Mad world

Hello dear subscribers,

The stock market world, as we know it, has not existed for a long time. When we think of Wall Street, we see brokers shout at each other and acting with each other. Stock exchange trading today takes place beyond the major stock exchanges, usually in large data centers of banks and institutions. While in the past traders were decisive factors in trade, they were long since replaced by physicists, mathematicians and programmers. At the heart of today's trading decisions are the algorithms that control highly complex trading bots. Over 10 years ago, the first high-frequency traders who penetrated the stock exchange markets in order to make life more difficult for banks, asset managers, life insurers, pension funds and investment funds became established. The three most common strategies used by high-frequency traders are the provision of liquidity, arbitrage, and the detection of liquidity. When providing liquidity, high-frequency traders behave like traditional market makers: they offer buying and selling prices, but without the commitment of traditional market makers to always be present on the market. In doing so, these dealers access a strategically sophisticated software environment.

Interesting high-frequency trading algorithm that has taken place in the S & P 500 futures contract. In 7 seconds, there were over 7,000 trades (52,000 contracts). The video shows in 7 minutes what happened in the 7 seconds.

In 1,238 trading days, the largest high-frequency trader made a loss on only one day, at the same time Goldman Sachs came to 124 loss days. Goldman Sachs tops the charts with a 90% win rate, but the largest high-frequency trader Virtu is still significantly better. Scientists working on Virtu's trading activity found Virtu not taking much risk in trading. High frequency trading is a worthwhile business. The big players have long recognized this and made a counter-stroke. They work with the same tricks to compete in the market. As a result, three major banks were also fined millions of dollars for spoofing. Therefore, the market has become even more confusing and harder. And in the future it will be much harder to earn money in these markets.

Although there are many more private traders trading on the stock exchanges than big players, the turnover of big players is well above retailers at 90%. For the stock exchanges, the big players are therefore clearly more important, what that means, is clear for everyone. There are significant differences in data feeds and fees, as well as the speed of order execution. The big players are able to trade millions of shares within 2 minutes without overly large orders. This is made possible by the special algorithms that take over the trade.

While the traders continue to upgrade, the stock exchange supervision hardly comes after. Traders generate up to 1,000,000 data records per minute via Eurex alone. If you want to track down grievances, you can immediately get a container ship with printouts of trade data. Complete monitoring of market manipulation is therefore no longer possible. That an authority can do something with the complicated algorithms, is also difficult to imagine. This facilitates future market manipulation. Techniques were banned by the stock exchange, where an algorithm stops orders in the trading system that should not be executed at all. However, it is hard to imagine that Deutsche Börse voluntarily puts rules in its statutes that annoy high-frequency traders. Its ten largest customers generate 50% of sales and provide additional liquidity in many markets.

As retail traders, we do not have complicated algorithms, fast data cables, high-performance computers or the capital needed to move markets. That's why we need to look more closely at the big player approach. Between the high-frequency traders and big players, I would not like to differentiate at this point, since the big players have already begun to work with the tricks of high-frequency traders. It is crucial to know the way of working in order to draw insights that protect us from possible losses.

Spoofing

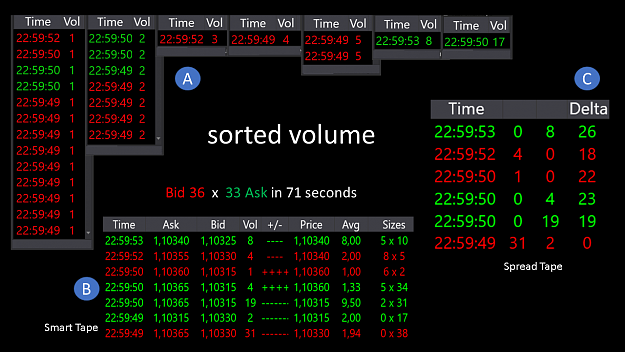

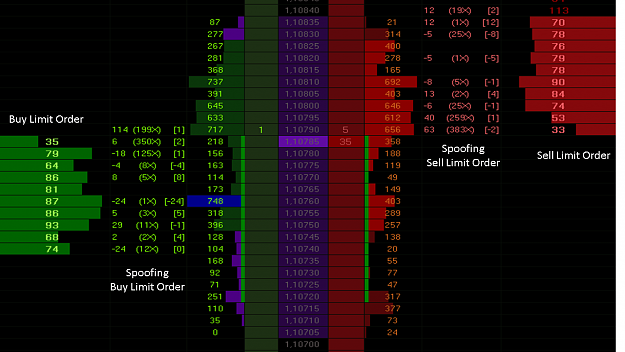

The practices often used in the past are called smoking or spoofing, which enables large market participants to gain trading advantages at the expense of slower acting business partners. This is because very short-term participants analyze the purchase and sale orders very precisely because they hope to obtain information about imminent price changes. For the big market participants, this offers the opportunity to simulate large orders, which in reality do not exist by the rapid adjustment. The other traders can not analyze these orders in the short term and are confused. Since they do not know which orders are correct and which are only fictitious orders, this gives the large market participants a time advantage, since they know their right orders. The big orders are then withdrawn at lightning speed as soon as the big player has executed its set counterorder in the market. Many high-frequency traders place their computers not so close to the exchange's main computer to trade faster, but to be able to cancel orders at lightning speed.

Many market participants are guided by the set limit orders in the Oderbuch, which represent the relationship between demand and supply. Some years ago, on the New York and German Stock Exchange more than 90% of orders were not executed. Therefore, I strongly recommend to pay less attention to these limit orders. While a good prop software can detect the deleted and added limit orders, in very volatile phases this is often useless. However, deleted limit orders help identify a new demand or offer. Certain algorithms use these phantom orders to try to get the opponent's algorithm to buy. It analyzes when the opposing algorithm begins to abandon its buy order. After that, exactly that number of limit orders that trigger the opposing algorithm are given up. For this reason, it will still continue to come to the known spoofing.

News Reader

It is a software that is able to read current business news into the marketplace by launching a specific algorithm that immediately places buy or sell orders in the market before the actual prices can react.

