*backtest data is at the end*

Methodology:

I must first say a little about myself and my approach to trading FX, first things first, I am a an experienced programmer (I began at age 11 and am now 16),

I write my code primarily in Java, and have developed a backtesting infrastructure with data from Quandl as well as a parser to read my brokerage's historical

FX data. I follow the assumption (based on evidence) that a single asset's past prices alone cannot predict that of the future, however when external information is applied (econometrics, other asset prices and correlation, order flow/volume, as well as implied volatility) all can be used to forecast future performance. An example of a system I may develop (for explanation purposes) would be short the dollar if Non Farm is below 150k, other wise hold. Compared this to others who may use

technical indicators which I have no data suggesting they are capable of predicting the market.

Current situation:

At the moment I have two strategies trading, these are swing trading systems making trading decisions based on fundamentals, each having four hours of exposure unless I intervene due to reasons such as FOMC press conferences/speeches or other news events that causes the trade to potentially reverse. The systems do not have stops/takes because I have found that greater returns are possible without them and as well due to how I mathematically model the effect of these events on volatility. My current goals are to build a portfolio of 5 market neutral strategies all with a low correlation to one another's returns, 3-4 short term, as well as 1-2 long term. I also plan to target a sharpe ratio of 2.5 or higher. Sharpe ratio for those who don't know is mean returns divided by the standard deviation of returns. A rule I have set for my short term strategies is a max leverage of 1:10, and 1:4 for long term. My strategies are currently very low latency, with only two opportunities a week and each trading an average of 40% of weeks (this means I will make a trade 64% of weeks). Finally I expect to make at least 5% return a month and will be compounding monthly hoping for 110%-200% return a year..

Another thing to note about backtests is that there is only 3 months of 30 minute bar data on my hard drive, If anyone can get me more data that is from Oanda that would be phenomenal!!

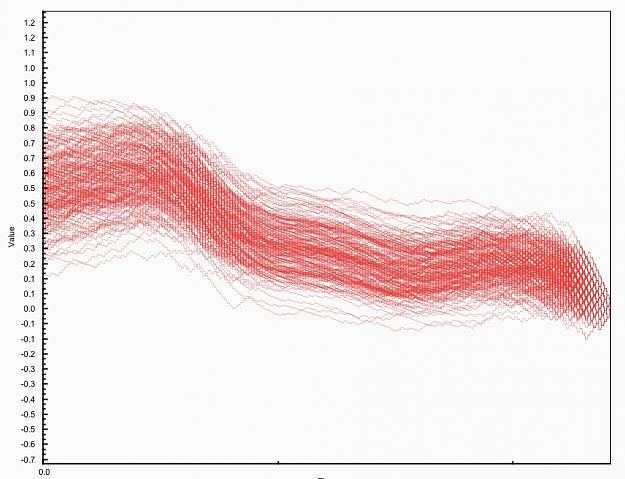

(Backtest Data Assuming Leverage)

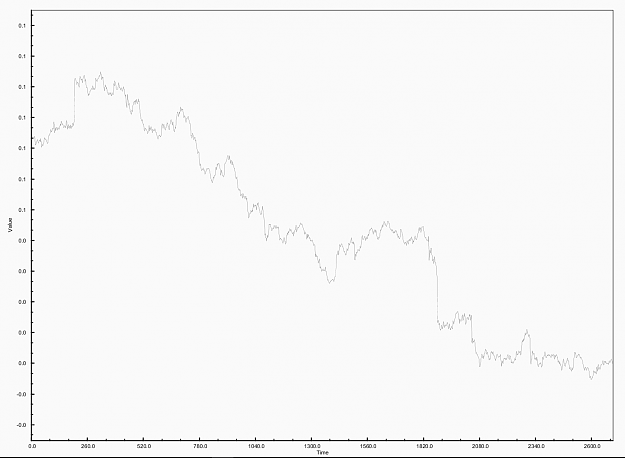

Strategy A Statistics:

CAGR: 52%

Sharpe: 2.85

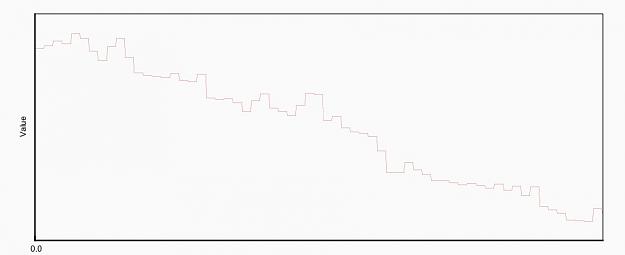

Strategy B Statistics:

