Our monthly transaction data suggest spending ticked up in April after a stagnant performance last month

Insight

Weak European PMIs have seen yields fall, though moves in US Treasuries retraced latter in the day.

“This thing we started, I don’t want it to stop; You know you make me shiver; Yeah, you got me singin’ like”, Ed Sheeran 2021

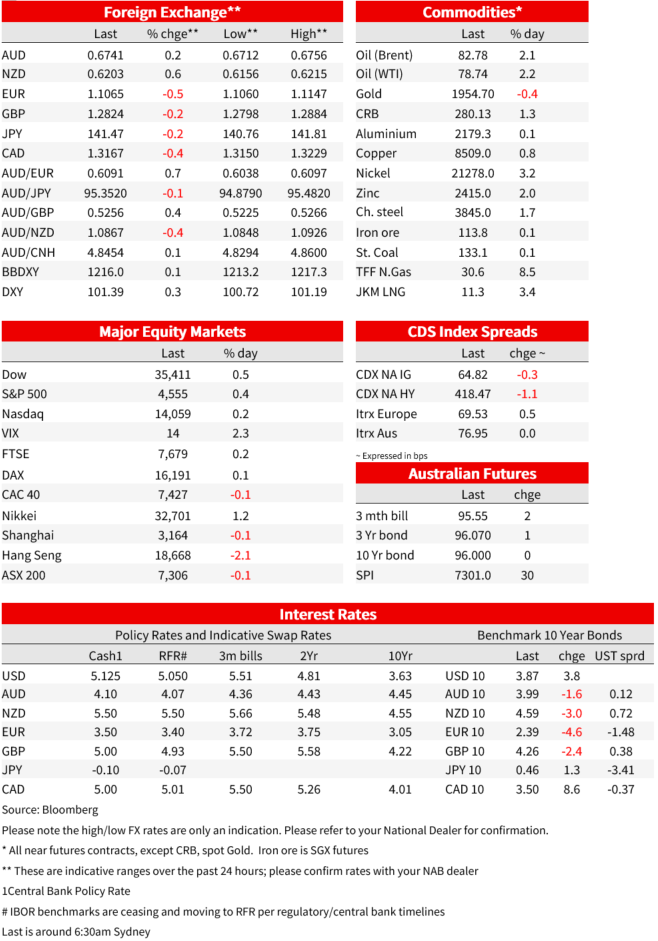

Weak European PMIs have seen yields fall, though moves in US Treasuries retraced latter in the day. China’s Politburo also announced some supportive measures for the real estate sector and for consumption, though fell short of announcing large-scale fiscal or monetary stimulus – will more come later in the week?. Given expectations for stimulus had been pared back, a modest risk-positive reaction has occurred with copper erasing earlier losses given mooted property support to be up 0.8%. As for the PMIs the Eurozone Composite was 48.9 vs. 49.6, and while weakness in manufacturing is well known, what was the bigger surprise was a softening in services which fell to a six-month low to 51.1. Global bonds initially rallied in the wake of the data with the German 10yr -4.4bps to 2.43% and 2yr -4.7bps to 3.05%. However in the UK and the US that early rally was later reversed. The US 10yr is actually up 4bps to 3.87%, after having hit an intra-day low of 3.79%.

In FX the weakness in the European PMIs weighed on EUR (-0.5%) and GBP (-0.3%), with the USD (DXY) up 0.3%. USD/JPY (-0.2% to 141.50) stabilised after several days of losses with reports the BoJ is considering large increases to inflation forecasts. Although no change to policy is expected on Friday, an upward revision to forecasts would increase the prospects of a move at a subsequent meeting. The AUD meanwhile was little changed +0.1% and NZD was stronger at +0.5%. Equity markets remain resilient with a deluge of earnings this week. The S&P500 rose 0.4% and remains just 5% off its all time high, having rallied some 27% from its lows of 2022. Today’s gains were led by the energy sector (+1.7%) with Chevron (+2.0%) beating expectations alongside the rise in oil prices overnight (Brent +2.2% to $82.85). It is a big earnings week for companies with 150 S&P500 companies report, comprising around 30% of the broader index.