Arbitrage

Here, price differences are exploited on different stock exchanges. Thereby, papers are bought on one stock exchange and immediately resold on another stock exchange. The price differences are small, but the larger the number of pieces, the sooner the deal is worthwhile.

Pinging

An algorithm is programmed to send small orders to different exchanges to find out where liquidity exists and at the same time to look at the trading books.

Snipping

With small, quickly issued orders, the market is searched for hidden orders. The goal of finding large buy and sell limits of other traders. Just before these thresholds, which promise the release of large orders, then the own orders are placed. The limit orders of the other participants will be triggered much later and drive the course in the desired direction of the big player.

Scalping

The faster the respective system, the higher the decisive advantage. As soon as the systems detect large order volumes, they are on the market at lightning speed. So you can buy even cheaper than the other dealers. Even before you can govern, the dealers are already outside again and the course turns immediately in the other direction. The slower traders are virtually eaten by the market.

Quote Stuffing

This is a fight between HFT algorithms. Some of these companies have chosen to fool their fellow competitors by placing thousands of orders within a second and immediately deleting them. This can be up to 15,000 orders within a few seconds. The point is that other algorithms have to handle this flood of data and are thereby deceived. The algorithm that sends these data knows that they are wrong and need not be analyzed. This saves time and they can wait for opportunities in the market that the other algorithms fail to recognize due to their "preoccupation" with the fake orders.

Wash trades

I have already described this approach in previous posts and is particularly controversial. The trader deals with himself here. He hunts his buy order up to his sell limit order, which then pushes the price down immediately. Or, in a rising market, a turnaround is suggested in order to buy cheaper again before the market turns sharply upwards again. The goal is to push merchants out of the market or to induce them to make transactions that they probably would not have done in other circumstances.

Front Running

This procedure is particularly nasty. A player is to buy a specific currency pair at a specific price for his customer. The player buy for himself, before acting for his client. Since this procedure is forbidden, the trading is done by another company. This makes it harder to prove an offense.

Big buy, small sell

This is a procedure I have been able to observe myself in the last few months, that's why I called it that. On a high, suddenly a huge purchase order is placed in the market. This purchase order is not a bogus order but an order actually placed in the order book. Traders see this single order and start buying. After all, a big player does not invest such a large order for nothing. The big player is starting to sell up his big order in small pieces. As a result, the price does not go up. Then the big player pushes the course down. As many buyers enter the market there is enough liquidity available. Once the Trader's first stops are triggered, there is a chain reaction down. Already there the big player gets out again. On his big order, the big player loses maybe a few dollars, which he get back but immediately.

Fake resistance zones

Since many traders believe in resistance zones, the big players produce artificial resistance zones by bouncing off the course at certain price zones. These resistance zones are exploited to get high liquidity at this price level, which is detrimental to most retail traders. Since many traders work with the Fibonacci, this type of trading is also incorporated into your strategy. At the 50 retracement, the price is pushed up, which attracts many buyers in the market, the short time later all are stopped. It does not matter if you work with an MA, Fibonacci or Candle Patterns, what we see is really different. How else can you explain that over 90% of traders are wrong?

The tricks of the big players create a false truth about supply and demand. The only truth is the resulting candle, but the moment we see the candle, that's already the past. Individual papers can lose 20 or even 40% of their value within seconds without fundamental justification, only to recover a short time later. Once the algo trade has spied a strategy, it is outdated. This approach makes the entire fundamental analysis almost superfluous.

Here you can see a Nanex animation of the S & P 500 futures during the Flash crash on May 6, 2010.

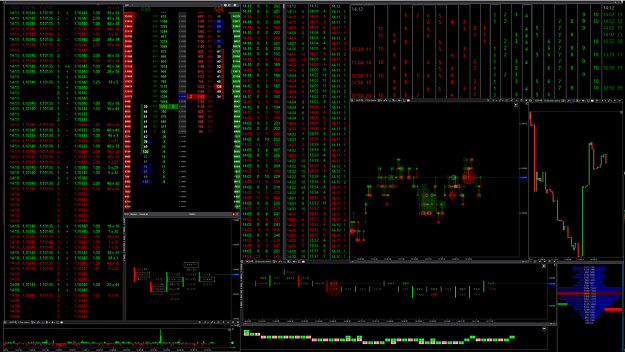

Market depth is a possible step to analyze demand and supply, but usually uses limit orders, which often give a false picture of demand and supply. Much more important seem to be the orders actually placed.

An important insight is that predicting a future course from the current track is wrong in most cases. The recommendation that we pay less attention to the current chart image and focus more on the Equilibrium. So on the small breaks in which the price is balanced.

First, we should deal with the reality that awaits us in the market.

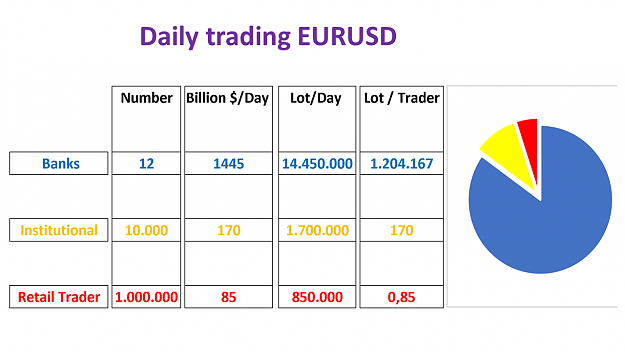

There are 12 big players in the forex market that account for 85% of the total market. Essentially, these banks control the price performance of the EURUSD. However, the willingness of individual retail traders to invest is also highly dependent on this. As we know, the big players in an equilibrium or sideways market must raise ask or bid to then push the price in their desired direction. It is crucial in which amount the retail traders are willing to invest ask or bid. As a rule, the retail traders are encouraged by the big players to make certain investments at certain price levels. The big players are able to project typical resistance and support zones to deceive retail traders. But this approach does not always work as the big players imagine. Therefore, they are trying all tricks, to lure the dump money on a wrong track. Spoofing, fake resistance zones, Big buy, small sell and stophunting are just a few of the endless possibilities to get the money from retail traders. When a big player has collected a large amount of Ask, news, politics and currency strength are no longer important. Even if news or politics point to dollar strength, the big player will push the euro higher to realize its gains. Therefore, news or political circumstances are often not relevant. The decisive factor is what happens in the market right now. Will the dollar or the euro is bought, will the euro or the dollar is sold. This situation needs to be analyzed daily and can change at any time. Of course, the central banks play a decisive role.

