Conditions, employment fall back to long-run average

Insight

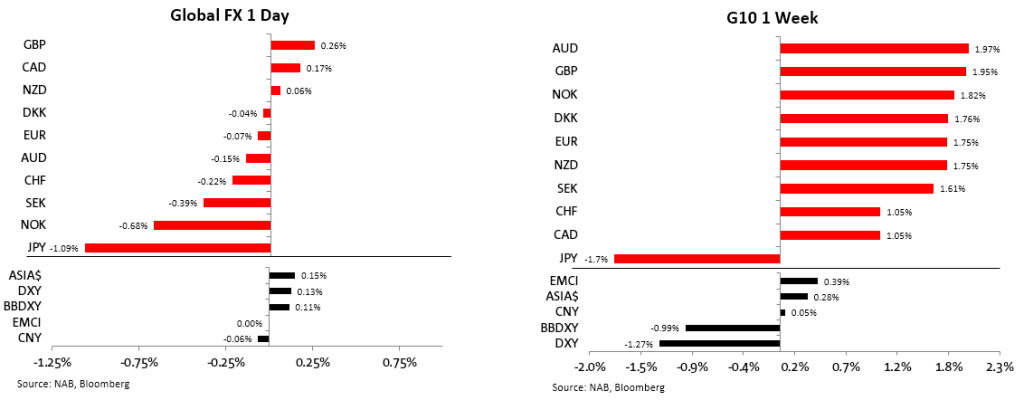

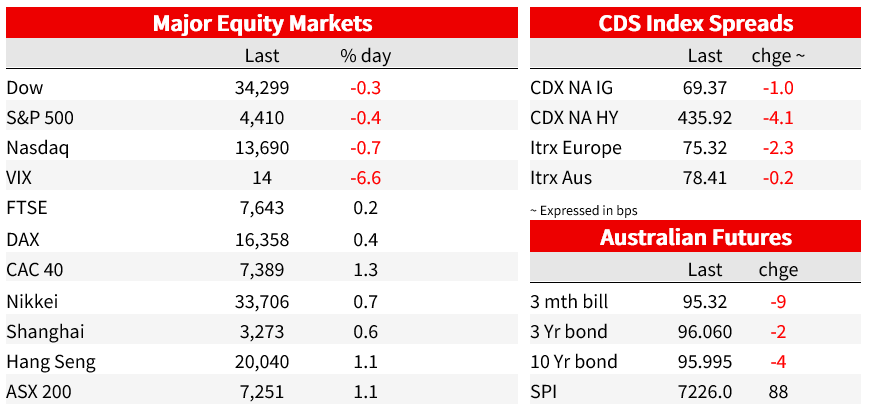

AUD ends a big if short local week at the top of the G10 currency pile, AUD/USD +2% w/w

Friday’s Economic Data and Events Highlights:

BoJ policy rate target -0.1%, unchanged as expected

BoJ 10Yr YCC target 0.0% (+/-0.5%) unchanged as expected

Final May EZ CPI 5.3% unchanged as expected

BoE/Ipsos Inflation next 12mths. 3.5% down from 3.9%

Uni. Of Michigan June Prelim. Consumer Sentiment 63.9 from 59.2 vs 60.0 expected

Uni of Michigan 5-10 Yr Inflation Expectations 3.0% as expected vs 3.1% in May

Uni. Of Michigan 1 Yr Inflation Expectations 3.3% vs 4.1% expected vs. 4.2% in May

