Currency strategy to achieve a better outcome for idle cash that may be awaiting deployment and earning little or no returns

Article

Bond sell-off reverses on softer US payrolls

Having thought that the wages sides of Friday’s US employment report might carry the day, in the event it was the slightly softer than expected non-farm payrolls print, with its attendant downward revisions, which prompted all of the post-data price action. With revision, the 189k NFP print reduced to 140k. This means payroll growth has averaged 218k in the past three months, down from 288k in the first four months of the year, a meaningful if modest slowdown, albeit enough to keep the unemployment rate flat. It was 3.5% at the end of 20122, and 3.5% now.

Average Hourly Earnings at 0.4% m/m left the annual growth rate at 4.4%, where it has been all year after coming down from 5.0% in late 2022. Stronger than the Fed would like (3-4%) though given the late July news on Q2 Employment Cost (1.0%) and last week’s non-farm productivity (3.7%) won’t be too troubling.

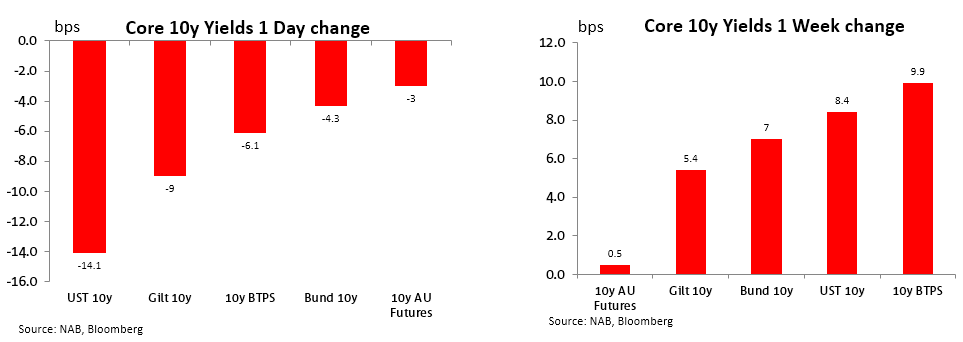

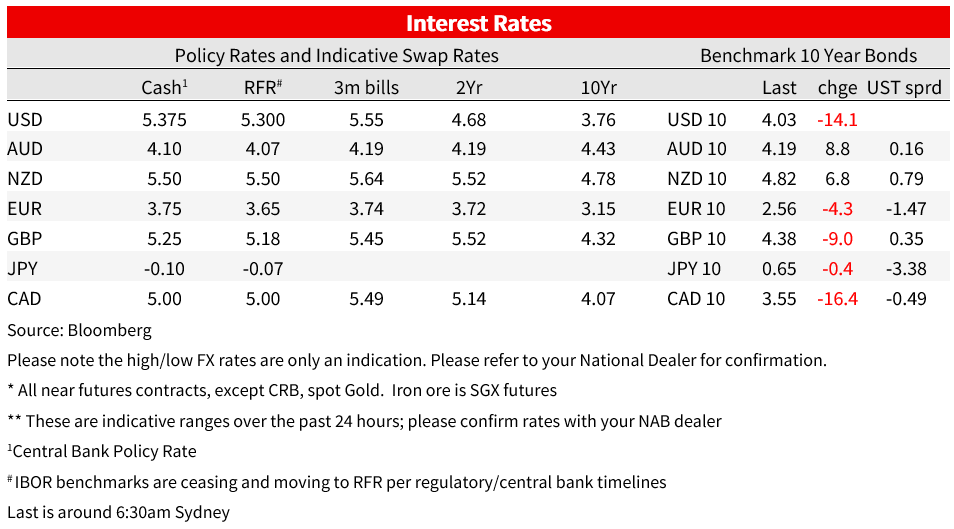

US Treasuries Friday & Weekly

US Treasuries rallied immediately following the non-farm payroll headlines, from 4.20% to 4.10% in the first 90 minutes, and to below 4.05% during the afternoon to end the week at 4.034%, a fall of just 8bps on the week. The 2yr slumped from 4.945% quickly down to 4.80% with falls extended to 4.764% by the close to be 12bps down on the week. Pricing for a further 25bps Fed rate hike in September reduced from 17% to 13%. For the curve, the front-end rally meant that while the curve was still much steeper on the week (2s30s +30bps) it was not in the end a pure ‘bear steepener’.

