Friday Speedrun: October 20, 2023

Friday Speedrun: October 20, 2023

Bonds bonds bonds bonds bonds bonds bonds bonds

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Global Macro

Bonds bonds bonds bonds bonds bonds bonds.

Bonds bonds bonds bonds bonds bonds bonds.

BONDS!

The global bond market is repricing faster than Travis Scott tickets as a confluence of factors creates a crazy mismatch between supply and demand for fixed income securities. Some of the most popular explanations for the bond selloff:

Everyone was calling for a recession and US growth is printing 6%ish for Q3. Rarely has the market been so wrong for so long on the trajectory of the US economy. Initial Claims below 200k this week, the US jobs market remains robust, and the student loan restart and government shutdown were just figments of your imagination.

Supply / issuance. The US government is spending a ton of cash. That cash has to come from somewhere. It comes via bond issuance.

Japan's bond market is unglued as BOJ has kept wildly unsustainable policy for way too long. Bond yields below 0.5% and inflation above 3% are a toxic mix for the long end. Global bonds all trade in sympathy, so if Japan poops the bed, others will too.

Buyer’s strike. China isn’t buying, they’re selling. The Fed isn’t buying. Saudis aren’t buying. US banks are stuffed to the gills with bonds. Who is the marginal buyer right now? Answer: Nobody.

Higher for longer raises term premium.

.

Anyway, there are plenty of reasons! The only thing that matters right now is that they are going down. The what is more important than the why. Bonds are careening downhill like a bunch of lugers.

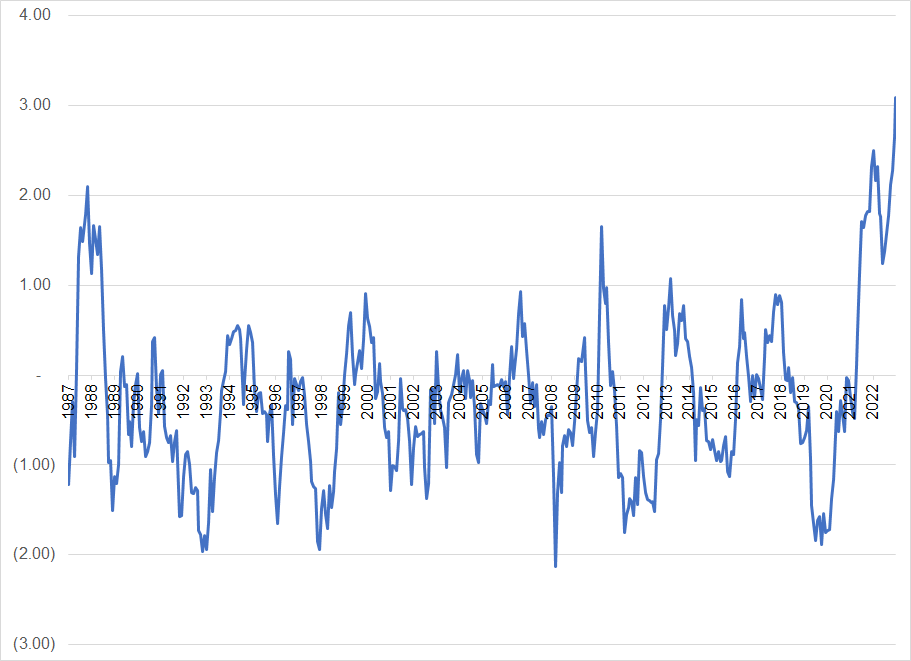

Two-year change in the US 30-year yield, 1987 to now

There are two camps with regard to what this rapid rise in yields means for the economy and risky assets. The first camp makes the somewhat commonsense observation that something is gonna break soon.

The less-popular but not radical view is that we are simply witnessing normalization. Rates were way too low. Now they’re back to their old happy place.

That is: Maybe this is no aberration and there isn’t anything all that nefarious going on. Maybe 2010 to 2019 was the aberration? I am more in the second camp as I think a return to properly-functioning capital markets with the price of money set well above 0% is a net good even if the road to getting there is likely to be scary, winding, and full of potholes.

