{quote} Responding to demand and creating demand for useless or unattainable things are two completely different things. The bullshit that is peddled in this industry is much like the bullshit peddled in the fashion industry who take the most beautiful women in the world and then airbrush their photos. What they are creating demand for is unattainable - it doesn't exist.

Ignored

Same phenomenon, different take on personal agency.

Quote

Disliked

I don't believe it has always been this way. For one, they didn't have the avenues such as TV and the internet to constantly bombard the public. But if that is all it was, bombardment, then that would be fine. But the study of phsychology has come a long way and marketing leans heavily on this. The colours, sounds, playing on peoples fear, greed, need to fit in etc. Hugely profitable companies spending huge portions of their revenue to create demand for useless crap and quests that can never be satisfied, at least not by the solutions they offer....

It has always been this way. Even as early as the 1900s bucket shops would still find ways to provide their services despite being illegal.

Given that once I am committed to a trade the price can do anything, the only thing that matters is the account.

Once I have money on a trade, it's the money that matters and not the price action.

{quote} Given that once I am committed to a trade the price can do anything, the only thing that matters is the account. Once I have money on a trade, it's the money that matters and not the price action.

Ignored

I thought that's what you were getting at. This is another cardinal sin according to the gurus that can actually work quite well. It helped me enormously when I turned away from the "trade the market, not your account". But I think it is a psychological edge more than anything else. We are not robots and psychological edges can be some of the most profitable. The more flexible and discretionary your trading is, the more they can help. I was just reading a good thread that uses this philosophy. http://www.forexfactory.com/showthread.php?t=549608

It is interesting you mention this though as I have been trying to move away from it a bit more over the past few months. Once I get a read on the market, I open a trade. Once I lose the read or get a read that suggest the opposite, it is time to exit. I have not been having much success really though as emotional responses are clouding my judgement more without the BE stop, taking quick partial profits after a few pips etc, but I believe that if I can master it I will increase profits. We will see

Painstakingly calculating your RR when it is positive gives you that warm and fuzzy feeling that may be you are onto something... only to be proven very wrong after the next trade or two. RR was created by Mr. Tharp so that he could sell books and speaking engagements... How can you be certain or your risk-reward ratio when the outcome (reward) is a random event?. The risk can be known but never the reward. Therefore you can never rely on the current expectancy for the future. Mr. Tharp's work has the appearance of solid math and logic but is totally...

Ignored

Hard to make people accept that their reward is a random variable. When a trader uses a fixed SL his risk is still a random variable because of slippage, gap, flash crash, low liquidity widening the spread... Try and convince a trader that his winrate is again a random variable too because it is impacted by the future market condition and he will still refuse to accept that the logical conclusion is that his equity curve is a random walk; hopefully with a positive drift.

Tharp's work is correct. He just over-simplified to a simple WIN R or LOSE ONE outcome to make things easy to understand for everybody. Sure in real life it is a lil' bit more complex. But I'm sure his message would have certainly not been understood if he used integrals of integrals of unknown probability distributions over latent variables.

People have a big hurdle with probabilities. Imagine when you explain that some probability itself is random... Now you lost 99% of your audience explain the few people left that those unknown probabilities of probabilities are changing over time... randomly and people start throwing you things at.

Well, well... we are getting more stuff in here and I like diversity.

@alphaomega

Quote

Disliked

For example the major pairs 10 years ago use to be a little bit more quiet with more stable trends. Now the days are crazy with all that algo trading and HFT going on. Even during "quiet" times prices are changing 20-30 times per sec. on most ECNs.

So do you think it's a good thing that the market is filled with more participants and a lot of inefficiencies on micro time frame or what?

Yes, I think crash is something we simply can't avoid. It is bound to happen every now and then.

@Agro

Quote

Disliked

Exactly. It is the way things are marketed these days. Much of modern marketing targets the lazy (or perhaps just time constrained) and instant gratification seeking behaviour that is prevalent in our societies. ...

The one easy fix that is the answer to all your dreams.

I think the marketing around the trading industry is more amplified in this aspect than most other industries.

Most of the time it's for the ones seeking short cut and then those with time constraints.

It is especially true because forex deals with money and direct profit (or direct loss) so people created a super hyped up ads specifically to attract people in seconds.

