Hi there guys. I am trying to use high quality tick data that I generated for MT4 using QuantDataManager, It already has an "export to MT4" feature so it exports .fxt and .hst files to the proper folders, you just need to choose which MT4 installation you want.

On the article here:

https://fxprosystems.com/how-get-99-...-quality-free/

He says that the backtester will use the .fxt file that is generated by the script (but in this case you don´t even need the script because quantdatamanager already did the job of conversion).

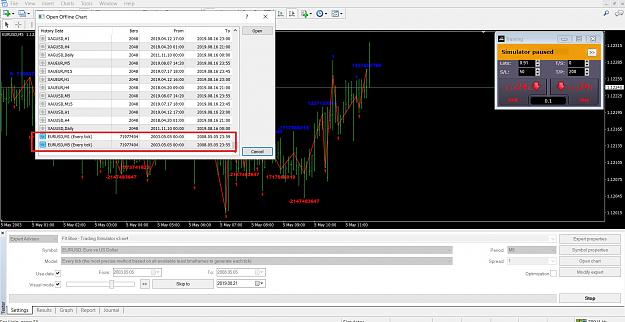

The thing is that the FXBlue trading simulator (which is an EA that uses MT4 backtester to work) is not using the high quality data provided. When it starts the simulation, it seems that it grabs crappy data online, you can see in the screenshot that the wave volume indicator loaded has the values all messed up, because it needs the ticks to work properly, so it confirms that the backtester is probably using some 1min interpolated data or something like that. I had some suspicion because I configured the simulator to generate offline charts so you can open different timeframes in sync with the main testing window, so when I went to open the offline charts I could see that the files generated had a time period that started years before the file I provided (my file starts at 2003.05.05), I thought that the backtester would grab the file I provided and use it as the source to generate the other timeframes. (I generated a 5m "every tick" data file). Is there something I am missing here?

On the article here:

https://fxprosystems.com/how-get-99-...-quality-free/

He says that the backtester will use the .fxt file that is generated by the script (but in this case you don´t even need the script because quantdatamanager already did the job of conversion).

The thing is that the FXBlue trading simulator (which is an EA that uses MT4 backtester to work) is not using the high quality data provided. When it starts the simulation, it seems that it grabs crappy data online, you can see in the screenshot that the wave volume indicator loaded has the values all messed up, because it needs the ticks to work properly, so it confirms that the backtester is probably using some 1min interpolated data or something like that. I had some suspicion because I configured the simulator to generate offline charts so you can open different timeframes in sync with the main testing window, so when I went to open the offline charts I could see that the files generated had a time period that started years before the file I provided (my file starts at 2003.05.05), I thought that the backtester would grab the file I provided and use it as the source to generate the other timeframes. (I generated a 5m "every tick" data file). Is there something I am missing here?

Attached Image (click to enlarge)

Attached Image (click to enlarge)