Looking for Analogs

I have been digging to see how things have played out in the past when presented with the current set-up. As you might expect, pandemic lockdowns, supply constraints, fiscal spending, and massive monetary accommodation topped off with a huge jump in inflation, ensures that there are few analogs to look at.

When, over the last 40 years, have we seen a meaningful synchronized move higher in oil, the dollar, and 10-year yields? Not often, and not of this magnitude across all three asset classes. In theory, this should be a toxic mix that taxes consumption, raises borrowing costs, and shrinks global liquidity.

Since we have now entered a regime in which markets are more worried about inflation than growth (growth being the main worry in a disinflationary environment), we really need to go back to before the Asian Crisis and the Russian default in the late ‘90s to find a world concerned with inflation.

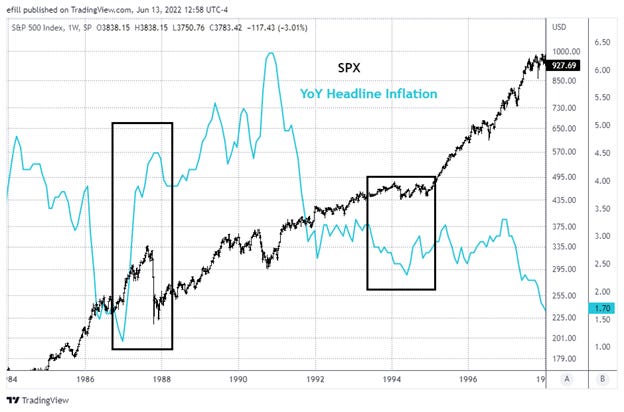

There were two periods in the late ‘80s and early ‘90s that stand out as also having a large jump in Treasury yields. Interestingly, the two periods saw very different outcomes for equities.

During the summer and fall of ’87, stocks and yields rose together until equities suffered a large drop which then also reversed the rise in yields. On the other hand, the brutal rise in yields in ’94 had a very different outcome, only putting equities into a year-long range that they then broke out from as soon as yields rolled over. Note, that in both these cases higher inflation and higher yields went hand in hand with a weaker USD, unlike this time. I would argue that the strong dollar this time around is more destabilizing, not less.

A key difference appears to be the magnitude of the inflation rise that accompanied the rising yields and the degree to which the Fed was “behind the curve” at the time.

Inflation during the two periods…

And with Fed Funds added…

Analogs are never perfect and the late ‘80s / early ‘90s were still feeling the effects of Reaganomics in a world that was far less globalized than today. However, one could argue that with the current trend towards de-globalization we are heading back in that direction. Does Reaganomics have parallels in the COVID response?

In any case, as we navigate the current inflation regime it might be better to reach back to the ‘70s, ‘80s, and ‘90s for historical presidents, rather than the events of the last twenty years.