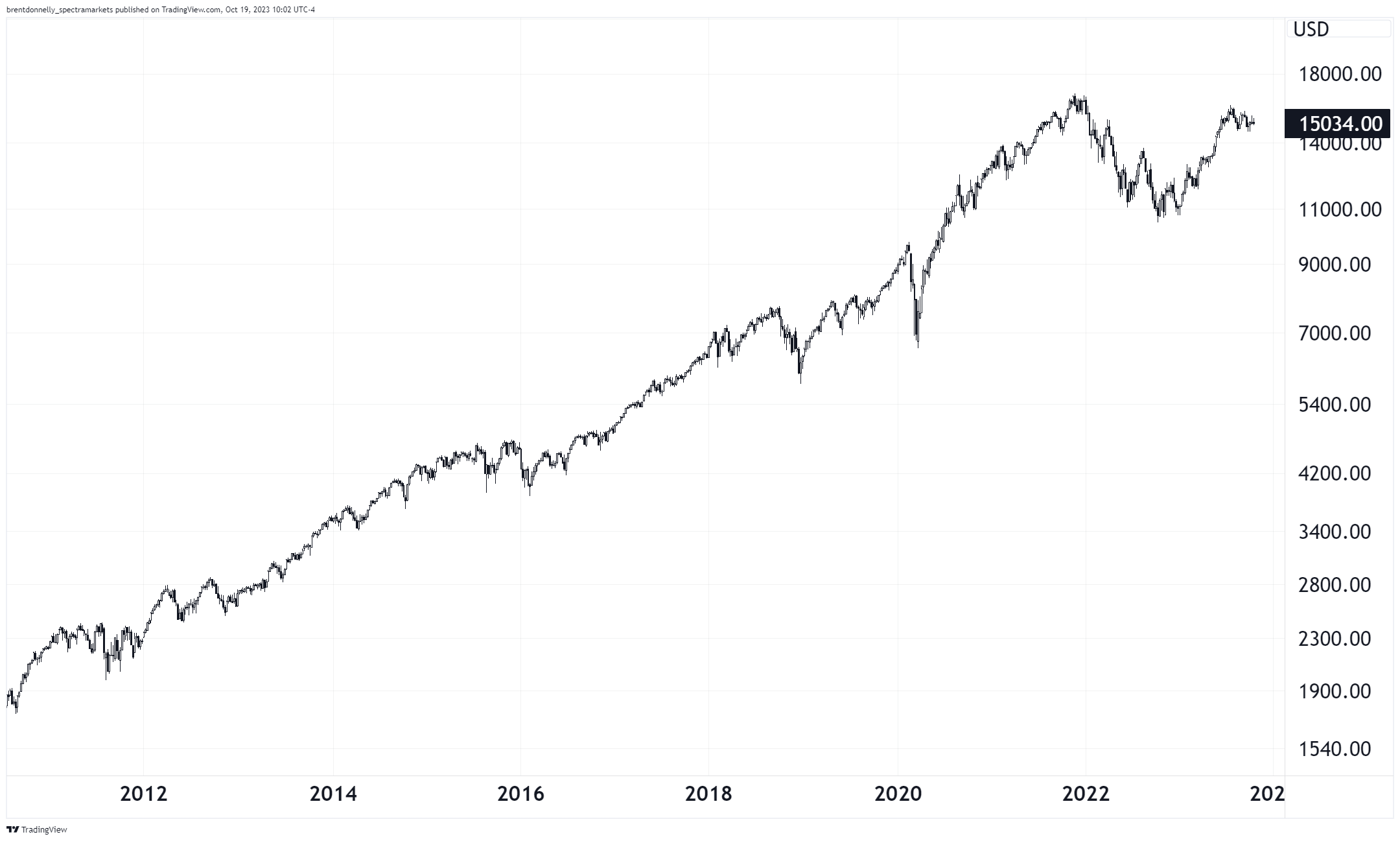

US 10-year bond yield, 1987 to now

AD

If you want to learn about trading, this book is jammed with so, so many useful lessons. Directional macro, technical setups, behavioral finance, positioning analysis, options vs. cash… And much, much more.

All written in an interesting and understandable way.

Buy the 50 Trades in 50 Weeks book on Amazon here.

END OF AD

Stocks

You might think that two wars, skyrocketing yields, persistent gloom, and high multiples would mean that stocks are trading down towards the lows, right?

Natalie Portman: Right??

A chart of the NASDAQ looks like this:

NASDAQ daily (log), 2010 to now

Apple trades kind of bruised, the media frenzy over AI has fizzled bigly, TSLA is running out of charge and yet… Here we are. And now the market is smack dab in the best seasonal period of the year and it feels like a rally would bring much sadness. Trading stock market indexes from the short side is one of the hardest jobs in the world. There are easier ways to make money.

Here is this week’s 14-word stock market summary: Tesla down, Netflix up, VIX up, stocks steady, year end rally ready for liftoff?

