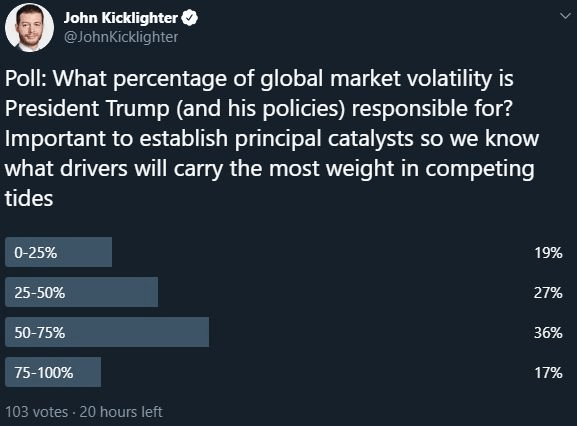

Trade Wars Talking Points:

- Reports from the USTR that some goods would not be swept up in Trump's $300 bln tariff hike charged a 'risk asset' recovery

- The Dow, carry trade, emerging market assets were quick to rally on the news, but follow through is not a certainty in this environment

- Considerations of growth and monetary policy remain key themes but seasonal liquidity will act as a constant headwind to progress

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 3Q 2019? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

Not a Trade War U-Turn, But Trump Turns on the Blinker

The markets were set for a fairly quiet session Tuesday until we were met with another dramatic run of headlines on the topic du jour of late: trade wars. Yet, where the last stretch of meaningful updates weighed the outlook for growth and capital market potential, we were finally met with a break in the clouds this past session. The news began with a headline that could be readily disputed for its impact - that US and Chinese officials had agreed to restart negotiations by phone starting in two weeks. It is easy to play down the importance of this headline given the lack of progress the two sides have made in the past months. Yet, that news was followed by something far more tangible when it was announced by the US Trade Representative's office that a certain group of good from China would be excluded from President Trump's August 1st announcement of the remaining $300 billion in imports into the country for safety, health and national security concerns. It is unclear what percentage of this broad group would fall under this designation.

Even more interesting, as it shows the administration will not pursue its trade war objectives at any cost (including the health of the local economy), was the news that tariffs on a range of electronics and clothing would be delayed from the September 1st implementation date to December 15th. The President said this was to avoid impacting holiday shopping, but it perhaps shows a general appreciation that taxing such consumer goods would have greater weight on US pocket books rather than Chinese businesses. That is not to say the ultimate aim is not the same: whether the burden of more expensive Chinese goods is borne by the foreign producers or local consumers, it will encourage a change of consumption habits. However, influencing local appetites isn't as politically palatable, particularly in the lead up to an election. What is interesting to note for trading/investment purposes from the volatility and headline reversals these past weeks, it seems a considerable amount of market activity falls to the unpredictable decision from the Trump administration.

Better Candidates for an Improved Trade Specific View

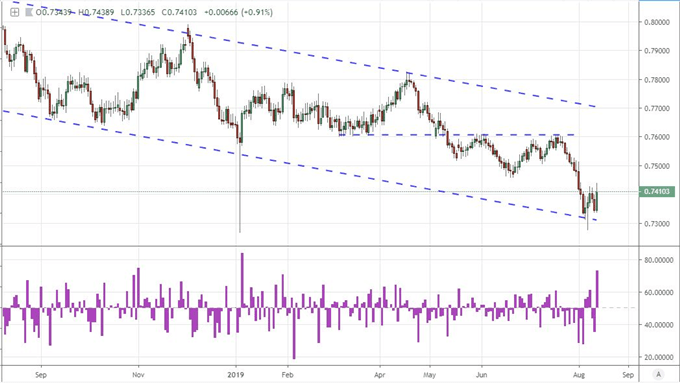

Given the volatility that has followed in the wake of trade war headlines these past weeks and months, this tentative improvement would naturally generate a charge of enthusiasm for risk assets in general along with a host of specific markets that are more directly tied to the US-China trade relationship. Perhaps one of the most impressive moves amongst the FX majors was the bounce from the Australian Dollar. Currency and economy have a distinct relationship to the health of trade and the economic potential it threatens. Having steadily depreciated to a multi-year low on a broad basis, the currency naturally enjoyed a firm bounce Tuesday to pull it off of its absolute lows. In fact, on an equally-weighted basis among its major counterparts, the Australian Dollar enjoyed its biggest single-day rally since the rebound following the January 3rd flash crash. A comparison to more normal conditions would bring us back years. Given how devalued this currency is and its clear connection to the theme, there is greater capacity to take advantage of relief on this front.

