Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Newsletter

Talks at averting another US government shutdown ended in deadlock at the weekend.

https://soundcloud.com/user-291029717/wall-talk-stumbles-brexit-can-kicked-further

One way or another, I’m gonna find ya, I’m gonna get ya, get ya, get ya, get ya , One way or another, I’m gonna win ya….Blondie

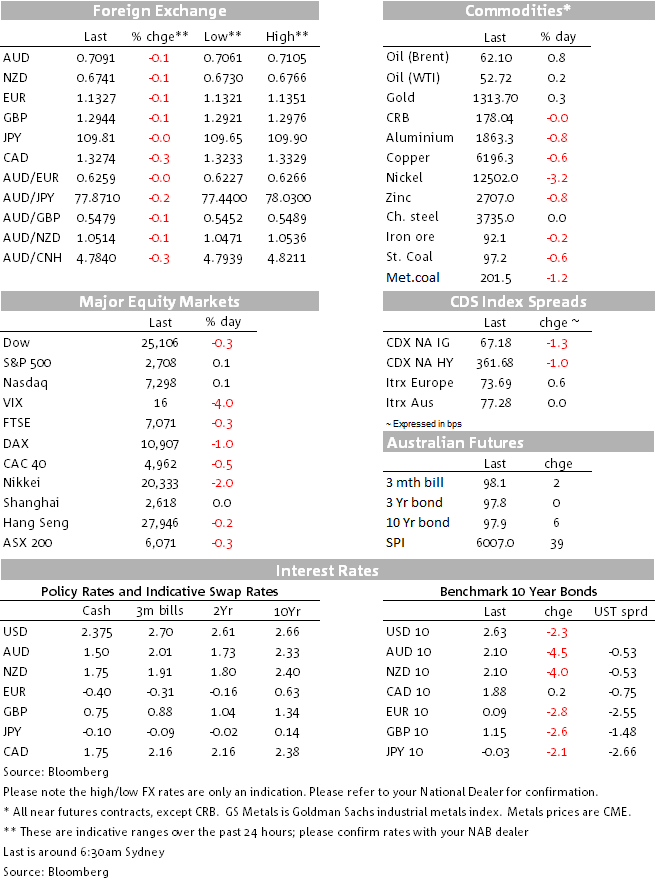

Markets closed Friday in a cautious mood reflecting a change in sentiment following Thursday’s confirmation by President Trump that he will not meet President Xi before the March 1st tariff deadline. News the US Administration is considering three options for EU car tariffs didn’t help the equity market in Europe while US equities ended the week essentially flat with the last hour of power saving the day. The USD continues to win the least ugly contest, up for a seventh consecutive day, CAD was the big winner in G10 FX after a very solid jobs print and the AUD recovered a bit of lost ground post the SoMP decline. Weekend news confirmed China-US trade talks will take place Feb 14-15 while US border talks to avoid another Government Shutdown hit an impasse. ON Saturday Trump tweeted ” Wall Coming One Way or the Other’ implying the declaration of a ‘national emergency’ to secure wall funding remains an option.

After we went home on Friday Asian equities closed the week weaker across the board, reflecting an increased level of apprehension on whether or not the US and China can find an agreement to deescalate their trade tensions ahead of the March 1st deadline. European equities traded sideways at the opened but then news that US Administration was considering three types of tariffs on European cars sour the mood. According to Germany’s Wirtschaftswoche magazine, the three options are(1) 10% rate; (2) 25% rate; (3) or specific customs duties limited to technological advanced cars and components such as electric vehicles. All major EU equity indices closed Friday in negative territory with the STX Europe 600, down -0.56%.

US equities were heading for a negative close on Friday with the S&P500 down ~0.90% at one point before staging a recovery later in the session with the move up accelerating in the last (power) hour of trading. The Dow closed in negative territory (-0.25%), but it still managed to record its seventh consecutive weekly gain. The S&P 500 rose 0.07%, to 2707.88, while the Nasdaq Composite added 9.85 points climbing 0.14% to 7298.20. The S&P 500 and NASDAQ also closed higher for the week. There was no obvious trigger for the turn-around in US equities, although some commentators cited comments by San Francisco Fed President Mary Daly, who raised the possibility of using QE as a more regular policy tool, as helping to boost the market. Daly said “you could imagine executing policy with your interest rate as your primary tool, and the balance sheet as a secondary tool, but one that you would use more readily”, although she added that no decision had been made

US led trade uncertainty along with increasing concerns over the extent of the current global growth slowdown has seen an increase in demand for core global bond. On Friday 10y Bunds led the move lower in yields, a part of the ongoing concerns over the state of the European economy, Italy’s fiscal position is also a growing worry, evident by the 36bps rise in 10y BTPS yields on the week (now at 2.95.5%). The threat of US tariffs on EU cars, didn’t help sentiment either with 10y Bunds trading down to an intraday low of 0.078% before closing at 0.087%. Meanwhile the UST curve bull steepened with the 2y rate declining 4.4bps to 2.482% while 10y UST’s closed at 2.636% ( 3.8bps lower on the day).

Against a backdrop of uncertainty and despite a Fed that is comfortably on hold, the USD continues to win the least ugly contest, up for a seventh consecutive day. The USD also closed the week broadly stronger with both DXY and BBDXY up almost 1%. That said, it was not all one way for the USD on Friday, the CAD was the G10 outperformer boosted by a much better than expected January labour market report. The Canadian unemployment rate ticked up, due to an increase in the participation rate, but wage growth was also higher than expected (see details below).

The AUD closed Friday at 0.7088, down 0.18% on the day. The aussie staged a mini recovery during Friday’s overnight session following an intraday low of 0.7061 immediately after the release of the SoMP during our morning on Friday. The market was seemingly surprised by the forecast downgrades which had already been flagged in Tuesday’s Statement and the Governor’s speech on Wednesday. The RBA new forecast revealed a hefty GDP growth downgrade of 2.5% over the year to June 2019 vs 3.5% previously. So the RBA expects a growth slowdown into the first half of 2019 followed by a pickup thereafter taking the 2019 growth to 3%.

One factor that may have contributed to the small AUD recovery can be attributed to the soaring iron ore price. Against a backdrop of soft commodity prices ( Brent -1.7% and WTI -2.54, copper -0.28%), iron ore prices have continued to climb reaching $94 during the Asian trading session – the highest level in 4½ years. China is back from holiday’s today and it will be interesting to see whether China’s iron ore prices reflect a similar jump.

Meanwhile the NZD traded a relatively tight range on Friday, consolidating after the sharp fall in the wake of the disappointing NZ employment report on Thursday. It closed the week at 0.6745.

Over the weekend we had confirmation China-US trade talks will take place Feb 14-15 and we have also had mixed reports in terms of the border negotiations between US Republicans and Democrats. Late on our Friday negotiators signalled they were close to reaching a compromise spending package suggesting a number between $1.3bn to $2bn was in the offing. This is clearly well below the $5.7bn demanded by President Trump. Not surprisingly and in a sign of defiance, on Saturday President Trump tweeted the ” Wall Coming One Way or the Other’, implying the declaration of a ‘national emergency’ to secure wall funding remains an option. Speaking to the media overnight, Mick Mulvaney, the acting White House chief of staff, said “You cannot take a shutdown off the table, and you cannot take $5.7 (billion) off the table,”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Newsletter

We see our NAB commodity index falling substantially in 2024, despite higher forecasts for base metals and gold.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.