RBNZ meeting preview: Let the hiking begin

We expect the Reserve Bank of New Zealand to hike rates by 25bp at its 18 August meeting, and see at least one more hike by year-end. Such a move has been fully priced in, and much of the market reaction will likely depend on the forward guidance on future tightening. We think NZD still has significant room to benefit from the RBNZ's hawkishness in 2021

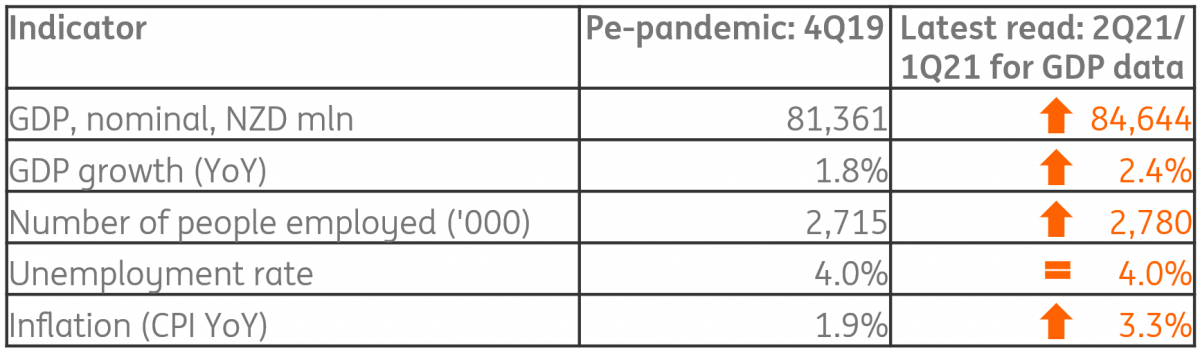

Reasons for ultra-low rates have faded

The New Zealand economy has been on a very solid recovery path in 2021 after having faced a double-dip recession in 2020. As of now, most indicators suggest that the Kiwi economy is no longer suffering from the negative impact of the pandemic, as shown in the table below, and is instead facing above-target inflation like many other countries.

The release of 2Q employment data were, in our view, the last piece of data the RBNZ needed to start its hiking cycle. With unemployment dropping to where it was before the pandemic hit (4.0%), there is a rising risk that inflationary pressures may be more persistent than what is implied in recent communication by the central bank.

Another factor that remains in our view absolutely crucial is the housing sector, which has experienced bubble-like inflation in the past two years. Despite the government’s efforts to discourage speculative real-estate investments, recent data indicate house prices have continued to rise. In July, housing inflation was still at 25% year-on-year.

The New Zealand government has made house affordability a central theme in its political agenda, and changed the RBNZ remit in February to include housing considerations. While the RBNZ may well continue to exclude house prices from the explicit reasons why it has started tightening monetary policy – with the aim of preserving its notion of independence – we still believe this has been (and will likely continue to be) a key factor in policy decisions.

We expect a 25bp hike in August, and at least one more by year-end

In light of the economic developements highlighted above, we expect to see a 25 basis point rate hike on 18 August from the RBNZ, and we forecast at least another one of the same magnitude by the end of the year (more likely in November rather than October), as data should continue to show signs that the Kiwi economy is indeed overheating.

We doubt that the recent flare-up in Covid-19 cases in the APAC region (where vaccination rates are generally lower than in North America and Europe) and the related risks of a slowdown impacting New Zealand are tangible enough at this stage to make the RBNZ refrain from starting to hike rates.

Markets fully pricing in hikes, but NZD can profit from carry in the longer-run

The OIS (overnight index swap) market show that investors have already fully priced in a 25 basis point rate hike in August, another one in November and two more in the first half of 2022, for a total of 100bp of tightening from the current 0.25% OCR rate.

Much of the market reaction at the 18 August meeting will depend on the RBNZ’s forward guidance

With this in mind, much of the market reaction at the 18 August meeting will depend on the RBNZ’s forward guidance. The Bank will release the Monetary Policy Statement, where it will include an update of its projected rate path. In the latest release (in May 2021), policymakers were forecasting no rate hikes before 2H22.

As shown in the chart above, rate expectations in New Zealand have jumped significantly in the past month, firstly thanks to a hawkish RBNZ meeting on 14 July – where the end of the asset purchase programme was announced – and then thanks to very strong inflation and employment numbers for 2Q21.

This re-pricing has allowed NZD to be the only G10 currency to resist USD appreciation in the past month, but the rise in NZD/USD has been very contained (+0.3% in the past month) considering the meaningful monetary policy divergence between the RBNZ (that ended asset purchases in July) and the Fed (that still has to start tapering).

We suspect that the NZD is still far from having fully benefitted from the higher RBNZ rate expectations, as a generalized risk-off sentiment – especially in China, to which NZD is highly sensitive – and the further unwinding of reflation trades acted as offsetting factors.

With the RBNZ hiking twice in 2021 in our estimates, NZD would have the most attractive carry in G10. However, the currency will continue to struggle to benefit from its attractive yield so long as the market sentiment on the global recovery (and in particular in Asia) remains choppy at best. We are still inclined to think global sentiment will enjoy some stabilisation in the fall months, which should allow at least a partial resurgence of carry/reflation trades. In such an environment, NZD – backed by the RBNZ tightening cycle – should emerge as a key outperformer in G10, and we target 0.74 in NZD/USD for 4Q21.

We target 0.74 in NZD/USD for 4Q21

In terms of the market reaction to the August meeting, we think that the upside for NZD may be contained as the hike is fully in the price and the rate-path projections by the RBNZ may fall short of fully endorsing the markets' very hawkish pricing. Still, recent data on FX positioning suggest that the NZD is no longer an overbought currency, and this means that the room for a post-RBNZ meeting profit-taking event in NZD do not look very likely if the Bank actually delivers a rate hike and signals more will come.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more