Interest Rates

Short Japanese bonds (JGBs) has been known as the widow-maker trade for decades because Japanese yields have gone inexorably down (yields down = bond prices up) even as Japanese gross debt levels are always top of the global league tables.

The widows are finding love these days.

Japan 10-year swap rate, 2009 to now

This is a good example of how “that trade never works!” is a backward-looking statement that suffers from extrapolation bias. There are plenty of trades that don’t work for ages, then pay off like a slot machine for a good period thereafter. Don’t allow the fact that something didn’t work in the past dictate whether you do it now or in the future. Now and tomorrow are not the same as yesterday.

Fiat Currencies

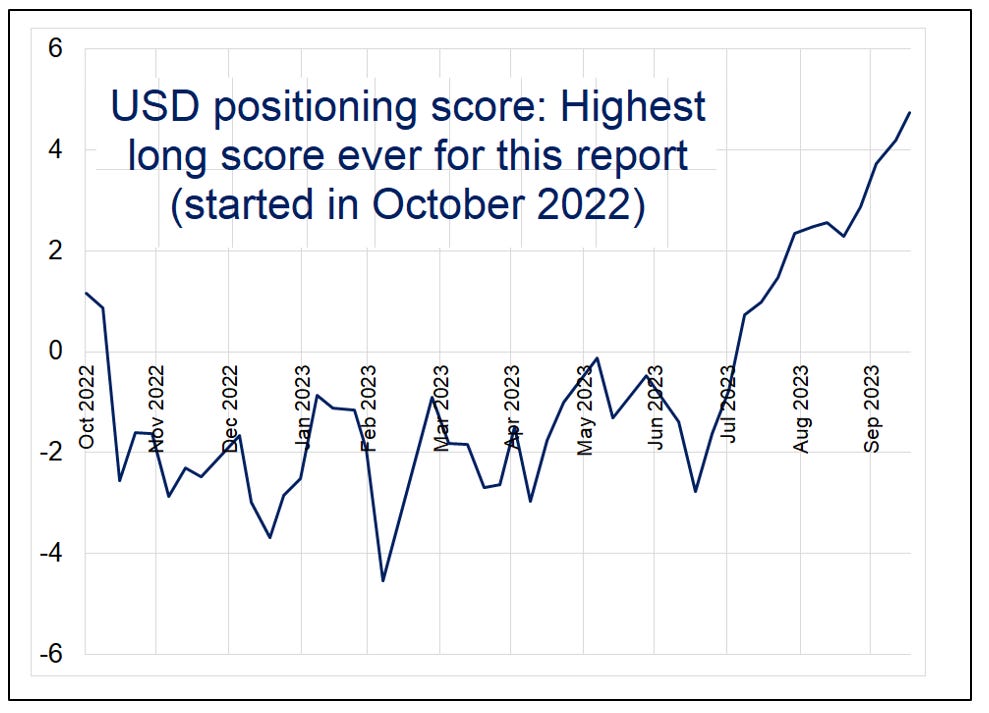

Dollar long positioning is extremely crowded as The Spectra FX Positioning Report showed this week. If you want my daily macro thoughts, including the positioning report every Monday and tons of other useful tools and insights, subscribe to am/FX. That’s the global macro daily I have been sending to institutions since 2006.