The big players rarely buy the euro at the low and usually never sell it at high. Likewise, they rarely buy the dollar high and never sell it low. The background is that the big players are implementing a high amount of lot. A big player buys the euro and pushes up the price. More traders enter the market and ensure a further increase in prices. To get out of the euro, the player now has to bring a high number of bid into the market. But there must be traders who continue to believe in the euro and invest in the market so that the big player can sell his euro. To get a good price, the big player has to get out of the euro before the high. This way of working distinguishes the big players from the retail traders. The most successful big players are day traders who realize their main profits within a day. Even more successful are some high frequency traders.

So it's always about gathering in the sideways markets Bid or Ask to realize profits. This situation can change any time a big player leaves his position. For this reason, a long-term forecast of a price development is not possible. The key is to recognize whether Bid or Ask is being collected. Unfortunately, no indicator in the forex market is able to recognize this, as no bid and ask are published in the forex market.

A short-term forecast is also not possible because the big players first collect a certain number of bid or ask in order to move the price in the medium term. If you are able to find out what the big players are collecting, it is possible to anticipate the medium term movement. Unfortunately, the exact time of an outbreak is difficult to see ahead.

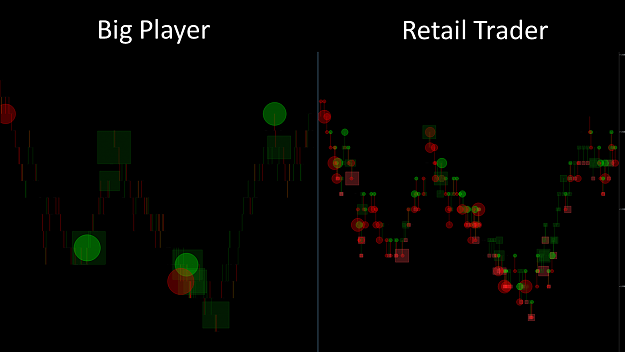

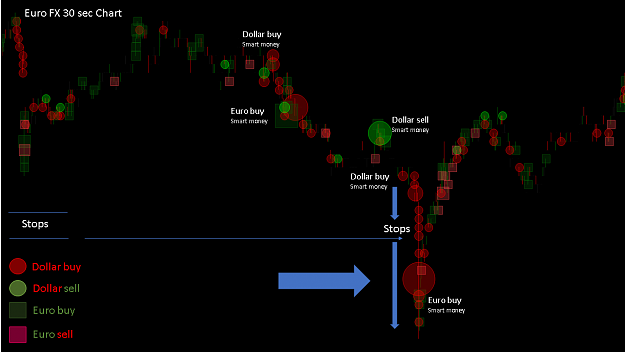

In the following video, I have set up a cluster search in which, using bid and ask, the market divides as follows: buy euro = green square, sell euro = red square, buy dollar = red circle and sell dollar = green circle. The filtering takes into account both a certain number of trades, an imbalance, an identification of the big players, and the delta between ask and bid. The setting is still incorrect, but should clarify the future goal.

You can already see the individual relationships between bid and ask and the resulting results. The filtering has to be optimized and adapted to individual market situations. From this one can not fundamentally derive a future movement, as the big players often work with a time delay. You must first collect before pushing the course in a particular direction. This approach is interesting in the sideways markets or within an equilibrium. There you can implement the information faster.

Let's summarize the information briefly again

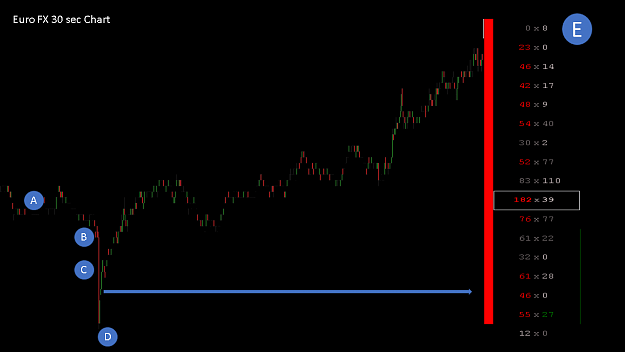

Point A

First, we realize that there is a stronger dollar sale, then the euro is bought on a larger scale, the price goes up.

Point B

Already here, a stronger euro sale takes place, which indicates that the price could not rise so much.

Point C

Already here, the first larger dollar purchases take place, the price goes down for a brief moment and is pushed up again.

Point D

Here comes a big dollar buyer in the market and pushes the price down a bit more.

Point E

In the smaller equilibrium you can see that the euro is bought very heavily at the end and the price goes up.

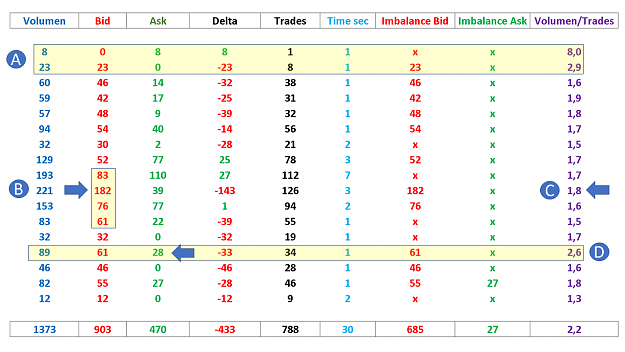

Point F

The euro sellers hold back first, when the course runs down the dollar is bought heavily.

Point G

Here, the euro is bought stronger and pushes the course again stronger. A short time later, a strong dollar buyer came into the market, pushing the price down.

