Hi all,

Before you go on, let's keep an open mind.

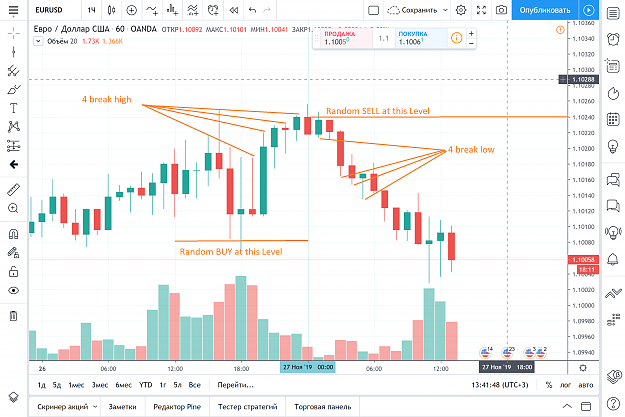

Here's a thought experiment. We like to talk about how edges decay over time (some swear by an average of 3 years before the efficacy of a strategy falls).

What if all trades were entered at random and all you could control is the exit strategy? A system based in random entries has to no edge to speak of, so by that logic, there is no edge to decay.

But how would you trade it?

I've been dabbling with this wild thought for a while now and wanted to see if there is a like-minded individual who wants to discuss this audacious experiment.

If there isn't enough interest in this area, I shall take my work elsewhere.

All ideas are welcome.

Before you go on, let's keep an open mind.

Here's a thought experiment. We like to talk about how edges decay over time (some swear by an average of 3 years before the efficacy of a strategy falls).

What if all trades were entered at random and all you could control is the exit strategy? A system based in random entries has to no edge to speak of, so by that logic, there is no edge to decay.

But how would you trade it?

I've been dabbling with this wild thought for a while now and wanted to see if there is a like-minded individual who wants to discuss this audacious experiment.

If there isn't enough interest in this area, I shall take my work elsewhere.

All ideas are welcome.