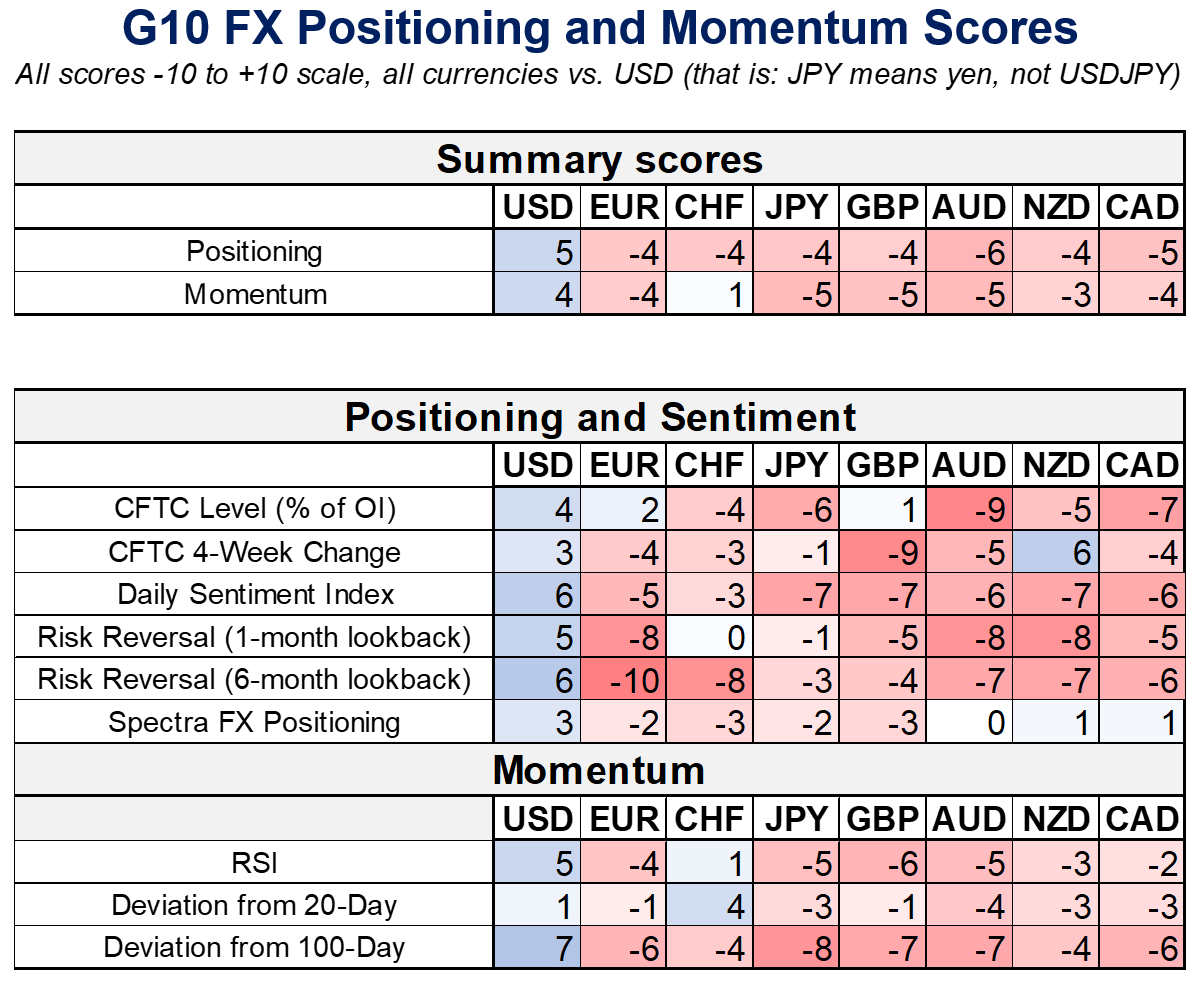

If you’d like more granularity, here is the positioning broken down by currency

This is a tricky setup as the dollar is trading like an all-weather beast. It does well when yields go up, it does well when stocks go up, it does well when stocks tank, it does well when oil does well. It’s hard to outline a regime where the dollar doesn’t do well these days!

But. But. But. The market is heavily long USD now, it’s somewhat overbought, and that makes it really hard to be bullish. Sometimes it feels pointless to be long and stupid to be short. This is one of those times for me.

The real story in fiat this week has been a big unwind of FX carry as MXN was hit particularly hard. In the context of the lovefest for Mexico, this is just a flesh wound, but it’s a big enough wound to require some gauze, not just Band-Aids.

USDMXN, mid-2020 to now

The story in Canada is getting a bit more interesting, too, as the lags from tighter monetary policy kick in Up North faster than they do in the USA because of the greater density of variable rate mortgages there. This week’s Q3 Business Outlook Survey from the Bank of Canada suggests the economy there is hitting the wall in slow motion. Canada’s exposure to real estate makes it a strong candidate for “Worst Economic Performance by a G10 Country” at the 2024 awards ceremony

Crypto

SBF is not looking good so far. Every ex-FTX employee is now happy to rat him out in micro detail as it seems that buying friends and influence only works until you run out of money.