@Atokys

Quote

Disliked

Its the same today as it was a hundred years ago with bucket shops. Its not the fault of modern marketing or brokers. They are simply responding to a demand. People tend to have biases that lead to sabotage when confronted with the nature of markets. The game of speculation is as old as the hills and so is human nature.

Can't deny that. Nothing's really new when it comes to human nature.

@Mingary

Quote

Disliked

How can you be certain or your risk-reward ratio when the outcome (reward) is a random event?. The risk can be known but never the reward.

Yes, I agree.

It is true for those who don't put TP on a trade but what do you think about those who limit their TP such as directly putting 1:3 RR.

Quote

Disliked

Given that once I am committed to a trade the price can do anything, the only thing that matters is the account.

Once I have money on a trade, it's the money that matters and not the price action.

I was about to ask about that "account based" thing but somebody else already did. Good explanation.

@PipMeUp

Quote

Disliked

Tharp's work is correct. He just over-simplified to a simple WIN R or LOSE ONE outcome to make things easy to understand for everybody. Sure in real life it is a lil' bit more complex. But I'm sure his message would have certainly not been understood if he used integrals of integrals of unknown probability distributions over latent variables.

People have a big hurdle with probabilities. Imagine when you explain that some probability itself is random... Now you lost 99% of your audience explain the few people left that those unknown probabilities...

Some people who rejected the idea might later come to realization of the difficult things he heard or read long ago. Sometimes it's just a matter of seeing it over and over again.

The poll on the 1st page showed more participant and that's good!

We have preference and we have reasoning behind it.

This is what it means to have a strong community

Poll, poll, poll ok?

Different/opposing ideas will make us learn and understand many things.

@alphaomega {quote} So do you think it's a good thing that the market is filled with more participants and a lot of inefficiencies on micro time frame or what?

Ignored

It's good for the people who know how to take advantage of these inefficiencies, and it's bad for the trend followers and longer term strategies.

You see, the thing is that these inefficiencies on the micro time frames are sitting below the radar of the big players. They just can't take advantage of them because the liquidity is not enough for them. You cannot scalp for 5 pips when you move hundreds of millions. But for the small traders who know what they are doing this is excellent opportunity. When heavy hitters trade, their orders impact the market, and create temporary inefficiency on the micro scale. That's why prices move up and down all day long even when there is no change in the fundamental picture. Over 80 % of the days are ranging with no crear direction. The market does up, down, up, down, up down....... and finishes the day in the middle of the range. Naturally on the micro scale almost all trends and breakout fail and the price reverts to the mean. And this pattern persist until major news hits the wires, that causes major shift in the perception of the crowd. Then the market starts to trend to find the new "fair value area".

For zero expectancy: randomly buy or sell at fixed time of day, stop 70 pips * multiple, target 30 pips * multiple, target win % is 70% but will vary more when trade count is low.

(Where stop/target multiple is m )

For positive expectancy, buy / sell when price is above/below moving average of length x, use 70m pip stop, 30m pip target. Stop/target numbers can be switched and there are also positive values with approximately 30% wins. To somewhat increase avg profit per trade, require price to be y pips above/below average to buy/sell. Don't allow reversals, just close trade on stop/target.

This is just an example I whipped out in R in a few minutes, not one of my models. Is this a good model? Probably not. Is this model easy to understand and implement - yes.

Its a combination of both. Most importantly, its all depends on Money management. whether you are satisfied with decent consistent profits or let your greed to eat your profits.

At the end of the day, if you are in profit. Stay happy. More profit.

For positive expectancy, buy / sell when price is above/below moving average of length x, use 70m pip stop, 30m pip target. Stop/target numbers can be switched and there are also positive values with approximately 30% wins. To somewhat increase avg profit per trade, require price to be y pips above/below average to buy/sell. Don't allow reversals, just close trade on stop/target.

Ignored

I have a feeling that this may not work out to have a positive expectancy.

{quote} Hard to make people accept that their reward is a random variable. When a trader uses a fixed SL his risk is still a random variable because of slippage, gap, flash crash, low liquidity widening the spread... Try and convince a trader that his winrate is again a random variable too because it is impacted by the future market condition and he will still refuse to accept that the logical conclusion is that his equity curve is a random walk; hopefully with a positive drift. Tharp's work is correct. He just over-simplified to a simple WIN R...

