTesting()){

Rx("save.image("" + SNAPSHOTS + "arbomat.R")");

}

(SNAPSHOTS is a folder name followed by /)

Then I run it in the backtester and after the backtest is completed I have a file arbomat.R in this folder. I start an interactive R session and

load("c:/some/folder/arbomat.R")

and then I have the exact state of the entire R workspace with all variables as it was at the end of the backtest and can explore it interactively and make plots from the columns of the testhistory matrix etc.

---

MT4 indicators are a bit tricky because they do not allow long running tasks in start() without entirely freezing MT4 (they are run in the GUI thread), you would have to split it across several calls to start() and also make use of RExecuteAsync() and then call RIsBusy() on every new tick to wait until you can continue. Since you can call RExecuteAsync() only once (and then have to wait again) you would call an R function with it that does a whole bunch of things. You would first Rx("source()") a separate R script that you wrote that defines this function and then call it with RExecuteAsync().

This is very complicated and makes the code incredibly difficult to understand (an example is given in the mt4R thread (the autoregressive indicator)) and this is the reason I made the whole thing an EA where I do not have to care about how long a task runs. An EA (and also a script) cannot freeze the GUI, it runs in its own thread that can run uninterrupted as long as I need it.

Please leave this autocorr EA out of this thread, its an entirely different thing and it is not meant to be used for trading at all. It is meant to be an interesting curiosity, a textbook example for overfitting at its best, overfitting in its purest form, free of any ballast, not more and not less.

Hi 7bit

Thank you for your good work.

are the errors from the new Arbomat already fixed?

(Http://www.forexfactory.com/attachme...hmentid=588211)

when will you make it to the forum?

what is different about the new Arbomat?

are the errors from the new Arbomat already fixed?

Ignored

The versions on my website are the currrent versions and I use then myself currently. They contain no errors (other than maybe the fact that the whole approach of using a linear regression and hoping for useful results might be flawed).

I am still hoping that someone else (who is more experienced in R and in statistics than me) will take the existing code and replace the simple regression with something else or otherwise enhance the script and publish the modified version here. I am doing some experiments myself but have nothing ready for publishing yet.

I wrote mt4R and these (example) EAs to lower the initial barrier and make it as easy as possible for people to quickly produce some working code that involves the usage of R and all its possibilities. I hope that I will not remain the only one who ever tries to write (and publish) some own code using the mt4R library.

I'm trying to find a whole method. From DOLS regression, using ERS unit roots tests instead of ADF, ...

I want to test by using log of prices and I have to test a method a saw in a technical paper about a method for testing the stationarity of the resulting serie by using a method not based on asymptotically based test (like ADF). A few things that takes a lot of time because it's long reading all this technical stuff and taking into account that I ended my Computer Science degree at college a few years ago so I have to "refresh" and wide a little bit my statistical concepts.

Anyway 7bit, thank you very much for your effort in developing this great R/MT4 stuff and for make this thread possible. You know you can count with me.

The versions on my website are the currrent versions and I use then myself currently. They contain no errors (other than maybe the fact that the whole approach of using a linear regression and hoping for useful results might be flawed).

I am still hoping that someone else (who is more experienced in R and in statistics than me) will take the existing code and replace the simple regression with something else or otherwise enhance the script and publish the modified version here. I am doing some experiments myself but have nothing ready for...

Been giving this thread a brief glance and appreciate the effort you've put in.

However I was just wondering if you've ran any cointegration tests on these actual pairs i.e. Johansen test. Because from a logical or economics stand point I don't see how such a large basket will all contain cointegration relationships. I guess you could argue that the world market is inter-related etc. but for it to be statistical significant seems too far fetched.

So by developing a linear combination of currency pairs I feel this is very prone to data-mining bias unless we have a good explanation for this connection.

Instead why not start from more logically sound cointegration relationships such as EURCHF and AUDNZD and build your portfolio and ideas from there. Since it is unlikely we could trade a simple AUDNZD cointegration idea since most people would recognise it as well.

Sorry if this all seems very critical but I just thought I'd give my $0.2 on this idea in case we start trading on spurious correlations etc.

Anyways this is an interest idea and I intend to help where I can but right now I am in the middle of a another project. However ff you haven't run any cointegration tests I could try and do so but it may have to be on excel as I am not familiar with R and have limited programming skills for MT4.