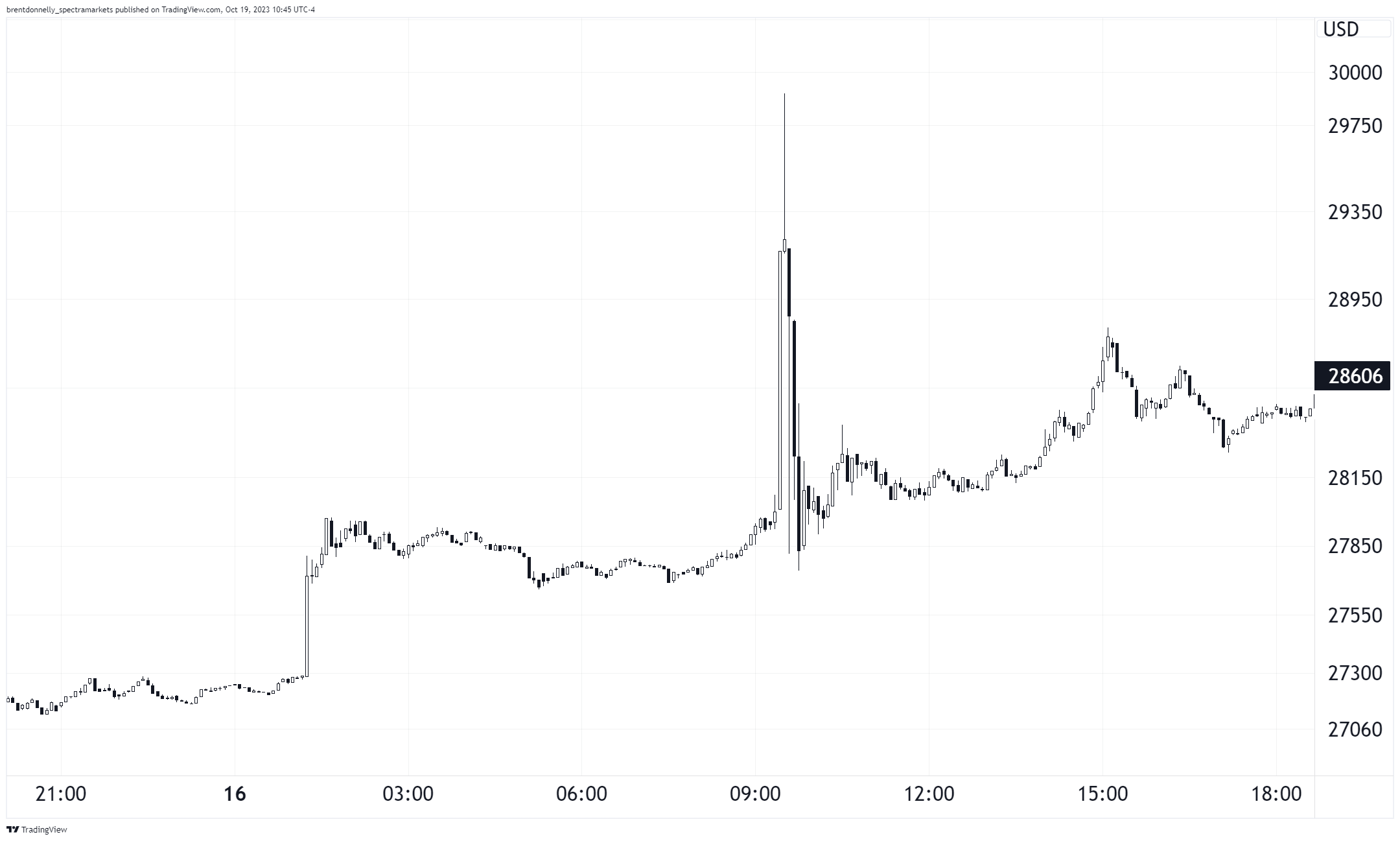

The Crypto Controversy of the Week winner was Cointelegraph as they published an erroneous tweet saying that the bitcoin ETF had been approved. Full mea culpa here. While you might have logically assumed that the ETFs are kind of priced in by now as the Grayscale discount has shrunk from 48% to 12% and it’s basically the primary news item almost every day… You would be wrong!

That spike from 28k to 30k and back to 28k was the outcome of the fake tweet shenanigans.