Ignored

I have always questioned the logic behind the the concept of "R:R ratio". To my understanding, this approach leads to cut the profitable trades and leave the losing trades to hit the stop loss where both can be managed in more efficient way. I believe markets or random most of the time except specific conditions and that fixed R:R is meaningless to greater extend.

Joined Aug 2010

|

Status: Stare Into the Lights My Pretties!

|779 Posts

I think traders should keep in mind that looking at RR and Win rate on a trade by trade basis is not very good measure of performance. It's much more professional to measure the results on daily and weekly basis. Also, you should focus more on things like VaR(value at risk) and Return to drawdown ratio. Individual trades doesn't matter long term.

Do not try to force every trade to give you high RR. Being greedy in this game leads to destruction. Learn to take YES for an answer, and take what the market is offering right now. If it gives you 5 pips -take it! If it gives you 105 pips - take it. Don't force it, asking for more pips. And when the market says NO and goes against you - take the loss and move on.

Greed and unrealistic targets and expectations, these are the major reasons people fail in trading. Most experienced trades tend to be on the correct side of the market 8 out of 10 times, but still lose money because they chase the myth for 2:1 , 3:1.......instead of collecting their profits.

{quote} I have always questioned the logic behind the the concept of "R:R ratio". To my understanding, this approach leads to cut the profitable trades and leave the losing trades to hit the stop loss where both can be managed in more efficient way. I believe markets or random most of the time except specific conditions and that fixed R:R is meaningless to greater extend.

Ignored

First this is not an approach. Second it has nothing to do with setting a TP or not. Whatever method you use your profit/loss will always be some multiple of your risk. If you set no SL at all the risk is the loss you would get at MC.

R:R is the ratio between the AVERAGE profit you make when your trade is a winner and the AVERAGE loss you make when your trade is a loser. There is no reason for it to be fixed or pre-defined. You don't decide your R:R you estimate it from your trades journal.

Quote

Disliked

I believe markets or random most of the time except specific conditions and that fixed R:R is meaningless to greater extend.

I personally believe markets are always random and found no evidence of the opposite. Note that random and unpredictable are two different things.

Joined Aug 2010

|

Status: Stare Into the Lights My Pretties!

|779 Posts

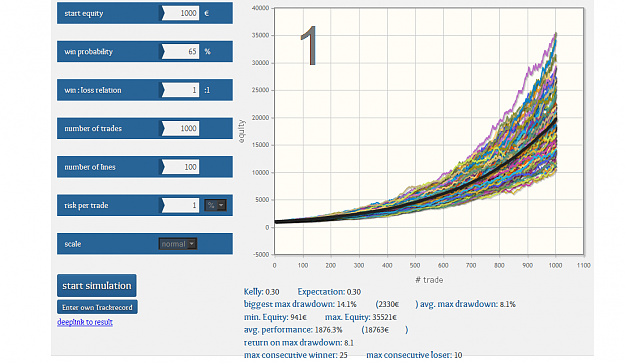

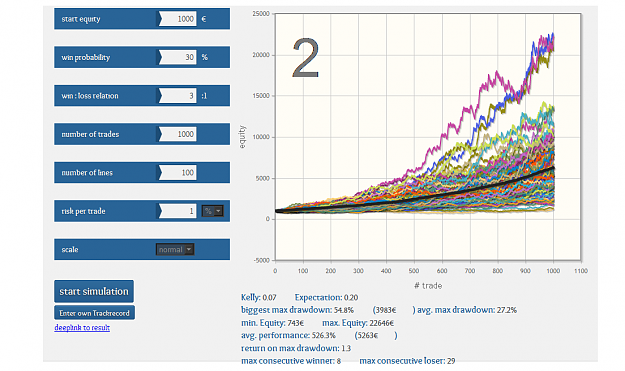

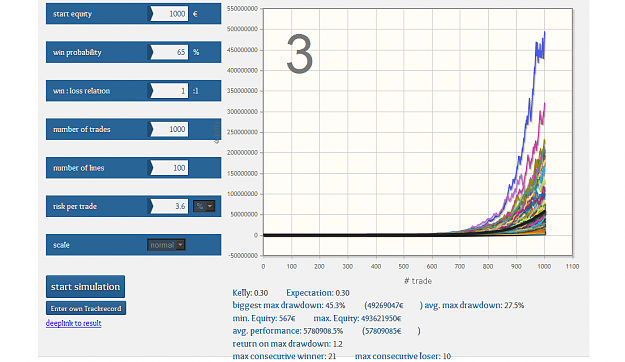

I made some simulations, Just for the sake of the argument, and to show/prove mathematically, that high Win rate is superior to high RR. Note that I am not saying which one is easier to achieve. Everyone should decide for themselves.