A memorable week for markets concluded with the AUD at the very top of the G10 currency pile, up 2% with positive risk sentiment firmly in the driving seat and the JPY firmly at the bottom after the BoJ left policy unchanged and Governor Ueda gave no succour to those (like us) looking for a shift out of next month’s meeting. AUD/JPY rallied by a cool 4.7% on the week. A small dose of US equity market profit taking Friday still left the S&P500 up over 2.5% and firmly back in bull market terrain. This was nothing compared to the 4.5% gain for the Nikkei, by far the DM world’s best performing market, followed by the Hang Seng, the latter driven by the PBoC’s mid-week policy easing and strong hints in local media of fiscal policy support soon to be forthcoming after May activity and credit data confirmed the faltering post-zero covid economic recovery. The US yield curve bear-flattened out of the FOMC with its accompanying addition of two further quarter-point rate hikes to its 2023 dot plot, but neither US equity and interest rates market nor too the FX markets are yet buying what the Fed is selling. UK CPI, the Bank of England and ‘flash’ PMIs promise to the highlight of the coming week – which begins with the US’ Juneteenth holiday (stock and bond markets are both closed today)

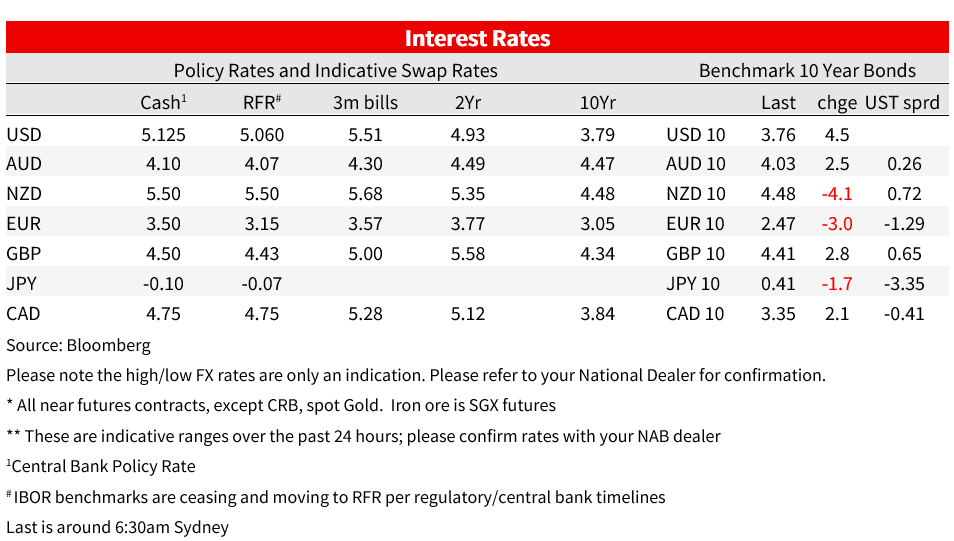

The Bank of Japan left policy unchanged in all respects on Friday. In the ensuing press conference, Governor Ueda said he expected wages to rise much more than last year but that the uncertainties for the outlook were high including the outcome of (ongoing) annual wage negotiations. He admitted the pace of decline in inflation has been somewhat slower than expected, but that whether towards the ‘middle of 2023’ the overshoot relative to the BoJ’s April outlook continues or inflation shows sharply is ‘highly uncertain’. A literal interpretation of the latter would be that the BoJ will only pass judgement on whether its prior view is right or wrong much later in Q3 or early in Q4 (i.e. mid fiscal year) but the BoJ has too much form blindsiding markets to rush to this judgement. In our view July is still live for a possible policy shift. The market upshot of the BoJ pronouncements was a small (1.5bps) fall-back in 10-yr JGB yields to 0.40% and extension of pre-BoJ JPY weakness, USD/JPY rising to its highest since 22 November 2022 just shy of ¥142 and AUD/JPY’s high of ¥97.58 its best since mid-September 2022.

Friday’s main data point was the preliminary University of Michigan Consumer Sentiment survey, sentiment up to 63.9 from 59.2 – stronger than expected – but whose correlation with retail spending has been particularly poor in the post-pandemic era to date. More relevant perhaps, the 5-10year inflation expectations gauge slipped to 3.0% from the 3.1% May final reading (originally put at 3.3%). Steady but still a little too high for Fed comfort (comparing to the pre-pandemic average closer to 2.5%). The 1-year read fell sharply though, to 3.3% from 4.2% (4.1% expected) driven by lower energy and food prices. A fall-back in 5-10-year expectations may well follow in coming months if headline inflation falls further.

