Hi TheMaxx,

here are some changes for lot calculation: please use

coefn[i] = coef[i] / PointValuePerLot with

PointValuePerLot= MarketInfo(Symbol(),MODE_TICKVALUE) / MarketInfo(Symbol(),MODE_TICKSIZE)

for normalizing the coef's to get the basis for lot multiples. TickValue alone is not sufficient . It shall replace the division by close quotes.

Ignored

Thanks - I don't know how to add this to the current code. Could you please help?

Hi,

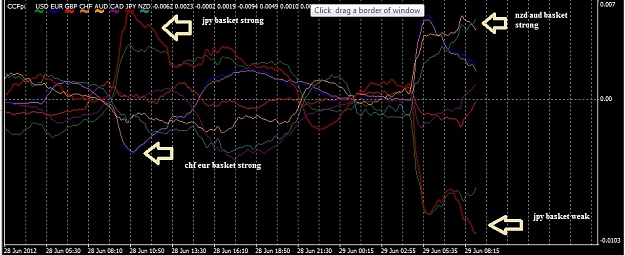

I have set up usdcad with nzdusd on H1 t/f, same as Dirtybrown is trading, I think. I realise that the Arbomat is a shifting window and it is difficult to do a visual look back. But it appears that if we are trading from the 2nd deviation line back towards the mean, then there would only be around 3 trades per 2000 bars (around 4 months for H1).

Is this correct?

Ignored

Yes, that is correct.

Also, if you set intercept to false you'll get horizontal lines rather than the angled lines on your R chart picture

sapiemas - I tried to import your code but I couldn't work out where to assign the initial value to lastpred.

I've attempted to fix the pred[0] bug in my own weird way - new EA is attached.

Ignored

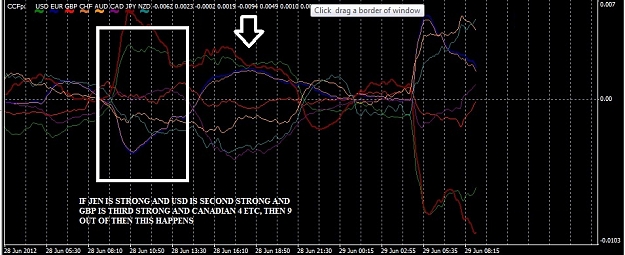

the problem about wrong values exist because not every candle of different pairs opens at the same time.

if for example you put the EA on an EUR/USD chart and take GBP/USD as the basket pair. if a new candle opens in EUR/USD does not mean that at the same time the GBP/USD candle also open. this results in false data especially if you have multiple pairs in a basket.

before the EA opens a trade you have to check if at every pair the new candle exist and then take the closeprice of the finished candle.

it is also better to use pred[1] as value because then you are safe with a finished value. pred[0] is the actual value and could change during candle development

it is also better to use pred[1] as value because then you are safe with a finished value. pred[0] is the actual value and could change during candle development

maybe you can use a relative strength ma like in ccfp indicator and code it in such a way to give weights to the wining losing basket, im giving you 2 examples with the normal ccpf and im also including the one with the relative strenth of gold, i hope this helps great idea btw

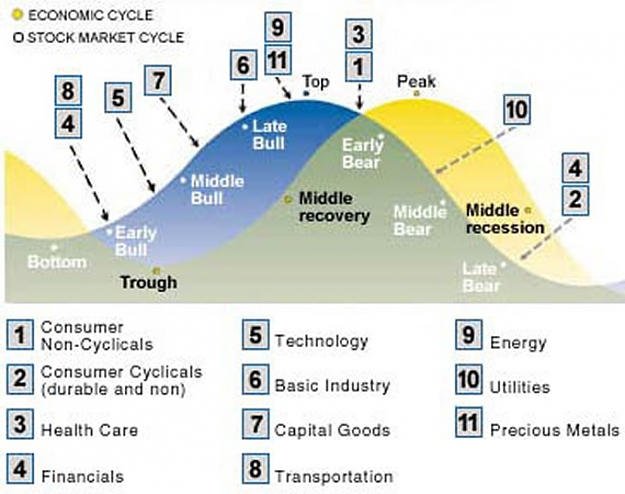

maybe what is really missing is what BETWEEN the numbers , no i just had to quote that order of chaos film , i mean maybe by using the arbomat to include usoil and ukoil as values from the loonie, using gold prices as weight of newzealand dollar and australian dollar , and as a risk/aversion ratio , i think thats all thats missing altho if you really want to get technical you can use the stock market buisness cycle, at least it would give an idea of some economies more affected by x economic factor and it can give greater weights to some

I'd be interested in collaborating on some research ... but I'm a R user (not Matlab). Any R users out there???

EZ

Ignored

perhaps using of JMULTI or Eview can be good starting point, than no need to programming at all. Afterwards model parameter can be just implemented in

MT4 or another trading platform.

perhaps using of JMULTI or Eview can be good starting point, than no need to programming at all. Afterwards model parameter can be just implemented in

MT4 or another trading platform.

Krzysztof

Ignored

Other than no need for programming, is there any analytical benefit of using JMULTI or Eviews over R? It took some time but I'm now quite comfortable using the packages in R. Are there methods in Jmulti / Eviews not available in R?

Other than no need for programming, is there any analytical benefit of using JMULTI or Eviews over R? It took some time but I'm now quite comfortable using the packages in R. Are there methods in Jmulti / Eviews not available in R?

Ignored

For sure it will save a time and decrease a risk of making programming errors, the people not familiar with Matlab or R can easily play to start with it.

There is also a lot of literature which helps to understand certain econometrics concepts using eview