CAGR: 60%

Sharpe: 3.01

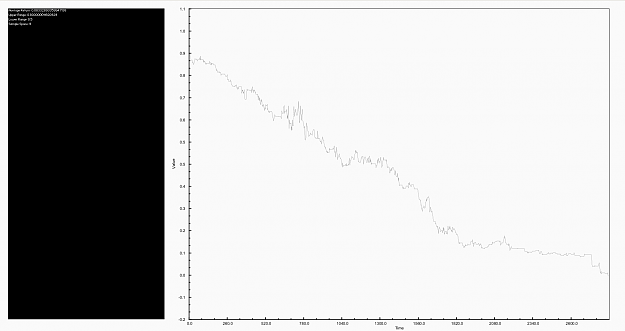

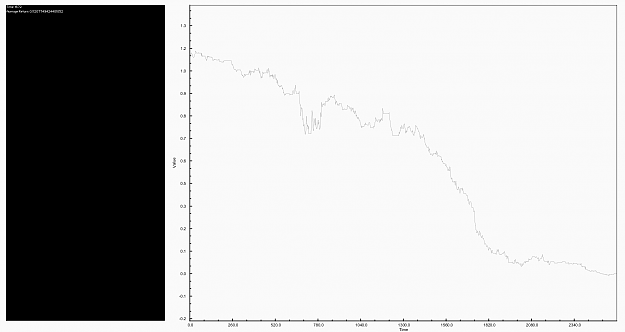

Strategy A Graph:

Strategy B Graph:

Methodology:

I must first say a little about myself and my approach to trading FX, first things first, I am a an experienced programmer (I began at age 11 and am now 16),

I write my code primarily in Java, and have developed a backtesting infrastructure with data from Quandl as well as a parser to read my brokerage's historical

FX data. I follow the assumption (based on evidence) that a single asset's past prices alone cannot predict that of the future, however when external information is applied (econometrics, other asset prices and correlation, order flow/volume, as well as implied volatility) all can be used to forecast future performance. An example of a system I may develop (for explanation purposes) would be short the dollar if Non Farm is below 150k, other wise hold. Compared this to others who may use

technical indicators which I have no data suggesting they are capable of predicting the market.

Current situation:

At the moment I have two strategies trading, these are swing trading systems making trading decisions based on fundamentals, each having four hours of exposure unless I intervene due to reasons such as FOMC press conferences/speeches or other news events that causes the trade to potentially reverse. The systems do not have stops/takes because I have found that greater returns are possible without them and as well due to how I mathematically model the effect of these events on volatility. My current goals are to build a portfolio of 5 market neutral strategies all with a low correlation to one another's returns, 3-4 short term, as well as 1-2 long term. I also plan to target a sharpe ratio of 2.5 or higher. Sharpe ratio for those who don't know is mean returns divided by the standard deviation of returns. A rule I have set for my short term strategies is a max leverage of 1:10, and 1:4 for long term. My strategies are currently very low latency, with only two opportunities a week and each trading an average of 40% of weeks (this means I will make a trade 64% of weeks). Finally I expect to make at least 5% return a month and will be compounding monthly hoping for 110%-200% return a year..

Another thing to note about backtests is that there is only 3 months of 30 minute bar data on my hard drive, If anyone can get me more data that is from Oanda that would be phenomenal!!

(Backtest Data Assuming Leverage)

Strategy A Statistics:

CAGR: 52%

Sharpe: 2.85

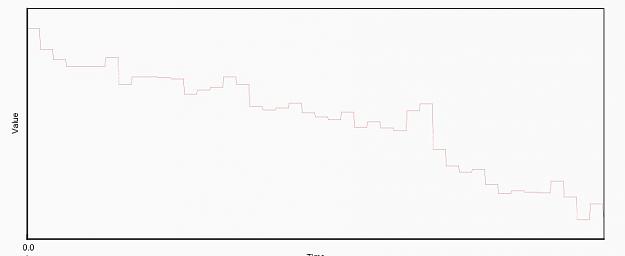

Strategy B Statistics:

CAGR: 60%

Sharpe: 3.01

Strategy A Graph:

Attached Image (click to enlarge)

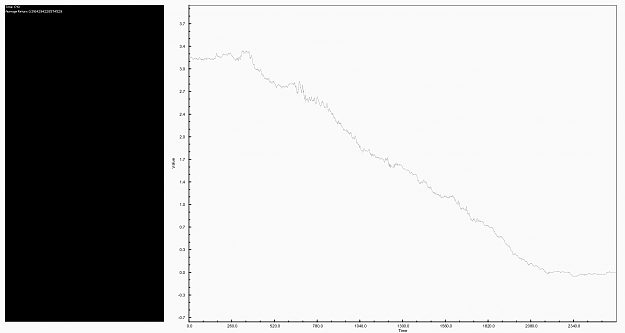

Strategy B Graph:

Attached Image (click to enlarge)

Quant Trader - My Blog: quantstop.blogspot (dot) com