Fed speakers on Friday included Governor Waller speaking at a Norges Bank/IMF event who claimed the US economy was still “ripping along for the most part” and that everything seems to be calm in the banking system, such that he did “not support altering the stance of monetary policy over worries of ineffectual management of a few banks”. Richmond Fed President Thomas Barkin said, “I am still looking to be convinced of the plausible story that slowing demand returns inflation relatively quickly to that target” and that “If coming data doesn’t support that story, I’m comfortable doing more”. And Chicago Fed President Austan Goolsbee said he thought of the Fed’s pause as a “reconnaissance mission, pausing now to scope it out before charging up the hill another time”’.

Meanwhile the Fed released its semi-annual monetary policy report ahead of Congressional testimonies from Fed chair Powell this week in which it noted it will make future decision on interest rates on a meeting-by-meeting basis, that tighter credit conditions are likely to weigh on the economy and that a period of below trend growth is likely to be needed to curb inflation.

ECB officials were also out in forc e, including President Lagarde who reaffirmed that a July rate hike was ‘very likely’ following which the ECB would follow a data dependent approach. We also heard from no fewer than seven Governing Council members – Rehn, Holtzmann, Muller, Centeno, Guindos, Munch and Villeroy. While the hawkish contingent among them stressed that rates hikes may have to continue beyond September, probably the best summation was from Muller who said that “what happens after July is pure speculation”.

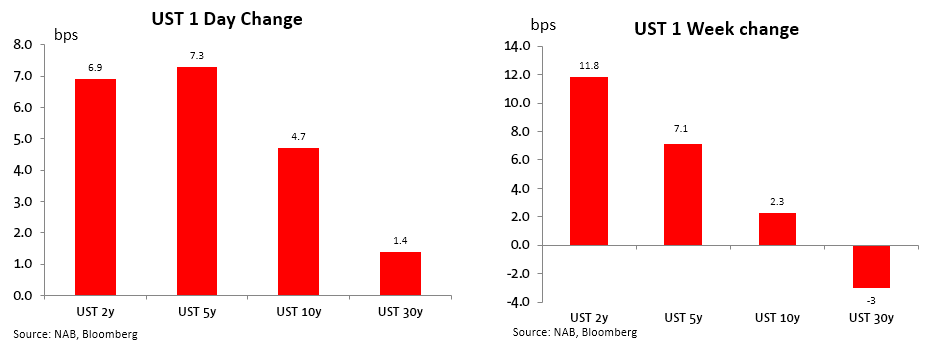

US Treasury yields rose across the curve on Friday, 2s by 7bps, 10s by 4.7bps and the 30-year a lesser 1.4bps, with more pronounced curve flattening over the week as a whole (2s +11.8bps, 10s 2.3bps and the long bond actually down, by 3bps). At -95bs, the 2/10s curve is at its most inverted since early March and reapproaching its 8-March maximum inversion of -109bps. A holiday shortened Australian week saw the yield on 3-year futures up 15bps to 3.95% and 10s a lesser 6bps, to 4.0%.

