Following a slow end to 2023, a slow start to 2024

Insight

Stronger than expected payrolls data initially saw yields sharply higher, equities lower, and the USD stronger, though with the unemployment rate steady and earnings growth moderating, those moves were retraced.

Events Round-up

GE Factory Orders MoM August: 3.9% vs fcst 1.5%, previous -11.7% (revised from -11.3%)

GE Factory Orders WDA YoY August: -4.2% vs fcst -7.9%, previous -10.5% (revised from -10.1%)

US chg nonfarm payrolls, Sep: +336k vs fcst +170k, previous +227k

US Unemployment rate, Sep: 3.8% vs fcst 3.7%, previous 3.8%

US avg hrly earnings, Sep: 0.2% (4.2% YoY) vs fcst 0.3% (4.3%), previous 0.2% (4.3%)

US labour force participation rate, Sep: 62.8% vs fcst 62.8%, previous 62.8%

CAD net chg employment, Sep: +63.8k vs fcst +20k, previous +39.9k

CAD unemployment rate, Sep: 5.5% vs fcst 5.6%, previous 5.5%

CAD hrly wage rate YoY, Sep: 5.3% vs fcst 5.1%, previous 5.2%

“Is it worth it? Let me work it

I put my thing down, flip it and reverse it” – Missy Elliot

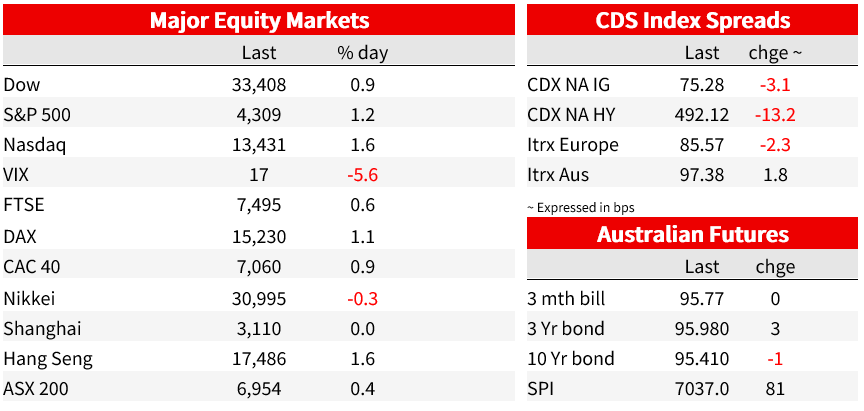

Stronger than expected payrolls data initially saw yields sharply higher, equities lower, and the USD stronger, though with the unemployment rate steady and earnings growth moderating, those moves were retraced. That retracement was only partial for US yields, with the US 10yr yield 8bp higher on the day and Fed pricing for the November meeting a little higher at 30%, resilience in the labour market keeping the threat of higher, or failing that higher for longer, rates alive. The US dollar was up as much as 0.6% following the payrolls data, but ends the day down 0.3%. Equities meanwhile reversed losses, with the S&P 500 up 1.2% on Friday to end the week 0.5% higher.