If we look at an M1 in EURUSD at the same time, it quickly becomes clear that we can not read this information based on a candle. That is also clear, because the important information of Bid and Ask is missing.

Conclusion

Whether the price rises or falls more or less in the short and long term is unpredictable. Predictable is that the course moves in waves up and down. Trading is always in the direction that promises the most profit for the big players, and that may be identifying in a medium term area. The crucial zones are the sideways markets or an equilibrium. There is often collected in the second half, a larger number of bid or ask, which can anticipate a possible future price course.

With the optimal filtering of individual clusters, it is easiest to be able to recognize what is happening in the market right now. The way the big players work is not like a racing boat but rather a container ship. Sometimes collecting bid or ask can take days before a sharp price move up or down. And a big player does not always have to be active in the market. Often the smaller players are allowed to operate in the market and big players only intervene in certain regions to build certain fake resistance zones, which are then exploited at the crucial moment.

The real stock market data have clear advantages over the Forex data, this is undisputed. But the trick is to filter that stock market data. The information obtained from this must show a trader whether a bullish move is caused by a euro buy or dollar sale. That's a big difference. If the bullish movement comes about through a dollar sale, it is likely that an equilibrium will be created first, and the euro will have to be rebuilt before the price moves higher. If the bullish movement is created by buying more euros, there is a greater likelihood that the market will continue to move higher. In addition, you should also pay attention to Euro sales and dollar purchases.

With the correct filter setting, triggered stops can also be displayed. This is just before major outbreaks a crucial indicator of the future price performance. The challenge is the exact filtering of individual data. And that is the crucial point, which will take a lot of time. In my opinion a decisive strategy to survive in this tough market in the long term.

I wish you a successful trading week

best regards

Hello dear subscribers,

The stock market world, as we know it, has not existed for a long time. When we think of Wall Street, we see brokers shout at each other and acting with each other. Stock exchange trading today takes place beyond the major stock exchanges, usually in large data centers of banks and institutions. While in the past traders were decisive factors in trade, they were long since replaced by physicists, mathematicians and programmers. At the heart of today's trading decisions are the algorithms that control highly complex trading bots. Over 10 years ago, the first high-frequency traders who penetrated the stock exchange markets in order to make life more difficult for banks, asset managers, life insurers, pension funds and investment funds became established. The three most common strategies used by high-frequency traders are the provision of liquidity, arbitrage, and the detection of liquidity. When providing liquidity, high-frequency traders behave like traditional market makers: they offer buying and selling prices, but without the commitment of traditional market makers to always be present on the market. In doing so, these dealers access a strategically sophisticated software environment.

Inserted Video

Interesting high-frequency trading algorithm that has taken place in the S & P 500 futures contract. In 7 seconds, there were over 7,000 trades (52,000 contracts). The video shows in 7 minutes what happened in the 7 seconds.

In 1,238 trading days, the largest high-frequency trader made a loss on only one day, at the same time Goldman Sachs came to 124 loss days. Goldman Sachs tops the charts with a 90% win rate, but the largest high-frequency trader Virtu is still significantly better. Scientists working on Virtu's trading activity found Virtu not taking much risk in trading. High frequency trading is a worthwhile business. The big players have long recognized this and made a counter-stroke. They work with the same tricks to compete in the market. As a result, three major banks were also fined millions of dollars for spoofing. Therefore, the market has become even more confusing and harder. And in the future it will be much harder to earn money in these markets.

Although there are many more private traders trading on the stock exchanges than big players, the turnover of big players is well above retailers at 90%. For the stock exchanges, the big players are therefore clearly more important, what that means, is clear for everyone. There are significant differences in data feeds and fees, as well as the speed of order execution. The big players are able to trade millions of shares within 2 minutes without overly large orders. This is made possible by the special algorithms that take over the trade.

While the traders continue to upgrade, the stock exchange supervision hardly comes after. Traders generate up to 1,000,000 data records per minute via Eurex alone. If you want to track down grievances, you can immediately get a container ship with printouts of trade data. Complete monitoring of market manipulation is therefore no longer possible. That an authority can do something with the complicated algorithms, is also difficult to imagine. This facilitates future market manipulation. Techniques were banned by the stock exchange, where an algorithm stops orders in the trading system that should not be executed at all. However, it is hard to imagine that Deutsche Börse voluntarily puts rules in its statutes that annoy high-frequency traders. Its ten largest customers generate 50% of sales and provide additional liquidity in many markets.

As retail traders, we do not have complicated algorithms, fast data cables, high-performance computers or the capital needed to move markets. That's why we need to look more closely at the big player approach. Between the high-frequency traders and big players, I would not like to differentiate at this point, since the big players have already begun to work with the tricks of high-frequency traders. It is crucial to know the way of working in order to draw insights that protect us from possible losses.

Spoofing

The practices often used in the past are called smoking or spoofing, which enables large market participants to gain trading advantages at the expense of slower acting business partners. This is because very short-term participants analyze the purchase and sale orders very precisely because they hope to obtain information about imminent price changes. For the big market participants, this offers the opportunity to simulate large orders, which in reality do not exist by the rapid adjustment. The other traders can not analyze these orders in the short term and are confused. Since they do not know which orders are correct and which are only fictitious orders, this gives the large market participants a time advantage, since they know their right orders. The big orders are then withdrawn at lightning speed as soon as the big player has executed its set counterorder in the market. Many high-frequency traders place their computers not so close to the exchange's main computer to trade faster, but to be able to cancel orders at lightning speed.