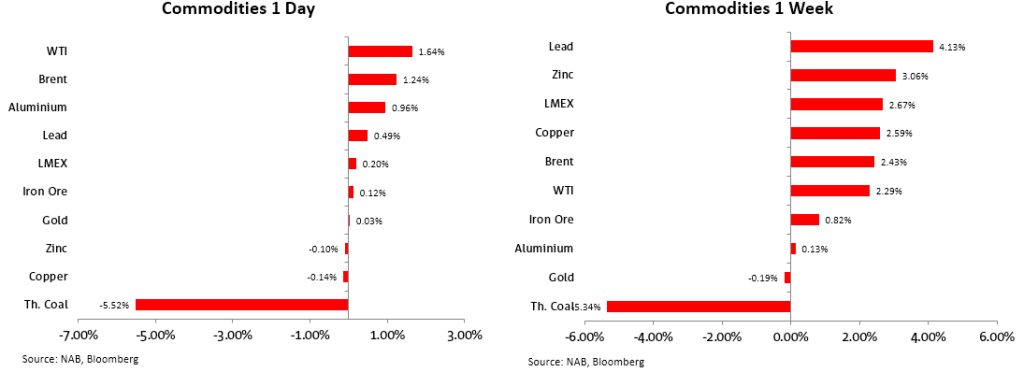

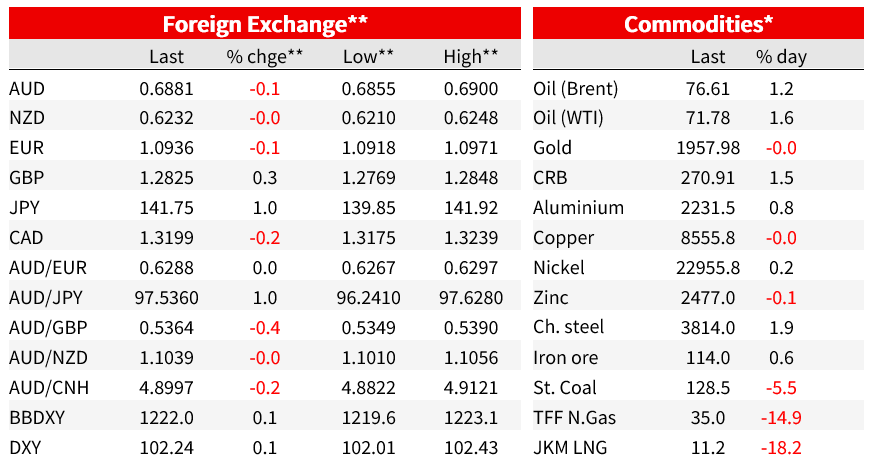

Buoyed by the promise of China stimulus, commodities for the most part were stronger Friday, capping a mostly ‘up’ week that saw the LMEX base metals index add 2.7% led by a 4.1% gain for lead and with ‘Dr Copper up 2.6%. The exception was thermal coal, down 5.5% Friday and similarly on the week. Relevant or not, AGL Energy Ltd. On Friday said it would massively expand its production of clean energy as it abandons coal-fired power plants. The company will spend as much as A$10 billion ($6.9 billion) of its own money to build new facilities, including with debt-financing, Chief Financial Officer Gary Brown said at an investor day in Melbourne on Friday.

A big week in FX that saw AUD/USD rise by 2% to be 6.5% up on its 31 May lows, was characterised on Friday by the more than 1% rise in USD/JPY linked to the BoJ’s no-change and higher US Treasury yields. AUD gave back a little of its Monday-Thursday gain (-0.15%) while ahead of the BoE this week, GBP extended its rise – GBP/USD to a high of $1.2848, its best since late April 2022, to vie with AUD for top slot on the week. All bar CHF, CAD and JPY were up by more than 1.5% – not bad in a week when the Fed tried to convince markets there are two more rate rises in the chamber this year. The DXY lost 1.3% on the week.

Finally, news wise, the AFR’s John Kehoe writes in the AFR this morning that the RBA and Treasury are considering the RBA executing a U-turn on its pandemic “money printing” stimulus and selling federal bonds back to the government. The bonds would be sold either to investors on the open market or directly to the AOFM. But any bond sales would be gradual, Kehoe writes, and not aim to use QT as an active monetary policy tool to push bond yields higher or tighten financial conditions. A decision on QT will be made after September 30, to assess the market impact of commercial banks repaying almost half – $84 billion – of the money borrowed from the RBA’s emergency term funding facility (TFF).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Conditions, employment fall back to long-run average

Insight

Currency strategy to achieve a better outcome for idle cash that may be awaiting deployment and earning little or no returns

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.