Volatility and Stops for the DayTrader con'd

Donald L. Jones, CISCO Futures, January 10, 2003

Copyright Donald L. Jones, all rights reserved

http://www.cisco-futures.com/volatilitystops.html

Volatility from Half-Hour "Meta-Profile" Bars

At CISCO we have calculated volatility from the half-hour bars in the Meta-Profile for many years. Our use of 30 minute range bars rests on the fact that the Meta-Profile is a mature methodology for describing market value. (Meta-Profile volatility is displayed in reference 4., as are volatility history tables.) Practically, we develop Meta-Profiles for other purposes, so it is a convenient database. Questions have arisen from time to time about whether a 15 or 20 minute time frame, say, might be a better descriptor. In this report, I will show you the results of a study that validates the 30 minute time frame as quite good, with the optimum time frame around 25 minutes. Also, these new calculations are divorced from the CBOT Market Profile, so that anyone with a ticker can find the volatility.

Quantitative volatilities benefit the trader by replacing the general "hmmm, I think the SP volatility is increasing" with the specific ("SP volatility on Monday 12/16/02 is 28.1, on Tuesday it is 28.1, and on Wednesday it is 37.9") (ref 5). In this example, the market was balancing on Monday, Tuesday and Wednesday (ref 5). The increase in volatility on Wednesday is a tip-off that new trading interest came into the market on Wednesday. You would be alerted to look into your trading methodology for Thursday's market. Maybe something is afoot. In fact, the close on Wednesday was 89150, Thursday closed at 88480, so the big jump in volatility gave you advance notice of a possible trading opportunity.

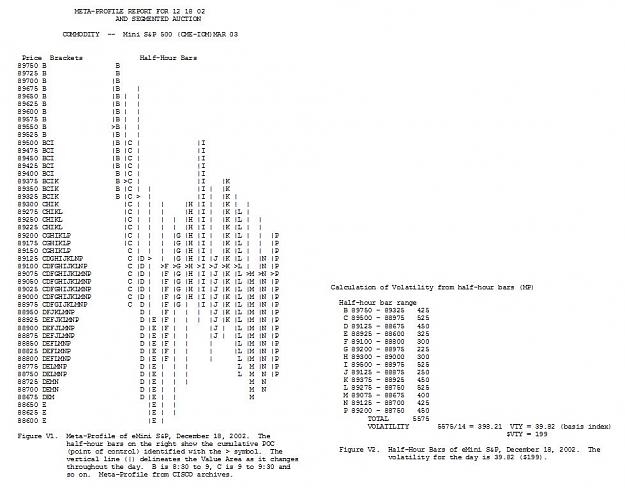

Volatility from the Meta-Profile

You can understand volatility measurement easiest with an example from a Meta-Profile and it's half hour bars. We use the eMini S&P to show that the volatility obtained for December 18 (39.82) is essentially the same as for the SP cited above (37.9). The eMini and the big SP contract differ primarily in their minimum tick size, so the volatilities should differ to some degree. The half hour bars in Figure V1 will be used to calculate the volatility in Figure V2.

Donald L. Jones, CISCO Futures, January 10, 2003

Copyright Donald L. Jones, all rights reserved

http://www.cisco-futures.com/volatilitystops.html

Volatility from Half-Hour "Meta-Profile" Bars

At CISCO we have calculated volatility from the half-hour bars in the Meta-Profile for many years. Our use of 30 minute range bars rests on the fact that the Meta-Profile is a mature methodology for describing market value. (Meta-Profile volatility is displayed in reference 4., as are volatility history tables.) Practically, we develop Meta-Profiles for other purposes, so it is a convenient database. Questions have arisen from time to time about whether a 15 or 20 minute time frame, say, might be a better descriptor. In this report, I will show you the results of a study that validates the 30 minute time frame as quite good, with the optimum time frame around 25 minutes. Also, these new calculations are divorced from the CBOT Market Profile, so that anyone with a ticker can find the volatility.

Quantitative volatilities benefit the trader by replacing the general "hmmm, I think the SP volatility is increasing" with the specific ("SP volatility on Monday 12/16/02 is 28.1, on Tuesday it is 28.1, and on Wednesday it is 37.9") (ref 5). In this example, the market was balancing on Monday, Tuesday and Wednesday (ref 5). The increase in volatility on Wednesday is a tip-off that new trading interest came into the market on Wednesday. You would be alerted to look into your trading methodology for Thursday's market. Maybe something is afoot. In fact, the close on Wednesday was 89150, Thursday closed at 88480, so the big jump in volatility gave you advance notice of a possible trading opportunity.

Volatility from the Meta-Profile

You can understand volatility measurement easiest with an example from a Meta-Profile and it's half hour bars. We use the eMini S&P to show that the volatility obtained for December 18 (39.82) is essentially the same as for the SP cited above (37.9). The eMini and the big SP contract differ primarily in their minimum tick size, so the volatilities should differ to some degree. The half hour bars in Figure V1 will be used to calculate the volatility in Figure V2.

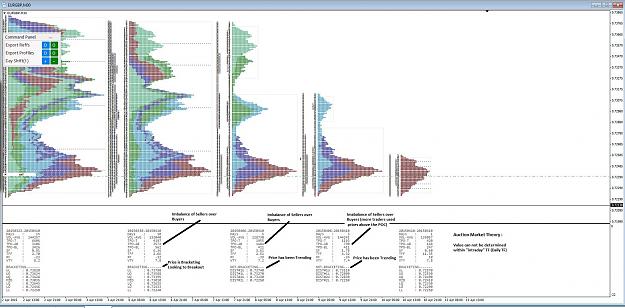

Attached Image (click to enlarge)

Markets are not efficient, rather they are effective - Jones