First to the Chinese Politburo. The top decision making body did not announce large-scale stimulus, though the announcement did not necessarily disappoint given expectations for stimulus had already been pared. According to Xinhua, China will stick to “proactive fiscal policy and a prudent monetary policy”, will seek to keep the RMB “generally stable at an appropriate and balanced level”. There was some talk of boosting consumption, particularly for “automobiles, electronic products and household items” and as well as on services such as “sports, leisure and cultural and tourist services ”. No specific policy tool to boost consumption though was cited. A plan is to be announced to resolve local government debt risks, as well as increasing support for the property market (see Xinhua: China Focus: CPC leadership maps out priorities for China’s economic development in H2). Market moves have been fairly contained, though it was been risk-positive overall – most commodities were up overnight and copper erased earlier losses to be up 0.8%.

As for the PMIs, the Eurozone PMIs disappointed across the board with the Composite falling to an eight month low at 48.9 vs. 49.6 expected and 49.9 previously. The Manufacturing PMI was very weak at 42.7 (vs. 43.5 expected) and is at a 38-month low, while in Germany the Manufacturing PMI was even weaker at 38.8. The worrying bit of the report was not necessarily the ongoing weakness in manufacturing, but the slowdown now being seen in the services sector – which to date had been insulated from manufacturing weakness. Instead the Eurozone Services PMI fell to a six-month low at 51.1 (vs. 51.6 expected) and in France it went deeper into contraction territory at 47.4 (from 48.0) and is at a 29 month low. One snippet was interesting, suggesting pushback from recent price increases “ services companies also linked lower sales to falling activity, although some companies commented on clients being deterred by higher prices”.

On the prices front the PMIs were more encouraging, noting that “price pressures meanwhile moderated further, with average selling prices rising at the slowest rate for almost two-and-a-half years. Price charged by manufacturers fell at a rate not seen since the height of the global financial crisis in 2009 amid slumping demand, while service sector selling price inflation cooled to a 21-month low” (for details see S&P Global PMIs for Eurozone, Germany and France). Overall the PMIs suggest the Eurozone has slowed further and that the ECB will move to greater data dependency after Thursday’s 25bp hike. Markets are almost fully priced at 97% heading into Thursday, and are 79.6% priced for a follow up hike by December. Yields moved lower in the wake of the CPI data with the German 2yr yield -4.7bps to 3.05% and 10yr yield ‑4.4bps to 2.43%.

Across the channel it was a similar story of PMI weakness with the UK Compositive at 50.7 vs. 52.3 expected and 52.8 previously. While manufacturing again led the decline (Manufacturing PMI 45.0), the real worry is the slowdown being seen on the services side with the Services PMI at 51.5 vs. 53.0 expected and 53.7 previously, falling to a six month low. Comments in the report noted “a number of firms

cited weaker residential property market conditions, while others commented on cutbacks to discretionary business and consumer spending”. While softness appears to be emerging, on prices the strong lift in wages growth is continuing to be pass on (“private sector companies indicated a robust rise in their average prices charged in July, largely due to the pass through of higher staff wages across the service economy”), meaning the BoE will need to remain hawkish. There was only a slight paring back of BoE rate hike expectations with a cumulative 87.9bps priced by February, from 91.6bps.

In the US, where next week’s ISMs are far more important, the Composite PMI was 52.0 vs. 52.0 expected and 53.2 previously. In contrast to Europe, the manufacturing side rebounded (49.0 from 46.3), while services underperformed expectations (52.4 from 54.4).

Coming up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Our monthly transaction data suggest spending ticked up in April after a stagnant performance last month

Insight

Conditions, employment fall back to long-run average

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.