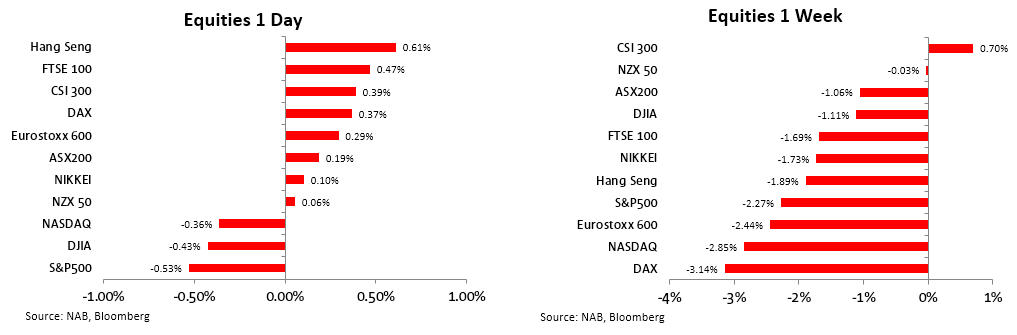

Equities Friday & Weekly

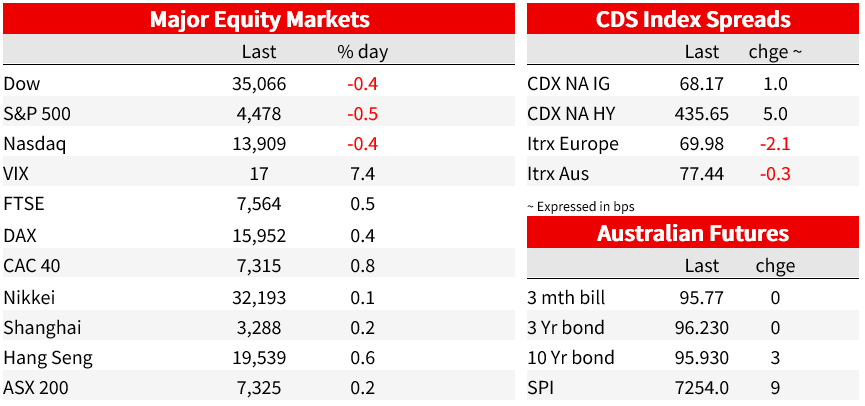

Equities, in the US and globally, underwent something of a reality check last week, the MSCI World index losing 2.3% for its worst week since March. Growth worries in Europe, and in China on so far unfulfilled promises of meaningful policy support, rising bond yields and Fitch’s US credit rating downgrade, are some of the fundamental factors fingered behind the sell-off. US equities failed to find comfort in lower bond yields on Friday, the S&P500 losing 0.5% and the NASDAQ 0.4%, not helped by Apple’s 4.8% drop following Thursday night’s earnings report which, unlike Amazon results half an hour before, failed to blast though analysts’ pre-release expectations. IT, down 1.5%, was the worst performing sub-sector.