Bitcoin 5-minute chart, October 16

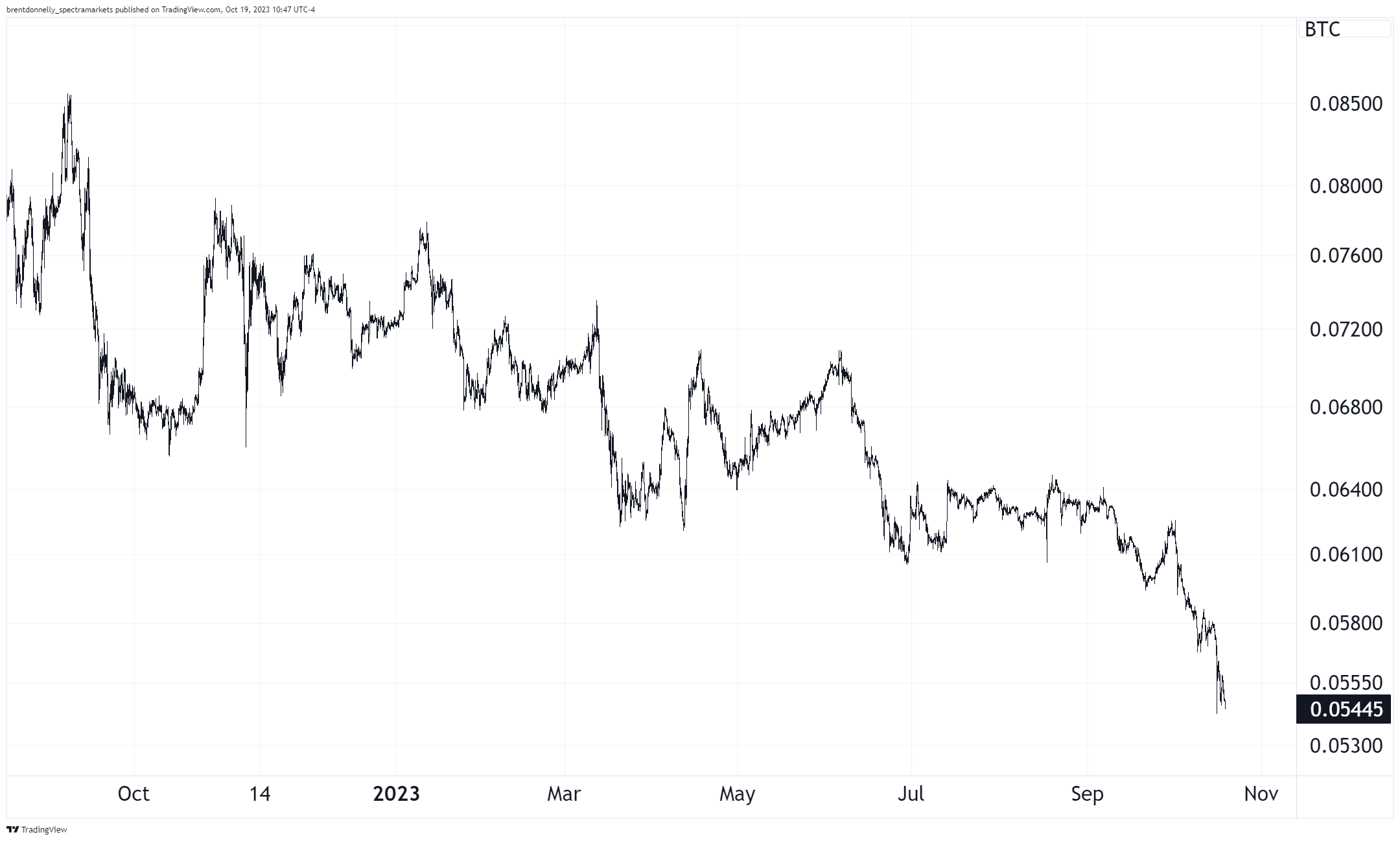

All this excitement about institutional demand for bitcoin has pushed ETHBTC to a new YTD low.