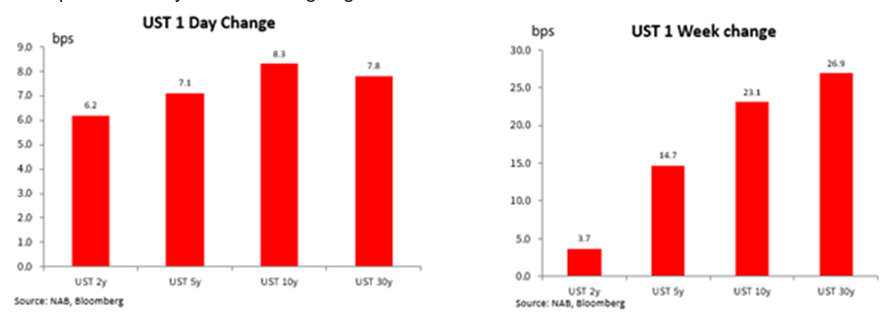

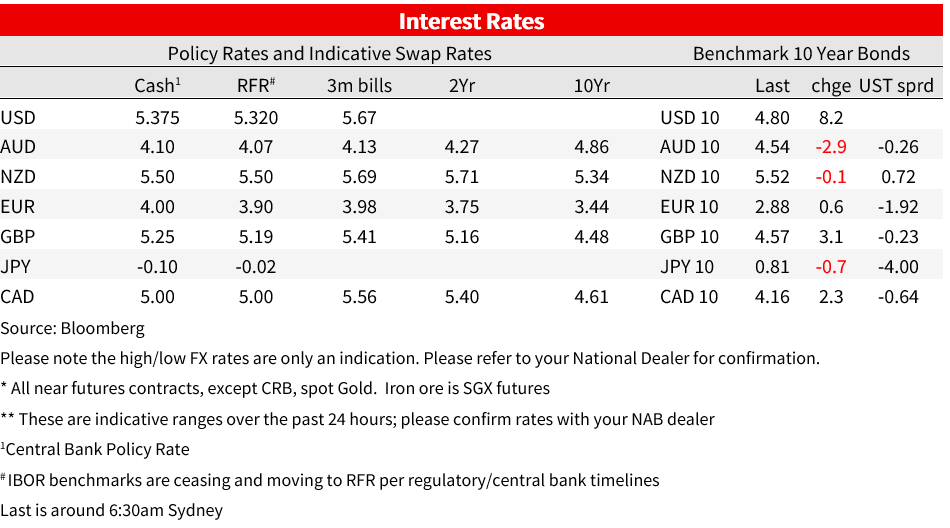

Payrolls smashed expectations, with payroll jobs up 336k against 170k expected. After 3 consecutive months of downward revisions, the beat in September was accompanied by a 119k net upward revision to the prior two months. Headline strength saw yields spike higher, but the detail suggested strong job gains overstated overheating in the labour market and the selloff was pared. The 10yr yields jumped around 14bp to a high of 4.89%, briefly surpassing its previous high on Wednesday, before paring gains to end the week at 4.80%, up 8bp on Friday. The 2yr yield jumped around 9bp to an intraday high of 5.14% and ended the day 6bp higher at 5.08%.

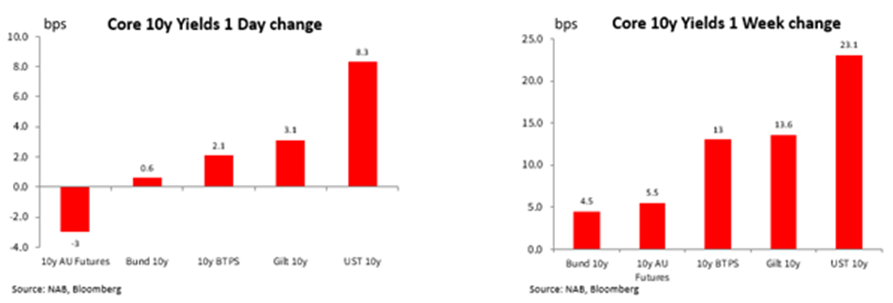

Yields were higher globally over the week, though the selloff was led by the US, and Treasuries underperformed on Friday. Over the week, the US curve steepened further. The 30yr was 27bp higher and the 10yr 23bp higher, compared to just 4bp for the 2yr. While markets remain comfortable policy rates are at or near their peaks, data resilience has seen expectations for cuts pared and longer-term real rates rise. Pricing for a hike at the November 1 FOMC meeting rose to 30% from 22% after payrolls data, and to 48% chance by year-end, up from 36%. Clevelend’s Mester said after the Jobs data that “with this one report, [the data] continues to say it’s a strong labor market, but it is getting a little bit less tight than we saw before ,” noting ‘tempering’ earnings growth. Over the weekend, Fed Governor Bowman on Saturday said she continues to expect “further policy tightening will be needed to bring inflation down in a sustainable and timely manner,”

The three-month average of payrolls gains is 266k, comfortably above pre-covid averages near 200k and rates needed to keep pace with population growth. It’s also faster than the pace of jobs growth earlier in 2023. As for the ratios out of the household survey, participation remained high at 62.8%, and the unemployment rate remained at 3.8% against expectations for a dip to 3.7%. Unemployment saw a low of 3.4% in April and was in a range of 3.5% to 3.8% in the year prior to the pandemic.