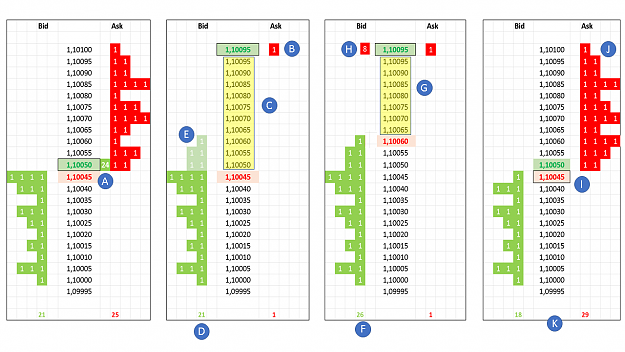

Attached Image (click to enlarge)

Many market participants are guided by the set limit orders in the Oderbuch, which represent the relationship between demand and supply. Some years ago, on the New York and German Stock Exchange more than 90% of orders were not executed. Therefore, I strongly recommend to pay less attention to these limit orders. While a good prop software can detect the deleted and added limit orders, in very volatile phases this is often useless. However, deleted limit orders help identify a new demand or offer. Certain algorithms use these phantom orders to try to get the opponent's algorithm to buy. It analyzes when the opposing algorithm begins to abandon its buy order. After that, exactly that number of limit orders that trigger the opposing algorithm are given up. For this reason, it will still continue to come to the known spoofing.

News Reader

It is a software that is able to read current business news into the marketplace by launching a specific algorithm that immediately places buy or sell orders in the market before the actual prices can react.

Arbitrage

Here, price differences are exploited on different stock exchanges. Thereby, papers are bought on one stock exchange and immediately resold on another stock exchange. The price differences are small, but the larger the number of pieces, the sooner the deal is worthwhile.

Pinging

An algorithm is programmed to send small orders to different exchanges to find out where liquidity exists and at the same time to look at the trading books.

Snipping

With small, quickly issued orders, the market is searched for hidden orders. The goal of finding large buy and sell limits of other traders. Just before these thresholds, which promise the release of large orders, then the own orders are placed. The limit orders of the other participants will be triggered much later and drive the course in the desired direction of the big player.

Scalping

The faster the respective system, the higher the decisive advantage. As soon as the systems detect large order volumes, they are on the market at lightning speed. So you can buy even cheaper than the other dealers. Even before you can govern, the dealers are already outside again and the course turns immediately in the other direction. The slower traders are virtually eaten by the market.

Quote Stuffing

This is a fight between HFT algorithms. Some of these companies have chosen to fool their fellow competitors by placing thousands of orders within a second and immediately deleting them. This can be up to 15,000 orders within a few seconds. The point is that other algorithms have to handle this flood of data and are thereby deceived. The algorithm that sends these data knows that they are wrong and need not be analyzed. This saves time and they can wait for opportunities in the market that the other algorithms fail to recognize due to their "preoccupation" with the fake orders.

Wash trades

I have already described this approach in previous posts and is particularly controversial. The trader deals with himself here. He hunts his buy order up to his sell limit order, which then pushes the price down immediately. Or, in a rising market, a turnaround is suggested in order to buy cheaper again before the market turns sharply upwards again. The goal is to push merchants out of the market or to induce them to make transactions that they probably would not have done in other circumstances.

Front Running

This procedure is particularly nasty. A player is to buy a specific currency pair at a specific price for his customer. The player buy for himself, before acting for his client. Since this procedure is forbidden, the trading is done by another company. This makes it harder to prove an offense.

Big buy, small sell

This is a procedure I have been able to observe myself in the last few months, that's why I called it that. On a high, suddenly a huge purchase order is placed in the market. This purchase order is not a bogus order but an order actually placed in the order book. Traders see this single order and start buying. After all, a big player does not invest such a large order for nothing. The big player is starting to sell up his big order in small pieces. As a result, the price does not go up. Then the big player pushes the course down. As many buyers enter the market there is enough liquidity available. Once the Trader's first stops are triggered, there is a chain reaction down. Already there the big player gets out again. On his big order, the big player loses maybe a few dollars, which he get back but immediately.

Fake resistance zones

Since many traders believe in resistance zones, the big players produce artificial resistance zones by bouncing off the course at certain price zones. These resistance zones are exploited to get high liquidity at this price level, which is detrimental to most retail traders. Since many traders work with the Fibonacci, this type of trading is also incorporated into your strategy. At the 50 retracement, the price is pushed up, which attracts many buyers in the market, the short time later all are stopped. It does not matter if you work with an MA, Fibonacci or Candle Patterns, what we see is really different. How else can you explain that over 90% of traders are wrong?

The tricks of the big players create a false truth about supply and demand. The only truth is the resulting candle, but the moment we see the candle, that's already the past. Individual papers can lose 20 or even 40% of their value within seconds without fundamental justification, only to recover a short time later. Once the algo trade has spied a strategy, it is outdated. This approach makes the entire fundamental analysis almost superfluous.

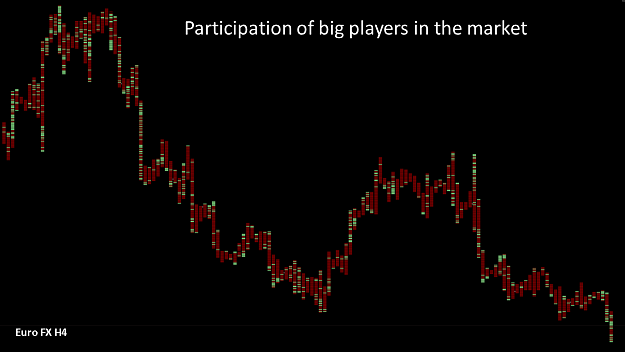

Here you can see a Nanex animation of the S & P 500 futures during the Flash crash on May 6, 2010.

