Our monthly transaction data suggest spending ticked up in April after a stagnant performance last month

Insight

Brent oil prices are down 17% since 14 June and have the potential to drive some welcome relief on headline inflation prints.

https://soundcloud.com/user-291029717/oil-dives-bonds-rally-as-recession-fears-grow?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

The US returned from the Independence Day holiday Monday to renewed recession fears. Today’s iteration has had a more distinctly European flavour, with the mood souring noticeably around the European open and overlayed with fresh energy concerns on the continent as oil workers in Norway launched a strike that threatened gas supplies. European equity markets are lower, the US dollar stronger, especially against European currencies, and commodities are sharply lower led by oil.

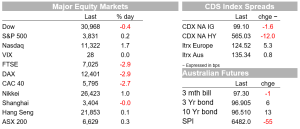

An early more positive tone helped by media speculation that sometime this week Biden would rollback tariffs on some Chine imports turn sharply around the European open. In equity markets, the EuroStoxx 50 was 2.7% lower, with other European bourses similarly in the red. US equities took their early lead from Europe at the open but staged a recovery through the day. The S&P500 managed to close in the green, up 0.2%, with the Nasdaq shedding earlier losses to be 1.8% higher. The Dow lost 0.4%. The claw-back in equities across the US session was not mirrored in rates or FX moves, with the US dollar holding onto most of its gains.

Oil prices reflected the renewed slowdown concerns as expectations for softening demand won out against a fundamentally tight supply backdrop. Brent was 9.3% lower to US$103.0 and WTI was 8.1% lower and sub $100 a barrel at US$99.62. Getting some headlines was a note from Citigroup strategists saying that crude could fall to US$65 this year in the event of a recession. Brent oil prices are down 17% since 14 June and have the potential to drive some welcome relief on headline inflation prints. Pump prices in the US were near $4.80 on Sunday after easing for 21 consecutive days from a mid-June record above $5 a gallon. Copper was also softer, down 4.2% to a new 19-month low.

Gas prices, however, ran against the grain. European gas prices surged to a four-month high as oil workers in Norway launched a strike due to a dispute over wages . Three gas fields have been shut in strikes that began Monday evening. were shut and there are plans to shut more down. The strike has reduced Norway’s gas exports by only 1% so far, but the Norwegian Oil and Gas Association said that this could rise to 56% by the weekend, which would hit exports to the UK as well as the EU. Europe has turned to Norway, traditionally its second-biggest gas supplier behind Russia as it rushes to fill storage ahead of winter. News in the past couple of hours is that Norway’s government has proposed a compulsory wage board to resolve the dispute. “The parties have said that they will end the strike so that everyone can return to work as soon as possible,” according to the Ministry of Labor and Social Inclusion.

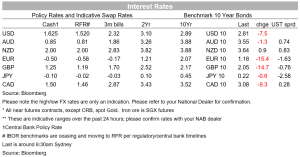

The energy crisis overlay could explain the more bearish tone evident in Europe. The euro lost 1.5% against the US dollar. FX moves were in the vanguard, the euro’s decline (or indeed the dollar’s strength against most G10 currencies) taking hold ahead of the rollover in equities. The euro reached a low of 102.35, a near 20-year low, and is currently around 1.0265. The heightened risk to the euro-area economy from curtailed gas supplies is clear, with the next key date now July 20/21 for whether gas supplies return to ‘normal’ after scheduled maintenance on the Nordstream gas pipe into Europe from Russia is due to end. These risks aren’t new, and NAB’s FX Strategy team’s view has for many months now been that the euro will see parity with the USD before year end.

Reflecting those same themes, declines against the dollar among G10 currencies were led by the Scandinavian currencies, with the NOK down 2.2%. The US dollar was earlier up 0.5% against the yen in Asia, but is flat over the day as the risk off dynamic took hold. The AUD was 1.0% lower at 0.6798, after hitting a fresh 2-year low of 0.6762; Friday’s low of 0.6764 not lasting long. The US dollar is 1.3% higher on the DXY and at 106.5 hit a new 2-decade high.

In keeping with recession fears, yields were lower globally. The German 10yr was off a 15bp to 1.18%, while gilt yields showed a similar fall, down 15bp to 2.05%. Higher US yields seen in the Asian trading session reversed and the curve flattened. The US 10yr yield was 7bp lower to 2.81%, after reaching as high as 2.98% earlier and the 2yr 1bp lower to 2.82%. The 2s10s curve back to inversion, although only just.

The RBA yesterday increased the cash rate target by 50bps to 1.35% as widely expected. There was also little change to the concluding paragraph which continues to note “the Board expects to take further steps in the process of normalising monetary conditions in Australia over the months ahead.” And that “the Board is committed to doing what is necessary to ensure that inflation in Australia returns to target over time ”. No big surprises then from the Bank, with more rate rises clearly in the pipeline, though those looking for signs the Bank would follow the Fed in communicating a swift march into restrictive territory may have been disappointed by the addition of the comment that medium-term inflation expectations are “well anchored” and the “close attention” paid to the uncertainties about the response of household spending.

Data flow yesterday was light. Caixin’s China PMI services index, a survey which has a higher weighting to smaller firms than the official index, came in well ahead of expectations ta 54.5 in June. That mirrored strength in the official non-manufacturing PMI and points to a strong bounce back in June after activity had been earlier mired by COVID restrictions. But in a timely reminder of the fragility of the current settings in China, Shanghai started mass testing in nine districts after detecting cases on Sunday and Monday, while Xi’an started seven days of control measures, including school and restaurant closures. In other news, in the UK, key members of Prime Minister Boris Johnson’s cabinet resigned. Johnson has reportedly vowed to stay on and would replace Chancellor of the Exchequer Rishi Sunak and Health Secretary Sajid Javid possibly as soon as Tuesday.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our monthly transaction data suggest spending ticked up in April after a stagnant performance last month

Insight

Conditions, employment fall back to long-run average

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.