I received an email that explains the strategy described below. Anyone have any experience trading something equal to or like this?

The program is designed to capitalize on the quantified market price behavior and unique correlation interplay that exists between three major currency pairs; the EUR/USD (Euro vs. US dollar), the USD/JPY (US Dollar vs. Japanese-yen), and the EUR/JPY (Euro vs. Japanese-yen).

The objective is to 'arb' the inefficiencies that frequently occur in this triangular combination, when one major pair is mispriced relative to its minor cross counter-parts or vice versa.

This is what a trade example might look like:

Let’s say the EUR/JPY (Euro vs. Japanese-yen) is normally equal to a value of 1. Alternatively, if one bought the EUR/USD (Euro vs. US dollar), and simultaneously bought the USD/JPY (US dollar vs. Japanese-yen), the combination of these two related pairs should also equal a value of 1. The inherent profit opportunity is presented when either "side" is not equal to 1. To capitalize on a perceived "imbalance" in the interrelationship of these pairs, a combination trade is entered to create a "synthetic" arbitrage. For example, this strategy would, SHORT 1.2 lots EUR/USD and simultaneously BUY 0.78 EUR/JPY and BUY 0.42 USD/JPY. Ideally one side will come back to sync and equal a value of 1.

The system was designed to capture the substantial efficiencies and capabilities of this institutional money management and trading methodology.

The program can be characterized as a counter-trending system, in that it primarily sells into strength and buys into weakness. To reduce the obvious event risk of any one of these currency pairs trending heavily in a single direction without a retracement, the system utilizes a triangular combination comprised of the three designated currency pairs to “hedge out” of losing trades, thus reducing risk levels to an acceptable level, while allowing for substantial returns.

This automated trading system does not rely on precise or perfect timing in the entry execution of a trade. Once a (buy or sell) trade (in one of the three pairs) has been initiated, should the market in that particular pair start to move against it, the system algorithms will initiate another trade in one of the two other pair choices to offset or mitigate the risk and/or create an incremental profit opportunity for the composite position “basket”.

In the process of executing its objectives, the system accumulates multiple positions - comprising a “basket” - very rapidly and over a short time span. As market elasticity and/or volatility expands, the system will continue to aggregate more (and perhaps larger) position sizes, until such point, when the entire accumulated basket position is liquidated at a pre-determined profit target – and then the process begins all over again. (The program always maintains a stop-loss in the event the pre-determined profit level(s) is not reached).

When the basket is liquidated some positions will be closed out with a debit and the other(s) with a credit. It is the objective of the system to close out each basket with an overall credit on the underlying basket.

The secret to the success of the program is the proprietary Money Management Module (MMM), which calculates and calibrates optimal trade (lot) position sizing relative to overall account balance. Our automated Money Management functions can adjust trade size settings according to the risk profile of each client. Trades can be specified in terms of Maximum Number of Orders, Slippage, Stop-Loss, Take Profit, Risk Level, etc. A percentage of the account value is risked per trade in order to generate a prescribed percent of profit (for example 1% of the account value is risked in order to achieve a 2.2% return on the account).

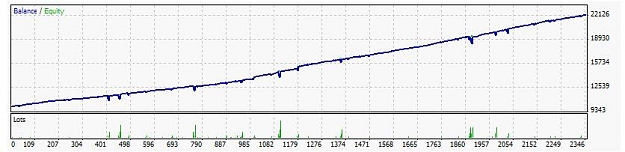

The program was structured and designed to yield a smooth and consistent rising equity curve. Investors should anticipate low-to-medium volatility with consistent monthly profits of between 3-5%.

The program is designed to capitalize on the quantified market price behavior and unique correlation interplay that exists between three major currency pairs; the EUR/USD (Euro vs. US dollar), the USD/JPY (US Dollar vs. Japanese-yen), and the EUR/JPY (Euro vs. Japanese-yen).

The objective is to 'arb' the inefficiencies that frequently occur in this triangular combination, when one major pair is mispriced relative to its minor cross counter-parts or vice versa.

This is what a trade example might look like:

Let’s say the EUR/JPY (Euro vs. Japanese-yen) is normally equal to a value of 1. Alternatively, if one bought the EUR/USD (Euro vs. US dollar), and simultaneously bought the USD/JPY (US dollar vs. Japanese-yen), the combination of these two related pairs should also equal a value of 1. The inherent profit opportunity is presented when either "side" is not equal to 1. To capitalize on a perceived "imbalance" in the interrelationship of these pairs, a combination trade is entered to create a "synthetic" arbitrage. For example, this strategy would, SHORT 1.2 lots EUR/USD and simultaneously BUY 0.78 EUR/JPY and BUY 0.42 USD/JPY. Ideally one side will come back to sync and equal a value of 1.

The system was designed to capture the substantial efficiencies and capabilities of this institutional money management and trading methodology.

The program can be characterized as a counter-trending system, in that it primarily sells into strength and buys into weakness. To reduce the obvious event risk of any one of these currency pairs trending heavily in a single direction without a retracement, the system utilizes a triangular combination comprised of the three designated currency pairs to “hedge out” of losing trades, thus reducing risk levels to an acceptable level, while allowing for substantial returns.

This automated trading system does not rely on precise or perfect timing in the entry execution of a trade. Once a (buy or sell) trade (in one of the three pairs) has been initiated, should the market in that particular pair start to move against it, the system algorithms will initiate another trade in one of the two other pair choices to offset or mitigate the risk and/or create an incremental profit opportunity for the composite position “basket”.

In the process of executing its objectives, the system accumulates multiple positions - comprising a “basket” - very rapidly and over a short time span. As market elasticity and/or volatility expands, the system will continue to aggregate more (and perhaps larger) position sizes, until such point, when the entire accumulated basket position is liquidated at a pre-determined profit target – and then the process begins all over again. (The program always maintains a stop-loss in the event the pre-determined profit level(s) is not reached).

When the basket is liquidated some positions will be closed out with a debit and the other(s) with a credit. It is the objective of the system to close out each basket with an overall credit on the underlying basket.

The secret to the success of the program is the proprietary Money Management Module (MMM), which calculates and calibrates optimal trade (lot) position sizing relative to overall account balance. Our automated Money Management functions can adjust trade size settings according to the risk profile of each client. Trades can be specified in terms of Maximum Number of Orders, Slippage, Stop-Loss, Take Profit, Risk Level, etc. A percentage of the account value is risked per trade in order to generate a prescribed percent of profit (for example 1% of the account value is risked in order to achieve a 2.2% return on the account).

The program was structured and designed to yield a smooth and consistent rising equity curve. Investors should anticipate low-to-medium volatility with consistent monthly profits of between 3-5%.

Attached Image (click to enlarge)