Euro at Risk Despite Rising CPI as Markets Envision ECB Rate Cuts

Euro at Risk Despite Rising CPI as Markets Envision ECB Rate Cuts

By:Ilya Spivak

The euro may fall as German and Eurozone inflation data helps make the case for interest rate cuts in 2024 despite pushback from the European Central Bank

- The euro scored strong two-month gains thanks to a weak U.S. dollar and hawkish ECB.

- Incoming German and Eurozone-wide inflation data will test the currency’s resilience.

- Traders may ignore a headline CPI jump and focus on domestic weakness, hurting the euro.

The euro enjoyed its best two months in a year in November and December of 2023, rising 4.4% against the U.S. dollar.

A broadly weaker greenback seemed to contribute most of the impetus for the move. The currency slumped as markets priced in a swift interest rate cut cycle from the Federal Reserve, eroding its yield advantage.

The European Central Bank (ECB) contributed a bit of the heavy lifting. While the Fed embraced the markets’ dovish repositioning at its December conclave, ECB President Christine Lagarde and the central bank’s Governing Council pushed back on similar speculation.

Euro sent higher as the ECB tries to resist rate cut pressure

Speaking at the press conference following the Dec. 14 policy meeting, Lagarde said the central bank “should absolutely not lower our guard” in the fight against inflation, adding that officials “did not discuss rate cuts at all”. That sent the euro sailing higher to close with a gain of over 1% on that day alone.

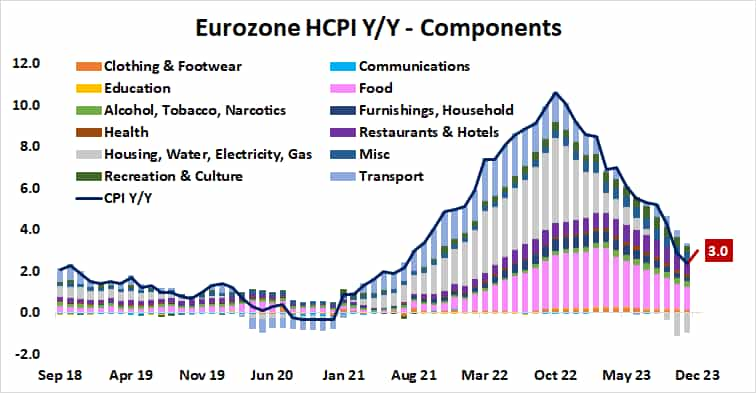

At the same time, Lagarde said the ECB expects base effects to push up inflation in December and will make for a slower disinflationary process in 2024. The markets seem to agree. Experts expect the consumer price index (CPI) measure of German price growth to have increased 3.9% year-on-year last month, up from a rate of 2.3% in November.

CPI data coming this week

Region-wide CPI statistics are due later this week are projected to follow Germany’s lead. Inflation is seen rising to 3% year-on-year in December from 2.4% in the prior month. That would mark the highest reading in three months and the largest one-month pickup since October 2022.

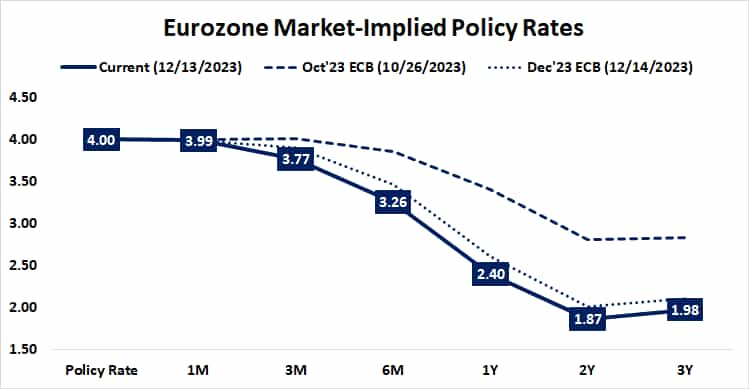

Nevertheless, the markets are dubious about the ECB’s hawkish appetite. The priced in policy path has continued to inch in a move dovish direction following December’s meeting rather than backtracking on November’s meaty adjustment. Analysts expect the first 25-basis-point (bps) cut no later than April.

Six cuts in total–amounting to 150 bps or 1.5% in rate reduction–are already reflected in market pricing. The probability of a seventh one is implied at 68%, giving it better-than-even odds and implying that traders see the path of least resistance as biased in a dovish direction.

Financial markets to the ECB: we don’t believe you

Investors’ disbelief seems rooted in the ECB’s own guidance. Back at the December ECB presser, Lagarde said that officials are “particularly attentive to domestic inflation” and that they “don’t have a recession in [their] baseline” for how the economy is expected to perform. All this was punctuated by a commitment to be “data dependent."

As it happens, the data seems to be telling a story about externally driven price growth and economic contraction. Food prices – where the ECB’s actions have little influence–remain the biggest contributor to headline CPI. Filtering them and energy costs–the “base effect” culprit–leaves price growth of just 2.3%.

Meanwhile, leading purchasing managers index (PMI) data shows that Eurozone economic activity shrank for a sixth consecutive month in December, with both manufacturing and the service sector in retreat. This suggests that a recession in the currency bloc is probably already underway.

With that in mind, the euro seems vulnerable as December CPI data prints this week. Traders may look through the widely expected jump in headline readings to focus on where they are coming from. If discounting external and base influences leaves domestic prices looking weak amid the downturn, the rate cut hopeful may drive the currency lower.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2024 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.