-

Fed's Williams: I'm not declaring victory over inflation, but I see progress

— Breaking Market News (@financialjuice) October 18, 2023 FED'S WILLIAMS: I'M NOT DECLARING VICTORY OVER INFLATION, BUT I SEE PROGRESS.

FED'S WILLIAMS: I'M NOT DECLARING VICTORY OVER INFLATION, BUT I SEE PROGRESS.

-

— Breaking Market News (@financialjuice) October 18, 2023 FED'S WILLIAMS: STILL HAVE A WAYS TO GO GETTING INFLATION BACK TO TARGET.

-

FED'S WILLIAMS: PATH OF MONETARY POLICY DEPENDS ON THE DATA #News #Markets #live

— Capital Hungry (@Capital_Hungry) October 18, 2023

-

— Breaking Market News (@financialjuice) October 18, 2023 FED'S WILLIAMS: THE FED NEEDS RESTRICTIVE MONETARY POLICY FOR A WHILE TO COOL INFLATION.

- Comments

- Subscribe

-

- Older Stories

From @DeItaone|Oct 18, 2023

From @DeItaone|Oct 18, 2023post:

WALLER: NO ONE EXPECTS ANY KIND OF RATE CUT SOON post:

WALLER: NO ONE EXPECTS ANY KIND OF RATE CUT SOON post:  FED'S WALLER: WE NEED TO SEE HOW INFLATION PROGRESSES IS IN 6-12 MONTHS, THEN SEE ABOUT CUTTING RATES. post: FED'S WALLER: IF WE SAW INFLATION COMING DOWN TO 2.5%, THE TAYLOR RULE WOULD SAY TO CUT RATES.

FED'S WALLER: WE NEED TO SEE HOW INFLATION PROGRESSES IS IN 6-12 MONTHS, THEN SEE ABOUT CUTTING RATES. post: FED'S WALLER: IF WE SAW INFLATION COMING DOWN TO 2.5%, THE TAYLOR RULE WOULD SAY TO CUT RATES. From think.ing.com|Oct 18, 2023

From think.ing.com|Oct 18, 2023Market expectations for the upcoming Bank of Canada policy meeting have fluctuated quite a lot since the last policy meeting on 6 September when it left rates on hold at 5%. Back ...

From federalreserve.gov|Oct 18, 2023

From federalreserve.gov|Oct 18, 2023Thank you, Professor Scobie. Thank you to the European Economics and Financial Centre for inviting me to speak and for the honor of referring to me as a "distinguished speaker." I have noticed that people started calling me "distinguished" only after my hair turned white. I suspect that "distinguished" is a polite way of saying you are old. My subject today is one I trust is of interest in this center of global finance—namely, the outlook for the U.S. economy and the implications for monetary policy.1 It has been one year and seven months since the Federal Reserve began raising interest rates to rein in inflation, and there has been considerable progress. But uncertainties remain, both about the forces that will shape the economic outlook in the coming months and about whether monetary policy has reached a level that is sufficiently restrictive to support continued progress toward the Federal Open Market Committee's (FOMC) target of 2 percent inflation. Let me share my thinking about what recent economic data can, and in some cases, cannot tell us about the outlook and the appropriate setting for monetary policy. The data in the past few months has been overwhelmingly positive for both of the FOMC's goals of maximum employment and stable prices. Economic activity and the labor market have been strong, with what looks like growth well above trend and unemployment near a 50-year low. Meanwhile, there has been continued, gradual progress in lowering inflation, and moderation in wage growth. This is great news, and while I tend to be an optimist, things are looking a little too good to be true, so it makes me think that something's gotta give. Either growth moderates, fostering conditions that support continued progress toward our 2 percent inflation objective, or growth doesn't, possibly undermining that progress. But which is going to give—the real side of the economy or the nominal side? I find myself thinking about two possible scenarios for the economy in the coming months. In the first, the real side of the economy slows. This is the scenario broadly reflected in the September Summary of Economic Projections (SEP) by FOMC participants, w post:

WALLER: TOO SOON TO TELL IF MORE POLICY RATE ACTION IS NEEDED WALLER: MORE ACTION ON POLICY RATE WOULD BE NEEDED IF DEMAND, ECONOMIC ACTIVITY KEEP UP RECENT PACE post: WALLER: IF REAL ECONOMY SLOWS, CAN HOLD POLICY RATE STEADY #News #Markets #live post: Fed governor Chris Waller blesses a November pause: After that, if growth cools along the lines of the Sept SEP, then stay on hold But if strong demand stalls recent progress on inflation, failing to respond "in a timely way” risks “unwinding the work that we have done to date" pic.twitter.com/EYJPsUWwZr

-

- Newer Stories

From cnbc.com|Oct 18, 2023|4 comments

From cnbc.com|Oct 18, 2023|4 commentsFederal Reserve Governor Christopher Waller on Wednesday indicated the central bank can afford to hold off on interest rate increases while it watches progress unfold in its ...

From federalreserve.gov|Oct 18, 2023|8 comments

From federalreserve.gov|Oct 18, 2023|8 commentsThank you, Tom. It is a pleasure to join you to take part in today's conversations.1 When we started Fed Listens back in 2019, the initiative was part of a broad, comprehensive review of the decisionmaking framework we use to pursue our monetary policy goals of maximum employment and price stability. We met with people across the country from a wide range of backgrounds and perspectives, and we learned a lot about how our monetary policy actions affect them, their businesses, and their communities. In light of the valuable insights we gained in those original listening sessions, we decided to expand the scope of Fed Listens to become an ongoing process of consultation with the public. I look forward to learning from the perspectives of today's participants, our panelists, as well as those of you in the audience. Through Fed Listens and other Board and System convenings, we are able to gain important insights about economic conditions by engaging directly with those experiencing the economy. Your views and experiences supplement the economic data that we monitor, providing important color and context. These discussions help us gain a deeper understanding of the ongoing burden from high inflation—from the considerations for families in making spending decisions to the f post:

BOWMAN SAYS INFLATION HAS COME DOWN, BUT IT IS STILL TOO HIGH post: FED'S BOWMAN: THE STRENGTH IN GOODS SPENDING HAS BEEN SURPRISING. From zerohedge.com|Oct 18, 2023

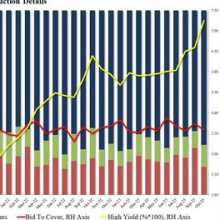

From zerohedge.com|Oct 18, 2023After last week's catastrophic 3/10/30 year auction and following today's latest blow out in yields that pushed the 10Y to 4.92%, it's safe to say that not many were looking with ...

- Story Stats

- Posted: Oct 18, 2023 12:37pm

- Submitted by:Category: Low Impact Breaking NewsComments: 0 / Views: 3,294

- Linked event: