Canadian growth shocker confirms central bank to pause

Canada’s economy surprisingly contracted in the second quarter with consumer spending slowing sharply and residential investment collapsing. Together with a cooling labour market, this should ease the Bank of Canada's inflation fears and lead to a no-change decision on 6 Sep. Still, the USD/CAD rally appears overdone, and we expect a correction soon

We expect a pause this week

Ahead of last Friday’s data, analysts were favouring a no-change outcome with just three out of 32 economists surveyed by Bloomberg expecting a 25bp interest rate increase while overnight index swaps suggested the market saw only a 15% chance of a hike. This was despite headline inflation surprising to the upside in July and the BoC signalling at the July policy meeting that it continued to believe inflation would only return to 2% by mid-2025 and that the door remained open to further hikes.

The GDP numbers and the manufacturing PMI that we got on Friday have only cemented the no-change expectation. Markets are now pricing little more than a 1% chance of a hike after the economy contracted 0.2% annualised in 2Q versus expectations of a 1.2% increase while 1Q GDP growth was revised down from 3.1% to 2.6%. Consumer spending rose just 1% annualised while residential investment fell 8.2% to post a fifth consecutive substantial contraction. Net trade was also a drag, but there was at least a decent non-residential investment growth figure of 10.3%. Meanwhile, the manufacturing PMI slipped to 48.0 from 49.6 to post its fourth consecutive sub-50 (contraction) reading.

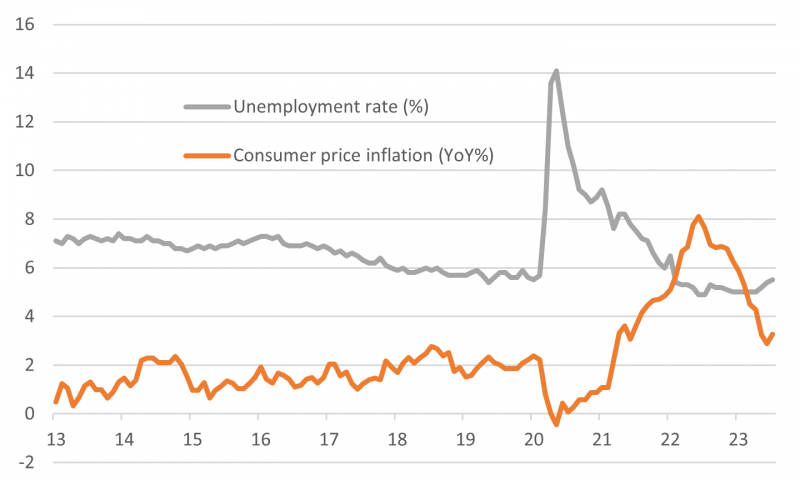

Canadian unemployment and inflation

Given the economy lost jobs in July we completely agree that the BoC will leave rates unchanged this month after having resumed hikes in June and July following a pause since January. Nonetheless, the BoC is likely to leave this as a hawkish hold given that policymakers are yet to be fully convinced they’ve done enough to return inflation sustainably to 2% given the recent stickiness seen. At a bare minimum, we will get a messaging of rates staying “higher for longer”, but given the perilous state of the Canadian property market and signs of spreading weakness globally, we do expect rate cuts to come onto the agenda by March next year.

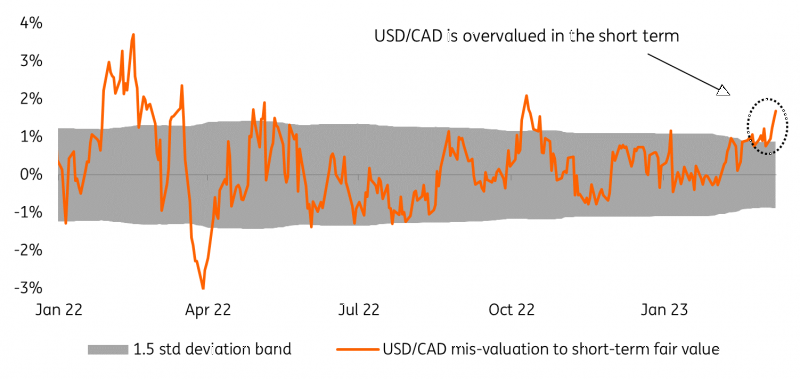

CAD weakness not justified

USD/CAD has rallied 3% since the start of August, broadly in line with the general strengthening in the US dollar, but in contrast with short-term USD:CAD rate differential dynamics. While USD/CAD rose in the past month from 1.32 to 1.36, the USD:CAD two-year swap rate differential was relatively stable in the -50/-40bp range throughout August, and only tightened to -30/-35bp after Canada’s poor 2Q GDP report.

Our short-term valuation model, which includes swap rate differentials as an endogenous variable, shows that USD/CAD is trading more than 2% over its fair value, a rather unusual mis-valuation level for the pair. Incidentally, CFTC data shows that speculators have moved back into bearish positioning on the loonie in recent weeks, with net-shorts now amounting to 9% of open interest.

USD/CAD is overvalued

We don’t expect the BoC to turn the tide for CAD, but the recent weakness in the loonie appears overdone, and technical indicators suggest a rebound is on the cards. We still expect USD/CAD to end the year close to 1.30 as CAD should benefit from the most attractive risk-adjusted carry in the G10, even without any more hikes by the BoC.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more