Inserted Video

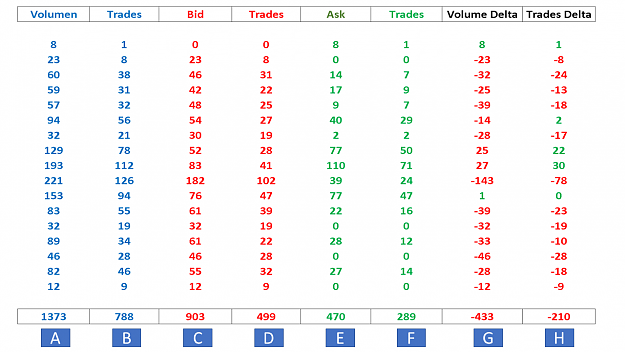

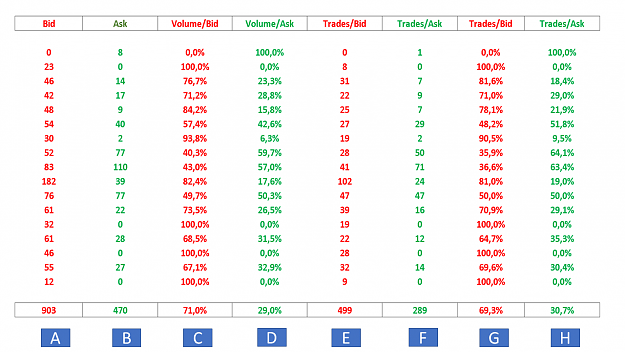

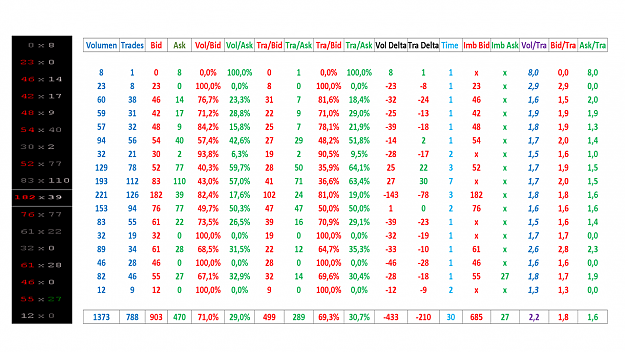

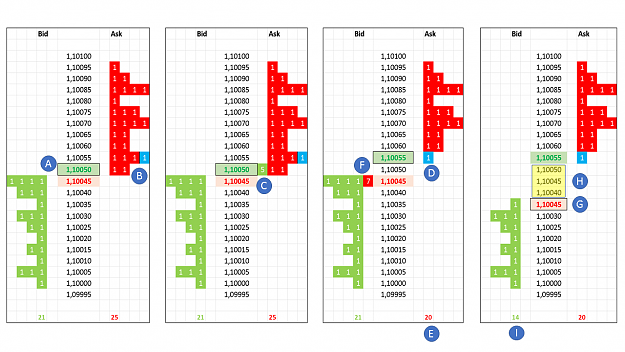

Market depth is a possible step to analyze demand and supply, but usually uses limit orders, which often give a false picture of demand and supply. Much more important seem to be the orders actually placed.

Attached Image (click to enlarge)

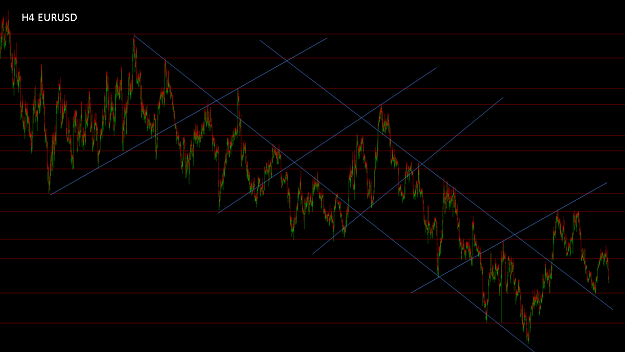

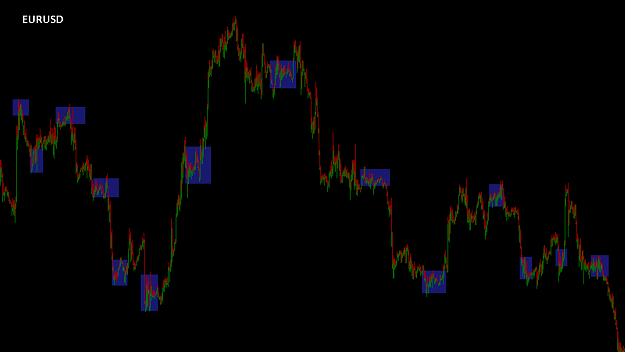

An important insight is that predicting a future course from the current track is wrong in most cases. The recommendation that we pay less attention to the current chart image and focus more on the Equilibrium. So on the small breaks in which the price is balanced.

First, we should deal with the reality that awaits us in the market.

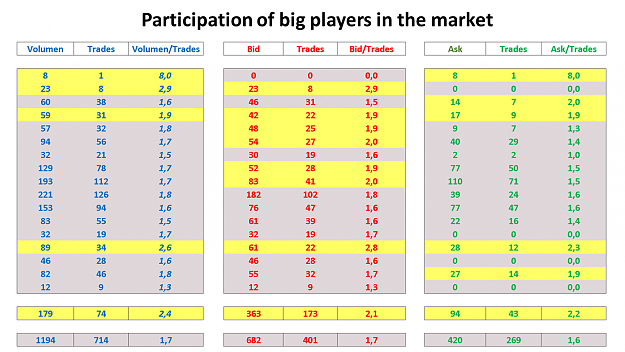

There are 12 big players in the forex market that account for 85% of the total market. Essentially, these banks control the price performance of the EURUSD. However, the willingness of individual retail traders to invest is also highly dependent on this. As we know, the big players in an equilibrium or sideways market must raise ask or bid to then push the price in their desired direction. It is crucial in which amount the retail traders are willing to invest ask or bid. As a rule, the retail traders are encouraged by the big players to make certain investments at certain price levels. The big players are able to project typical resistance and support zones to deceive retail traders. But this approach does not always work as the big players imagine. Therefore, they are trying all tricks, to lure the dump money on a wrong track. Spoofing, fake resistance zones, Big buy, small sell and stophunting are just a few of the endless possibilities to get the money from retail traders. When a big player has collected a large amount of Ask, news, politics and currency strength are no longer important. Even if news or politics point to dollar strength, the big player will push the euro higher to realize its gains. Therefore, news or political circumstances are often not relevant. The decisive factor is what happens in the market right now. Will the dollar or the euro is bought, will the euro or the dollar is sold. This situation needs to be analyzed daily and can change at any time. Of course, the central banks play a decisive role.