Substantial normalisation in the in the labour market has already occurred even without a large lift in the unemployment rate (see quits rates and trend decline in openings) and more helpful labour supply dynamics could explain why robust employment gains have occurred alongside still-moderating wages growth. Average hourly earnings were up just 0.2% m/m in September to be running at just a 3.4% 3m-annualised rate . That’s a noisy and heavily revised number but doesn’t say the labour market is too hot to forestall progress on disinflation. The Fed will look to the Q3 ECI on 31 October to confirm moderation in wages. Other indicators, including the Atlanta Fed Wage Tracker, have moderated less than AHE (so far).

Canadian labour market data was also strong, with employment up 64k jobs in September (+20k expected). The unemployment rate was unchanged at 5.5% while hourly wages accelerated to 5.3% y/y. Although the economy has slowed, inflation and the labour market have remained firm. The market is almost fully pricing a further 25bps hike by March.

China returns from National Day Holiday’s this week. Early reports on holiday spending are spending some 130% higher than the same period last year, but still only slightly above pre-Covid levels. Domestic tourism revenue reached 753.4 billion yuan for the eight-day holiday period, 1.5% higher than 2019, while there were 826m travellers, up 4.1% on 2019. Spending fell short of the tourism ministry’s forecast for just under 900 million travellers spending more than 780 billion yuan. Holiday spending is consistent with a consumption recovery that is still ongoing but has not seen a decisive shift.

