Currency strategy to achieve a better outcome for idle cash that may be awaiting deployment and earning little or no returns

Article

The absence of a debt ceiling deal weighs on risk sentiment even as Biden calls talks ‘productive,’ while global PMIs reaffirm the stark divergence between services and goods.

GE: Manufacturing PMI, May: 42.9 vs. 45.0 exp.

GE: Services PMI, May: 57.8 vs. 55.0 exp.

EA: Manufacturing PMI, May: 44.6 vs. 46.0 exp.

EA: Services PMI, May: 55.9 vs. 55.5 exp.

UK: Manufacturing PMI, May: 46.9 vs. 48.0 exp.

UK: Services PMI, May: 55.1 vs. 55.3 exp.

US: Manufacturing PMI, May: 48.5 vs. 50.0 exp.

US: US Services PMI, May: 55.1 vs. 52.5 exp.

US: New home sales (k), Apr: 683 vs. 665 exp.

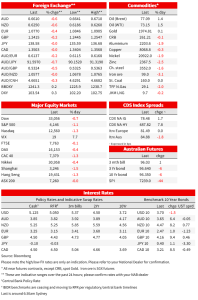

Debt ceiling negotiations grind on. President Biden called the talks ‘productive’ but there is no deal yet. Speaker Kevin McCarthy told Republicans that the two side were “not anywhere close” to a deal. The lack of progress on the debt limit as the calendar continues to march towards the nominated early June x-date weighed on risk sentiment. US equities were lower, while the US dollar was stronger.

McCarthy presented spending cuts as the sticking point, telling reporters that Democrats “still want to spend more money this year than they did last year…That’s the red line,” but did say he believes a deal can be done by 1 June. Republican negotiator Patrick McHenry said the White House must agree to cut spending levels in 2024 rather than just freeze them. Adding to the calendar pressure, McCarthy said he would not waive a rule that allows House lawmakers 72 hours to review legislation before a vote. Senate Republican leader McCarthy said “ Regardless of what may be said about the talks on a day to day basis, the president and the speaker will reach an agreement.” The Washington Post reported Treasury has asked federal agencies whether they can delay upcoming payments.

Equities were lower across markets. In the US, the S&P500 slipped 1.1%, led by Materials, IT, and Communication Services, but with all sectors except energy in the red. Oil prices are up over 1% after Saudi’s Energy Minister fired a warning shot against speculators ahead of the next OPEC+ meeting, “I would just tell them: Watch out.” The Nasdaq fell 1.3%. In Europe, the Euro Stoxx 50 lost 1.0%.

Yields were generally little changed. US 10yr yields were 2bp lower over the day at 3.70%, retracing earlier gains alongside the selloff in equities in the US afternoon. US 10yr yields had earlier reached a high of 3.76%, a fresh 2-month high. German 10yrs were 1bp higher at 2.47%, while the UK 10yr yield rose up 9bp to 4.16% after reaching 4.19% intraday, its highest level since October 2022 following the “mini” Budget of then-chancellor Kwasi Kwarteng.

The USD is broadly stronger, up 0.3% on the DXY. While higher oil prices have supported CAD, the NZD and AUD have underperformed against the backdrop of weaker risk appetite and lingering concerns about China’s economy that continue to weigh on the yuan, with USD/CNY sustaining a break above 7.05. The AUD is down around 0.6% to just over 0.66.

May flash PMIs were the highlight of the data calendar. Overall, the recent story of robust services and contracting goods persists. The Eurozone services PMI slipped marginally to 55.9 from 56.2, but remained firmly in expansionary territory, led by the jump to 57.8 from 56.0 in Germany. In contrast, manufacturing dipped to a 36m low of 44.6. Overall prices charged moderated to their slowest in 25 months but remained elevated. But while goods prices fell for the first time since September 2020, services prices accelerated in May with firms citing higher pricing power amid high demand and higher wage costs. For the US, the Services PMI rose to 55.1, the recent rise contrasting the slowing in the closer watched ISM in March and April. The key question going forward is whether manufacturing is providing the usual cyclical leading indicator that services will come down to earth under the weight of cumulative policy tightening and high inflation, or whether the weakness across manufacturing is a hangover from the desynchronised goods and services cycles over the pandemic period and the divergence can persist.

Separately, US new home sales rose to their highest level in over a year, supported by limited inventory in the existing homes market. The data support improving US residential construction activity.

BoE Governor Bailey spoke alongside colleagues in Parliament. Bailey conceded there were “big lessons” from recent experience about how to operate policy in a world of uncertainty. As for the current juncture for policy, he didn’t give away much (“I can’t tell you that we’re near to the peak or at the peak, but we’re nearer to the peak ”) but did say that inflation has “turned a corner” and that services inflation is tracking “more or less as we thought in Feb.” Bailey said that “If evidence of more persistent pressures, then further tightening in monetary policy would be required.” BoE communication has put the onus on the data to push the BoE further, whereas markets continue to price more from here as the default, pricing Bank Rate to get up to 5% from its current 4.5%, and a near 90% chance of a June hike. UK Inflation data today is expected to fall from 10.1% to 8.2% on energy base effects, with the shape of core inflation (expected unchanged at 6.2%) and services inflation in focus for policymakers.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Currency strategy to achieve a better outcome for idle cash that may be awaiting deployment and earning little or no returns

Article

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Newsletter

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.