ETHBTC, 4-hourly, September 2022 to now

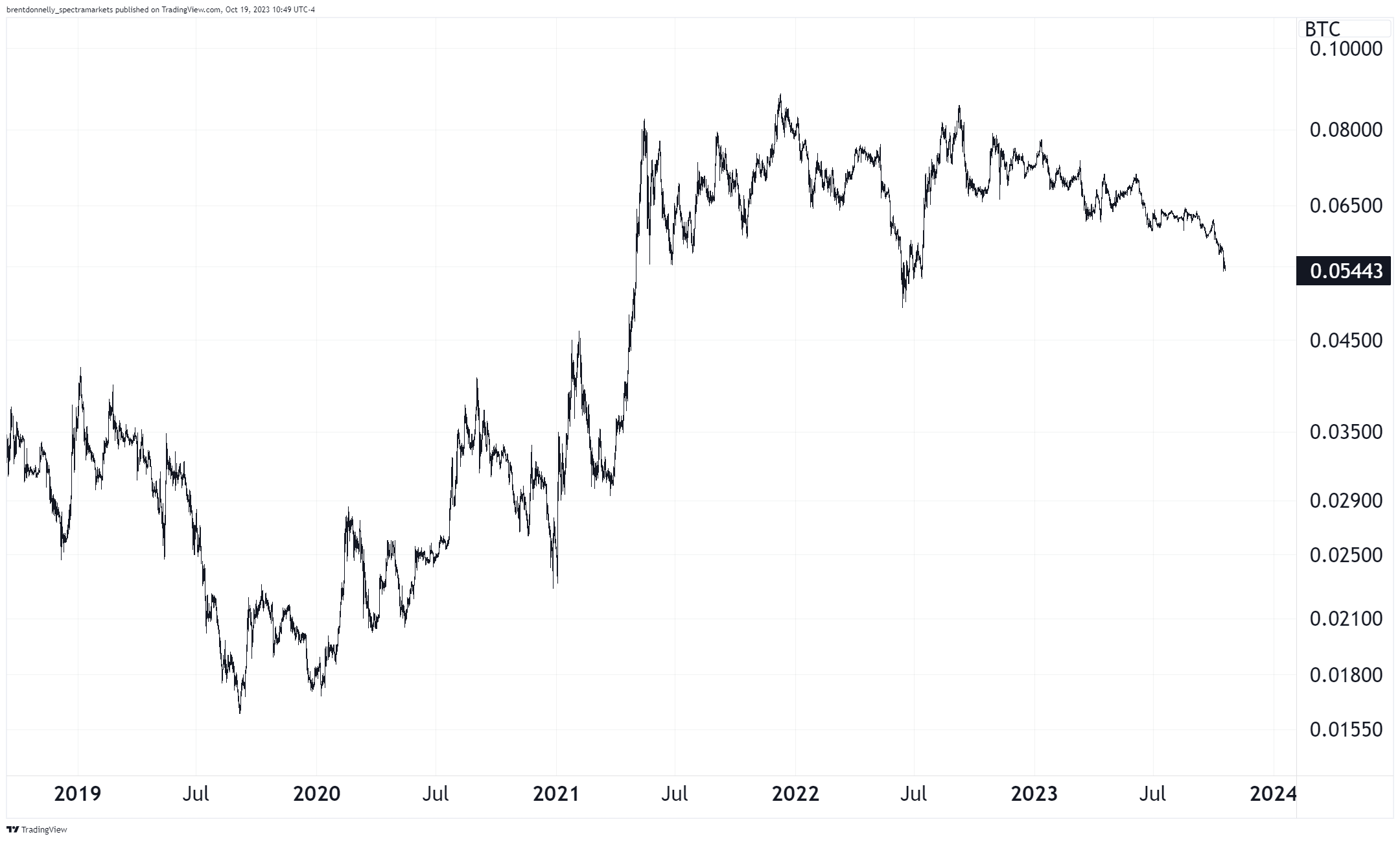

That said, if you zoom out, this is a blip. Low crypto volumes, low crypto volatility, a lack of excitement around new Web3 ventures, and high correlation between ETH and BTC have kept ETHBTC in a slow drift that cannot compare with the ETH-driven excitement seen in 2017 or 2021.