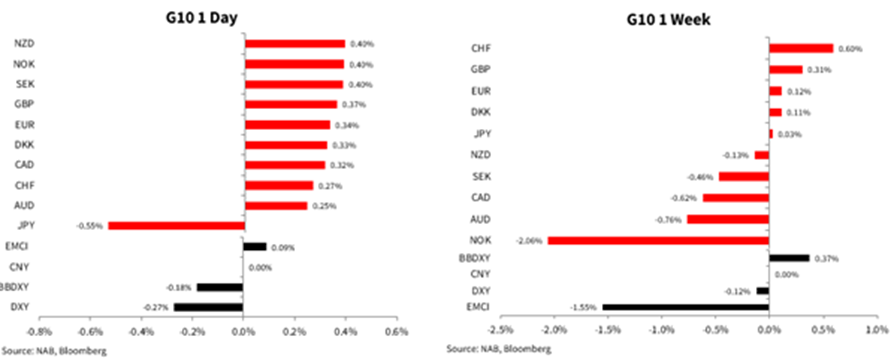

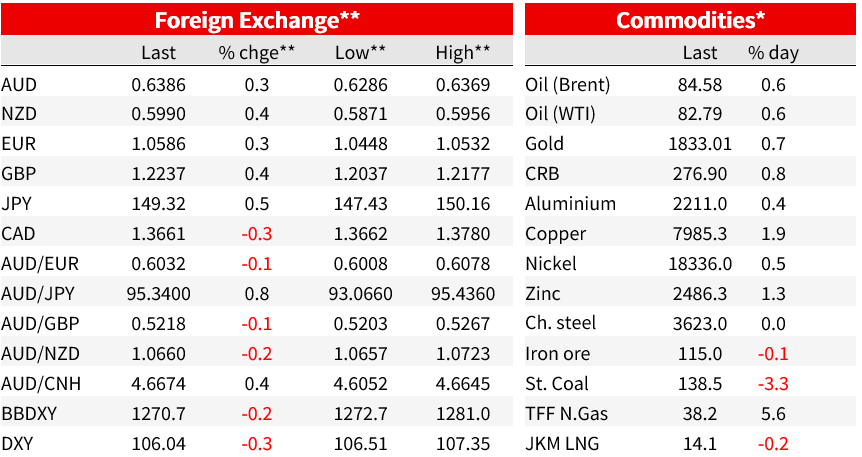

In currency markets, the US dollar was 0.3% lower on the DXY on Friday at 106.1, reversing earlier gains that saw it up close to 0.6% and near 107. The dollar was weaker against al G10 currencies except the yen on Friday. The Euro was 0.3% higher at 105.86, up 0.1% over the week. The AUD was up 0.25% on Friday against the broadly weaker dollar , though was among the worst performers over the week. The AUD was 0.8% lower over the weak, outpaced only by NOK among G10 currencies, and ended the week around 0.6386 after touching fresh year-to-date low of 0.6286 on intraday on Tuesday. The Yen was a notable underperformer on Friday, down 0.5% against the USD.

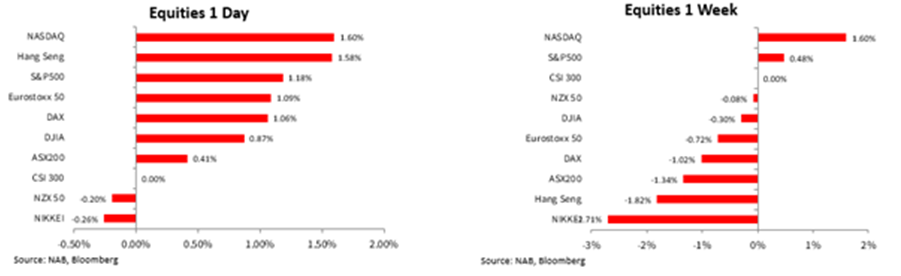

US Equities were higher on Friday, reversing declines early in the session. The S&P 500 rose 1.2% to be 0.5% higher over the week. That’s its first weekly gain in 5 weeks. The Nasdaq 100 was 1.7% higher on the back of gains in Microsoft, Apple, Nvidia. European equities were also higher on Friday, with the Eurostoxx 50 up 1.1%, though the index was 0.8% lower over the week.

US Earnings season kicks off this week, with third-quarter per-share profit expected to fall 0.3% for S&P 500 companies collectively, according to FactSet. 12 S&P500 companies are set to report in the week ahead, including JP Morgan, Citi, and Wells Fargo on Friday.

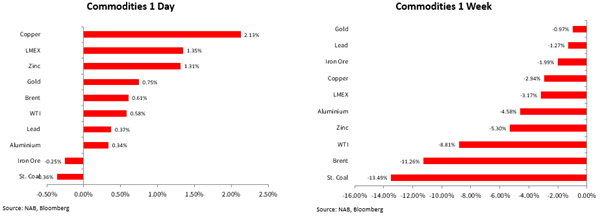

Oil was 0.6% higher on Friday, but Brent oil was down some 11.3% over the week to $84.58. That was the largest weekly drop since March. The move takes oil back to around its lowest since August, erasing the latest leg higher on the back of extended production cuts from Saudi Arabia and Russia. Commodity prices more broadly also generally declined over the week.

Developments in Israel and Gaza complicate the geopolitical picture for risk markets. While there can be expected to be few direct supply interruptions for oil without a broadening of the conflict, stricter enforcement of Iranian sanctions and waning hopes of more Saudi supply through 2024 alongside a normalisation of Saudi-Israeli relations have been cited by some analysts as potential immediate impacts. A Bloomberg Opinion article by Javier Blas makes the case that there is little prospect of a repeat of the 1970s oil shock, even if oil prices may be higher for longer (For Oil, It’s Not 1973, But It Could Still Turn Ugly – Bloomberg).

Coming Up

This Week

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Following a slow end to 2023, a slow start to 2024

Insight

Strong issuance volumes underpinned by extremely robust levels of investor liquidity and improved economic conditions.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.