Simulation 1 - WR 65% , RR 1:1, risk per trade 1%

Simulation 2 - WR 30%, RR 3:1 , risk per trade 1%

Simulation 3 - Shows simulation 1 , but on risk adjusted basis with simulation 2 (with the same expected drawdown)

{quote} First this is not an approach. Second it has nothing to do with setting a TP or not. Whatever method you use your profit/loss will always be some multiple of your risk. If you set no SL at all the risk is the loss you would get at MC. R:R is the ratio between the AVERAGE profit you make when your trade is a winner and the AVERAGE loss you make when your trade is a loser. There is no reason for it to be fixed or pre-defined. You don't decide your R:R you estimate it from your trades journal. {quote} I personally believe markets are always...

Ignored

newbie here and did not get what you are saying about R:R has "nothing to do" with setting TP or SL and "no reason" for fixed or pre-defined R:R. Moreover, if you are dealing with "always" random market, it really does not matter you just decide your R:R out of thin air or "estimate from trading journal".

Yes there is a difference between random and unpredictable. exactly for that reason i do not share your believe about market being always random. Random is when no known contributing variables exist and therefore you can't predict the outcome. Unpredictable is when there is simply no sufficient information to correctly calculate the outcome. Market does have the known contributing variables and if you have access to ALL existing information, including the order flow, then you can predict the market with great extend of accuracy.

Second it has nothing to do with setting a TP or not. Whatever method you use your profit/loss will always be some multiple of your risk. If you set no SL at all the risk is the loss you would get at MC. R:R is the ratio between the AVERAGE profit you make when your trade is a winner and the AVERAGE loss you make when your trade is a loser. There is no reason for it to be fixed or pre-defined. You don't decide your R:R you estimate it from your trades journal.

Ignored

Why even record this then? If it is not an approach then it doesn't matter right? Averages don't mean a thing when there are different data sets to consider and trading is all about different data sets. One week your average R:R may be totally different to the next as it will be year on year if you are trading the opportunities that the market presents rather than forcing your rules upon the market. IMHO R:R is really only for those wishing to force their trading into a specific category.

I made some simulations, Just for the sake of the argument, and to show/prove mathematically, that high Win rate is superior to high RR. Note that I am not saying which one is easier to achieve.

Ignored

This is interesting but *almost* useless in real world application as it assumes that high R:R goes hand in hand with low win rate and vice versa which is not the case. But I assume you already know this due to your previous post and your comment 'Note that I am not saying which one is easier to achieve'.

{quote} This is interesting but *almost* useless in real world application as it assumes that high R:R goes hand in hand with low win rate and vice versa which is not the case. But I assume you already know this due to your previous post and your comment 'Note that I am not saying which one is easier to achieve'.

Ignored

Hmmm.... Show me one (just one) strategy producing high win rate combined with high RR. Just one! I bet you can't,........ because it just doesn't exist!

This is basic probability in context of markets. Mixing high win rate with high RR is like mixing oil with water. It just doesn't work no matter how hard you try!

{quote} Hmmm.... Show me one (just one) strategy producing high win rate combined with high RR. Just one!

Ignored

This. Also, I would like to see a strategy with a positive expectancy that takes profit at 1R and cuts losses at -1R. Though I suspect that these do not exist and if they do all the winners are clustered during large scale trends and using a trailing stop would have probably maximized gains.

{quote} Hmmm.... Show me one (just one) strategy producing high win rate combined with high RR. Just one! I bet you can't,........ because it just doesn't exist! This is basic probability in context of markets. Mixing high win rate with high RR is like mixing oil with water. It just doesn't work no matter how hard you try!

Ignored

If you mean by a strategy a system or signal then I can't show you that. What I could show you is an individual trade idea that has a very high probability of success with a very high R:R.