I have been forward testing a new AI system since yesterday with good results but I am seeing a consistent bias towards opening short positions instead of Long positions.

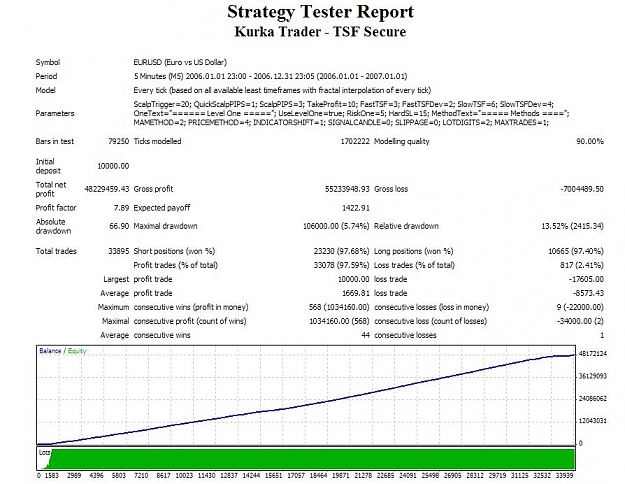

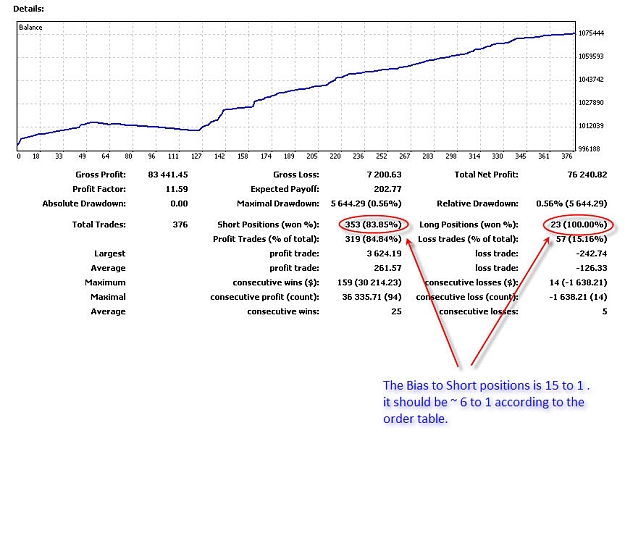

The EA creates a market netural order table with all available currency pairs (in this case 24 pairs * 8 indexes * 3to6 positions for the hedge totaling between 576 and 1152 positions) then trades these positions based on what the AI algos determine is the best solution for each available position. The order table has about a 6 to 1 ratio of short to long positions but the actual trading is about a 15 to 1 ratio (see attachment). The only reason I can think of is that the AI is calculating everything based on the bars which only represent the Bid pricing and do not include the spread.

So the question is ... how do you handle the bias towards short positions in your systems ?

Also, how would you adjust your indicators to correct this bias ? this is particularly important in oscillator type indicators...

The EA creates a market netural order table with all available currency pairs (in this case 24 pairs * 8 indexes * 3to6 positions for the hedge totaling between 576 and 1152 positions) then trades these positions based on what the AI algos determine is the best solution for each available position. The order table has about a 6 to 1 ratio of short to long positions but the actual trading is about a 15 to 1 ratio (see attachment). The only reason I can think of is that the AI is calculating everything based on the bars which only represent the Bid pricing and do not include the spread.

So the question is ... how do you handle the bias towards short positions in your systems ?

Also, how would you adjust your indicators to correct this bias ? this is particularly important in oscillator type indicators...

Attached Image (click to enlarge)

Keep it simple stoopid....