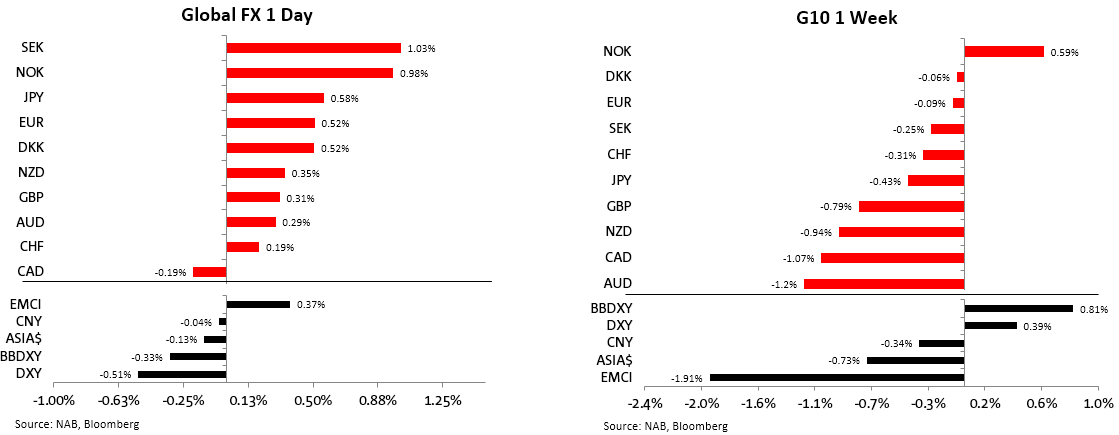

FX Friday & Weekly

FX market weren’t quite able to keep up with the antics of the bond market last week, though payrolls did produce a meaningful reversal of Monday-thru-Wednesday US dollar gains that had pulled the DXY index up to a one month high and so reversing all the post-July US CPI losses. DXY lost 0.5% on Friday, trimming its weekly gains to just 0.4%. The Scandies led the move with both NOK and SEK up 1%, followed by JPY, the latter finally getting some relieve from the fall-back in 10-year Treasury yields. EUR/USD also gained 0.5% to just creep back onto the 1.10 handle, while gains for GBP and AUD and NZD were limited to about 0.3%.

CAD was the only G10 loser Friday, after its employment report showed a loss of 6.4k jobs against +25k expected and the unemployment rise from 5.4% to 5.5% as expected. CAD’s loss of 0.12% brought its weekly fall to 1.1%, though this was still exceeded by the AUD, the worst performing G10 currency, suffering on the RBA’s 1 August ‘no-change’ and heightened sense they could be done at 4.1% , plus ongoing concerns about the veracity of promised official support for China’s economic growth.

Friday’s RBA SoMP revealed that the Board again considered the case for a hike this month before deciding against. It downgraded its 2023 growth forecast – to 0.9% from 1.2%, but also its 2023 inflation forecast – 4.1% from 4.5%, and its forecast now show inflation at 2.75% in its (for the first time) end 2025 forecasts. Despite which, local money markets ended Friday lifting pricing for the terminal RBA cash rate to 4.23% from 4.20% Thursday (coincidentally, roughly in line with the 4.25% assumed cash rate implicit in the new SoMP forecasts).

Friday also brought news of China lifting trade sanctions on Aurlain barley imports (80.5% duties). The Weekend Aurlain said it understood the announcement came after Beijing received a draft copy of the WTO ruling that was problematic for China, though there is also a suggestion, the newspaper notes, that the lifting of the ban could also be because of Russian’s inability to meet China’ barley demand. Australian trade officials have understandably been quick to call the resolution of the barley dispute a template for the wine industry, though the same Weekend Australian article quotes Lowy Institute senior fellow Richard McGregor warning against assuming the lifting of sanction in wine would follow the same path as barley, noting that Chinese wine producers were voicing opposition to dropping the sanctions.

Other China related news worth noting Friday includes two FT reports, one saying the US and China are opening new lines of communication to tackle contentious issues, in one of the first signs of progress towards stabilising relations since secretary of state Antony Blinken visited Beijing in June. Another says Chinese authorities are putting pressure on prominent local economists to avoid discussing negative trends such as deflation, as concerns mount about Beijing’s ability to boost a flagging recovery in the world’s second-biggest economy. Multiple local brokerage analysts and researchers at leading universities as well as state-run think-tanks said they had been instructed by regulators, their employers and even domestic media outlets to avoid speaking negatively about topics ranging from fears of capital flight to softening prices. Seven well-regarded economists told the Financial Times that their employers had told them some topics were off-limits for public discussion.

Commodities Friday & Weekly

Coming Up

Market prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Currency strategy to achieve a better outcome for idle cash that may be awaiting deployment and earning little or no returns

Article

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Newsletter

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.