Unicredit FI/FX desk notes

News and Events

■ CH: 2Q GDP came in better than expected, edging up slightly to 7.5% from the previous 7.4%. This outcome reflects an earlier and stronger than expected impact from the authorities’ pro-growth measures.

■ UK: We see the unemployment rate falling 0.1pp to 6.5% in the three months to May, with employment rising 186k when compared to the prior non-overlapping three months. Jobless claims are expected to fall by another 25k in June (10:30 CET).

■ US: Industrial production likely rose a more moderate 0.3% in June, after rebounding in May. (15:15 CET).The Beige Book will also be released today (20:00 CET).

■ Fed: Janet Yellen will give her semi-annual testimony to the House (16:00 CET).

FI/FX Strategy

■ FI view: We do not see any real market mover for euro-area bond markets today and the impact from abroad should also be modest. With Janet Yellen highlighting the slowdown in the housing recovery, special attention is on today's NAHB index as well as tomorrow’s housing starts and building permits. As we expect an increase in the latter, although to a lesser extent compared with the consensus estimate, impulses from the US should be benign.

■ DE: Germany will sell EUR 4bn of 1.5% 2024. With the 10Y trading at around 1.20%, just 7bp above the prior low of June 2012 (1.127 intra-day), we are not enthusiastic. While we see a limited risk in favor of quickly accelerating yields in the short run, we have strong doubts whether current levels are sustainable and do not recommend a duration extension beyond the 5-7Y segment. On a multi-week horizon, the 10Y should ultimately steepen vs. the 2Y and 5Y, which are supported by the easy monetary policy and discussions of further monetary policy accommodation, while we expect a bear-flattening in 10-30Y over a medium-term horizon.

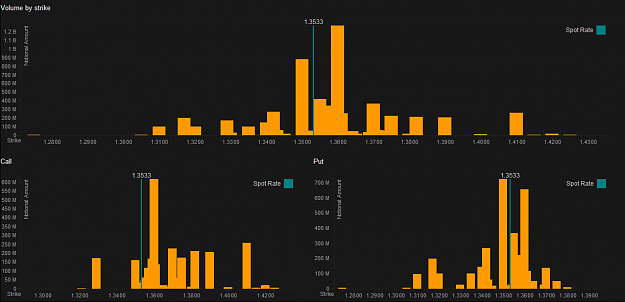

■ EUR: EUR-USD declined yesterday although Janet Yellen’s testimony did not offer any fresh news. Indeed, bids emerged close to 1.3550, thus suggesting no great market conviction to ride a further and more intense sell-off. Her address to the US House today is unlikely to offer news and slower US IP data may push EUR-USD back above 1.36.

■ GBP: Better labor data in Britain for June may offer a new lift today, but at current levels we do not see great upside potential for cable after peaks above 1.7190 yesterday, given a monetary policy scenario that is well priced in. EUR-GBP may still struggle on the edge of 0.79.

■ CAD: The BoC is expected to stay pat at 1.00% today, with the focus more on recent weaker economic data releases at home that may increase downside risks to the growth picture rather than on the recent pickup in inflation. USD-CAD is likely to extend its recent recovery towards 1.08 and above.

■ SEK: The minutes of the Riksbank’s 3 July meeting, after which the bank surprised markets with an aggressive 50bp rate cut, may offer further information on how much the bank board was split on the decision. EUR-SEK is now steadying close to 9.25 after its recent drop and current levels do not appear attractive to ride a further and profitable downward correction.

News and Events

■ CH: 2Q GDP came in better than expected, edging up slightly to 7.5% from the previous 7.4%. This outcome reflects an earlier and stronger than expected impact from the authorities’ pro-growth measures.

■ UK: We see the unemployment rate falling 0.1pp to 6.5% in the three months to May, with employment rising 186k when compared to the prior non-overlapping three months. Jobless claims are expected to fall by another 25k in June (10:30 CET).

■ US: Industrial production likely rose a more moderate 0.3% in June, after rebounding in May. (15:15 CET).The Beige Book will also be released today (20:00 CET).

■ Fed: Janet Yellen will give her semi-annual testimony to the House (16:00 CET).

FI/FX Strategy

■ FI view: We do not see any real market mover for euro-area bond markets today and the impact from abroad should also be modest. With Janet Yellen highlighting the slowdown in the housing recovery, special attention is on today's NAHB index as well as tomorrow’s housing starts and building permits. As we expect an increase in the latter, although to a lesser extent compared with the consensus estimate, impulses from the US should be benign.

■ DE: Germany will sell EUR 4bn of 1.5% 2024. With the 10Y trading at around 1.20%, just 7bp above the prior low of June 2012 (1.127 intra-day), we are not enthusiastic. While we see a limited risk in favor of quickly accelerating yields in the short run, we have strong doubts whether current levels are sustainable and do not recommend a duration extension beyond the 5-7Y segment. On a multi-week horizon, the 10Y should ultimately steepen vs. the 2Y and 5Y, which are supported by the easy monetary policy and discussions of further monetary policy accommodation, while we expect a bear-flattening in 10-30Y over a medium-term horizon.

■ EUR: EUR-USD declined yesterday although Janet Yellen’s testimony did not offer any fresh news. Indeed, bids emerged close to 1.3550, thus suggesting no great market conviction to ride a further and more intense sell-off. Her address to the US House today is unlikely to offer news and slower US IP data may push EUR-USD back above 1.36.

■ GBP: Better labor data in Britain for June may offer a new lift today, but at current levels we do not see great upside potential for cable after peaks above 1.7190 yesterday, given a monetary policy scenario that is well priced in. EUR-GBP may still struggle on the edge of 0.79.

■ CAD: The BoC is expected to stay pat at 1.00% today, with the focus more on recent weaker economic data releases at home that may increase downside risks to the growth picture rather than on the recent pickup in inflation. USD-CAD is likely to extend its recent recovery towards 1.08 and above.

■ SEK: The minutes of the Riksbank’s 3 July meeting, after which the bank surprised markets with an aggressive 50bp rate cut, may offer further information on how much the bank board was split on the decision. EUR-SEK is now steadying close to 9.25 after its recent drop and current levels do not appear attractive to ride a further and profitable downward correction.