The big players rarely buy the euro at the low and usually never sell it at high. Likewise, they rarely buy the dollar high and never sell it low. The background is that the big players are implementing a high amount of lot. A big player buys the euro and pushes up the price. More traders enter the market and ensure a further increase in prices. To get out of the euro, the player now has to bring a high number of bid into the market. But there must be traders who continue to believe in the euro and invest in the market so that the big player can sell his euro. To get a good price, the big player has to get out of the euro before the high. This way of working distinguishes the big players from the retail traders. The most successful big players are day traders who realize their main profits within a day. Even more successful are some high frequency traders.

So it's always about gathering in the sideways markets Bid or Ask to realize profits. This situation can change any time a big player leaves his position. For this reason, a long-term forecast of a price development is not possible. The key is to recognize whether Bid or Ask is being collected. Unfortunately, no indicator in the forex market is able to recognize this, as no bid and ask are published in the forex market.

A short-term forecast is also not possible because the big players first collect a certain number of bid or ask in order to move the price in the medium term. If you are able to find out what the big players are collecting, it is possible to anticipate the medium term movement. Unfortunately, the exact time of an outbreak is difficult to see ahead.

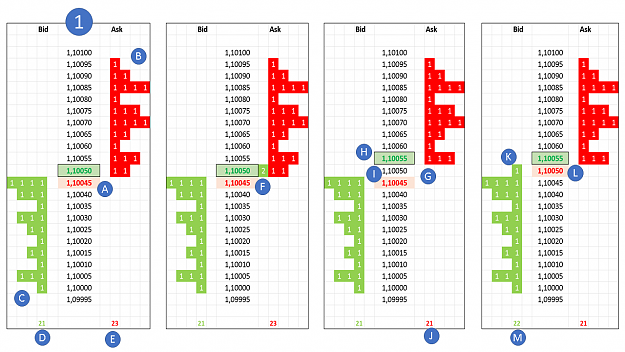

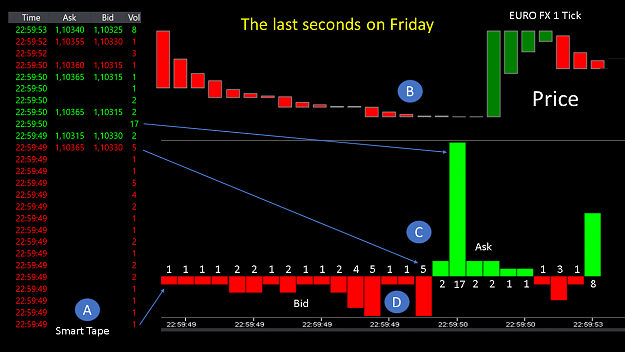

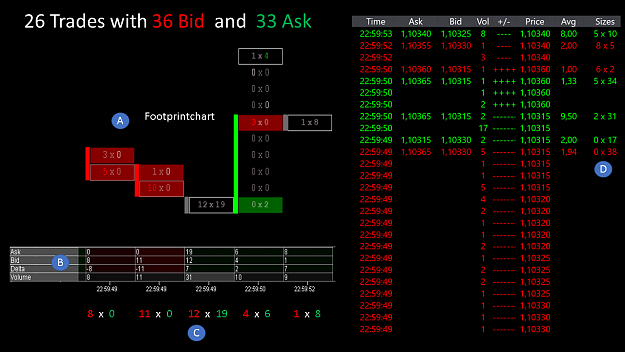

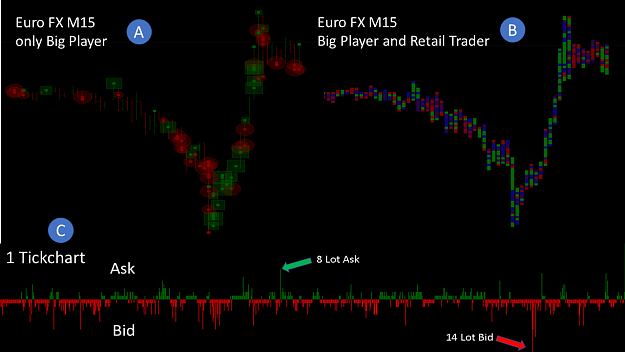

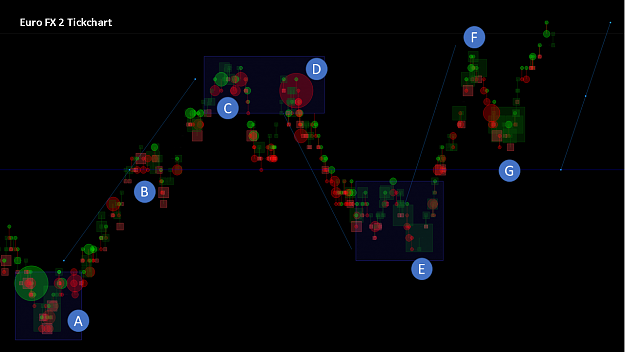

In the following video, I have set up a cluster search in which, using bid and ask, the market divides as follows: buy euro = green square, sell euro = red square, buy dollar = red circle and sell dollar = green circle. The filtering takes into account both a certain number of trades, an imbalance, an identification of the big players, and the delta between ask and bid. The setting is still incorrect, but should clarify the future goal.

Inserted Video

You can already see the individual relationships between bid and ask and the resulting results. The filtering has to be optimized and adapted to individual market situations. From this one can not fundamentally derive a future movement, as the big players often work with a time delay. You must first collect before pushing the course in a particular direction. This approach is interesting in the sideways markets or within an equilibrium. There you can implement the information faster.