Hello 7bits,

I went over your thread and examples over the WK-E and this is really interesting work you have shared.

I will start using your mt4R to design a equity curve in-sample/out-sample/live-sample analysis so as to monitore the evolution of backtested systems and eventually quickly detect discrepencies in performance due to a change in data behavior (between optimization of an EA on a backtested period and live experience).

If this is successful (as it shouldn't be too hard), I will look at your "co-integrated basket" and see if I can contribute.

As well, this R integration could be of great help to any grid strategies based on real statstitics ;-)

Thx for your work.

X.

PS: I believe a great % of traders are in need of strong statistics to some extent. Thus more and more ppl should come to your thread (at least the quant ;-) ) ... we just need time to stumble upon it.

I wrote mt4R and these (example) EAs to lower the initial barrier and make it as easy as possible for people to quickly produce some working code that involves the usage of R and all its possibilities. I hope that I will not remain the only one who ever tries to write (and publish) some own code using the mt4R library.

However I was just wondering if you've ran any cointegration tests on these actual pairs i.e. Johansen test.

Ignored

No, not yet, but this is next on my list. Currently I just visually inspect the resulting basket (moving the time window around and watching the out-of-sample behavior) and decide whether I want to trade it.

These cointegration tests are good for finding pairs when I want to test a huge number of possible combinations in an unsupervised way but I believe they should not replace a visual inspection and replace the judgment of a trader.

For example it is always said that the residuals should not have any autocorrelation anymore (durbin watson), otherwise the regression was "wrong" but I don't have any problem trading something that is strongly autocorelated. If for example (hypothetically) the result were the superposition of a perfect sine wave and a linear trend it would fail all these tests but I would *happily* trade it until the end of all days and stop searching for anything else anymore.

Quote

Disliked

Because from a logical or economics stand point I don't see how such a large basket will all contain cointegration relationships. I guess you could argue that the world market is inter-related etc. but for it to be statistical significant seems too far fetched.

I believe they are *strongly* interrelated. Running a regression on the returns (as opposed to the absolute values) shows strong significant and constant coefficients between almost *all* pairs, so my conclusion is that also the absolute values are related to some degree (or keep the same relation at least long enough to make one or two trades, after which I make a new regression until I find something promising again).

Of course it is true that the more pairs I include the more likely it is that I will find nonsense regressions but I have the impression (I cannot (yet) prove it) that the results are far better than one would expect from such an approach and there is much less randomness than is commonly thought and a considerable amount of the *same* bulls and bears chasing each other through only these seven major currencies and *never* leave them!

(or keep the same relation at least long enough to make one or two trades, after which I make a new regression until I find something promising again).

Ignored

It agree. Coefficients all time adapt.

The main thing is a hypothesis: Laws of the market change not quickly.

The basket should be made, using laws of the market.

But regress use is an incorrect way since regress isn't equal in rights to the members.

It's what I've been using and is simple enough so I ran it (Johansen test) on daily AUD and NZD for 2000-2010 and it fails to show any signs of cointegration up to a lag of 20.

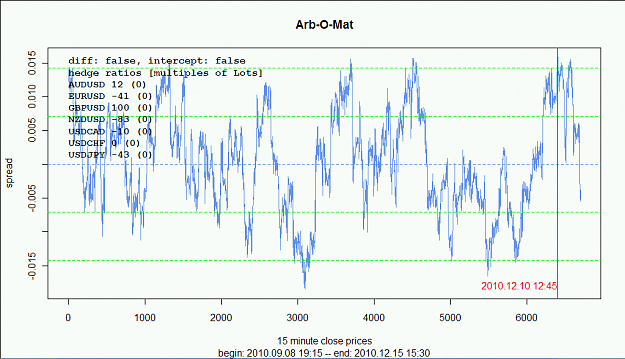

sold at the red line near 2*sd and just closed it with a nice profit :-)

The spread curve might fail many sorts of statistical tests, but this does not mean it is not tradeable (people successfully trade all kinds of instruments for which no models and no tests exist at all).

Just yesterday began testing the your ideas and closed three baskets in profit, small, but profits. Two in the USDJPY m15 2304 bars, last one in the EURUSD m5 288 bars.

Although I still don't understand everything explained here, I would like to ask you, if possible, to draw the spread lines (or sd lines???) from the R plot in the mt4 chart that the ea is attached, with the values in the right side.