ETHBTC, daily late 2018 to now

Commodities

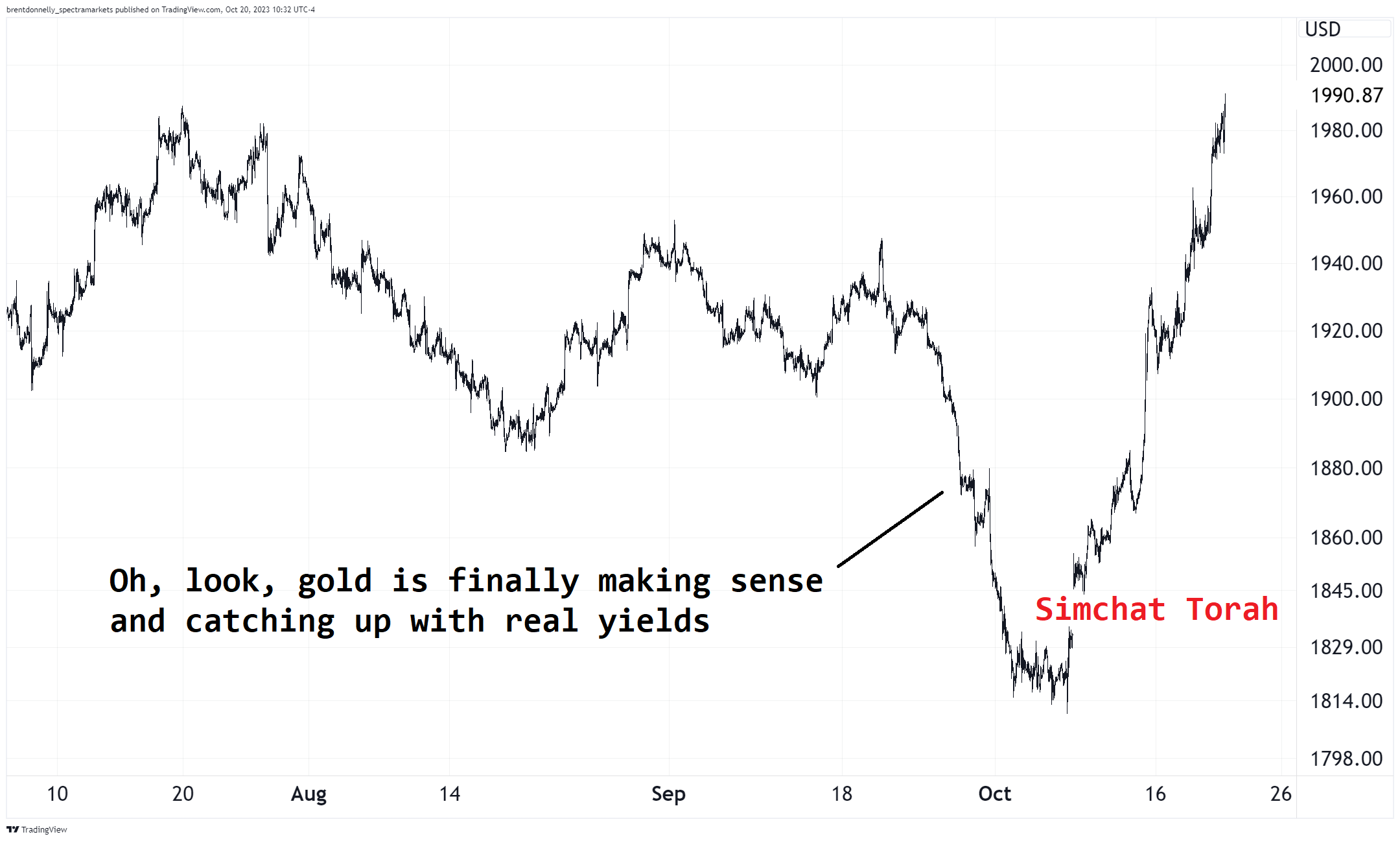

There is a shortage of safe havens. Bonds don't work in this regime (obviously) and neither does yen. The only two decent safe havens appear to be gold and CHF and those are getting gobbled up.

While gold's role as a safe haven is unreliable, it works here if people are trying to get their money out of things that can be seized in the case of dramatic escalation in the Middle East. If you have money in euros or dollars and you’re looking to park it somewhere safe from the Eye of Sauron, and away from the SWIFT system… Gold isn’t a bad idea.

Gold hourly, early August to now

It is not accurate to call gold a safe haven all the time. Quite often, it’s a liquidity barometer and it dirtnaps along with all the risky assets. But in times of capital flight, it’s a nice, shiny way to get your money out of the system.

Oil didn’t react too much to the events in Gaza, but the real fear trade in oil would only kick in if Iran gets involved. If that were to happen in any transparent way (i.e., not just hard-to-prove proxy activity) that would be very, very bad. It would take oil much higher and risky assets much lower.

But in the end, markets tend to overreact to wars because they are scary and while the human toll is obviously horrendous, the toll on markets tends to be short-term and non-persistent, especially when it comes to large caps.

This paper covers the topic nicely.

Geopolitical Threat, Market Capitalization, and Portfolio Return

In this paper, we validate that in the US equity market, the large and prime cap portfolios can generate significantly positive returns against geopolitical threats, whereas other medium and small cap portfolios fail to exhibit such results. The results of our investigation are equally supported by the Markov regime-switching model where we find that portfolio returns perform better against geopolitical threats during high-volatility regimes. Additionally, we demonstrate that geopolitical threat has a significant impact on the conditional volatility of large and prime cap portfolios. However, the monthly impact and lag effect of geopolitical threat is not visible in our results indicating that investors adjust their portfolios instantly against geopolitical threat. Our findings are robust in the presence of various alternative measures of market uncertainties, for example, economic policy uncertainty, economic uncertainty, VIX, etc. We also conduct a series of out-of-sample regressions to confirm our results. Finally, we report a few trading strategies using geopolitical threats.

OK! That was 6.84 minutes. Please share this Substack with any aspiring finance professionals that you know! Thanks!

Get rich or have fun trying.

Links of the week

Interesting / smart

The Atlantic: You can bet on anything now.

Welcome back

Natalie Portman.

Great joke.