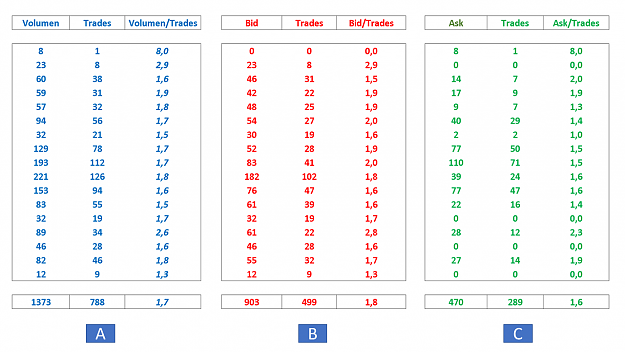

Attached Image (click to enlarge)

Let's summarize the information briefly again

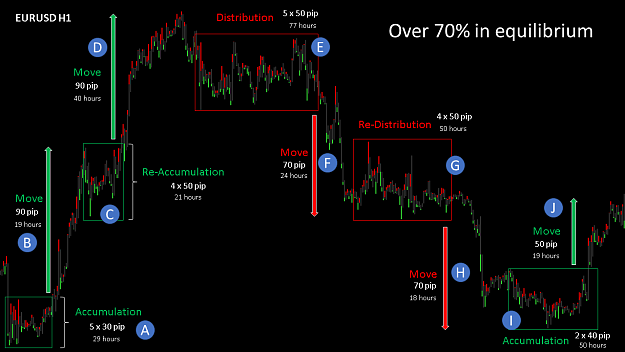

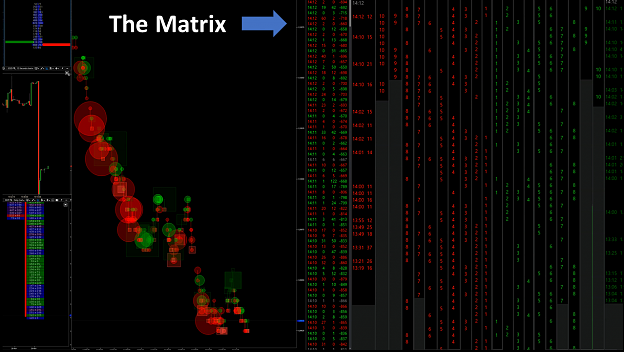

Point A

First, we realize that there is a stronger dollar sale, then the euro is bought on a larger scale, the price goes up.

Point B

Already here, a stronger euro sale takes place, which indicates that the price could not rise so much.

Point C

Already here, the first larger dollar purchases take place, the price goes down for a brief moment and is pushed up again.

Point D

Here comes a big dollar buyer in the market and pushes the price down a bit more.

Point E

In the smaller equilibrium you can see that the euro is bought very heavily at the end and the price goes up.

Point F

The euro sellers hold back first, when the course runs down the dollar is bought heavily.

Point G

Here, the euro is bought stronger and pushes the course again stronger. A short time later, a strong dollar buyer came into the market, pushing the price down.

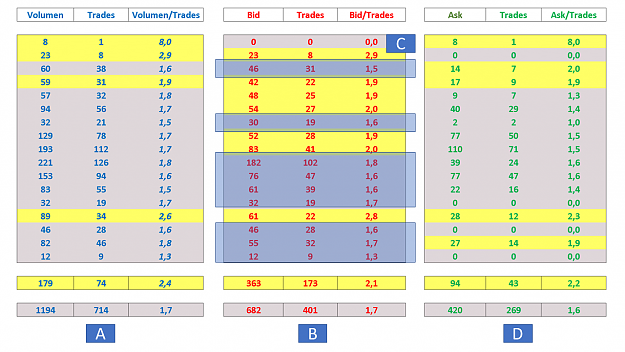

Attached Image (click to enlarge)

If we look at an M1 in EURUSD at the same time, it quickly becomes clear that we can not read this information based on a candle. That is also clear, because the important information of Bid and Ask is missing.

Conclusion

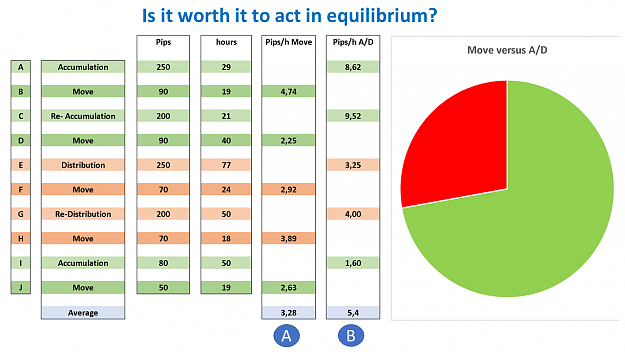

Whether the price rises or falls more or less in the short and long term is unpredictable. Predictable is that the course moves in waves up and down. Trading is always in the direction that promises the most profit for the big players, and that may be identifying in a medium term area. The crucial zones are the sideways markets or an equilibrium. There is often collected in the second half, a larger number of bid or ask, which can anticipate a possible future price course.

With the optimal filtering of individual clusters, it is easiest to be able to recognize what is happening in the market right now. The way the big players work is not like a racing boat but rather a container ship. Sometimes collecting bid or ask can take days before a sharp price move up or down. And a big player does not always have to be active in the market. Often the smaller players are allowed to operate in the market and big players only intervene in certain regions to build certain fake resistance zones, which are then exploited at the crucial moment.

The real stock market data have clear advantages over the Forex data, this is undisputed. But the trick is to filter that stock market data. The information obtained from this must show a trader whether a bullish move is caused by a euro buy or dollar sale. That's a big difference. If the bullish movement comes about through a dollar sale, it is likely that an equilibrium will be created first, and the euro will have to be rebuilt before the price moves higher. If the bullish movement is created by buying more euros, there is a greater likelihood that the market will continue to move higher. In addition, you should also pay attention to Euro sales and dollar purchases.

With the correct filter setting, triggered stops can also be displayed. This is just before major outbreaks a crucial indicator of the future price performance. The challenge is the exact filtering of individual data. And that is the crucial point, which will take a lot of time. In my opinion a decisive strategy to survive in this tough market in the long term.

I wish you a successful trading week

best regards

Forget:That does not work, amateurs build the ark, pros the Titanic!

9