Chart of Equally-Weighted Australian Dollar Index (Daily)

Chart Created Using TradingView Platform

Emerging markets are another segment that stood to leverage direct benefit from warmed relations between the two largest economies in the world. The US is the world's largest consumer of finished goods and China its primary buyer of raw materials. An improved outlook for these two economies bodes well for economies whose fundamental health depends more heavily on exports. The EEM Emerging Market ETF posted a healthy recovery this past session, but the disadvantage relative to the all-world equities ACWI remains remarkably pronounced. The same, long climb is apparent with the EM currencies - though here the hole is significantly less deep. The Mexican Peso (USDMXN), Russian Ruble (USDRUB) and Indian Rupee (USDINR) deserve a closer look. This improved balance however isn't substantial enough to change the misfortunes of the Argentine Peso (USDARS).

Chart of EEM Emerging Market to ACWI All-World ETF Ratio (Daily)

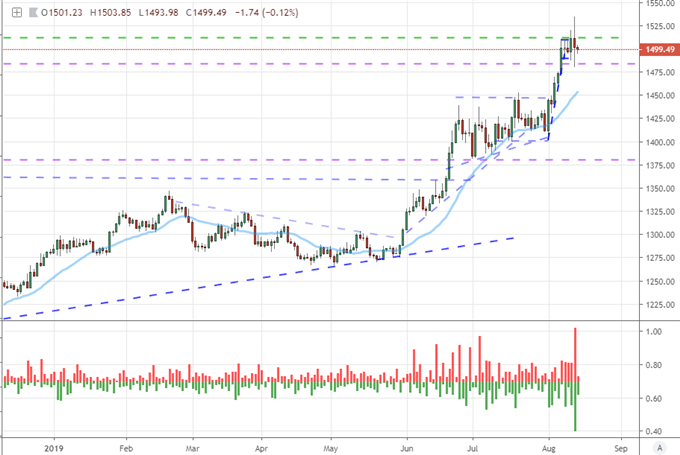

Another uniquely well-turned measure of trade wars in the risk structure is gold - though not as a benefactor of questionable improvement in relationships but rather as a dispassionate measure of how genuine confidence behind the situation. The precious metal responded readily to the day's news with an intraday tumble that was 3.5 percent peak-to-trough. And, despite sliding through 1,490, the market wouldn't charge the break into a full-blown bearish reversal. There is a lot more behind the appeal of this alternative to traditional fiat assets than just the pressure exerted by the US and China stubbornness. The renewed drive of accommodation by the world's largest central bank not only lowers the bounds for yield competition, it works to deflate the value of these pinnacles of valuation.

Chart of Gold and Wicks (Daily)

Chart created using TradingView Platform

The Problem with General Risk Trends: Complacency and Long-Term Value

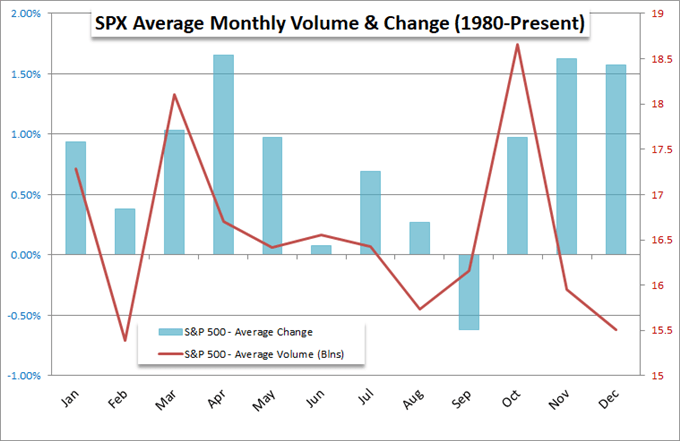

There is a very big difference between the easing of an ever-expanding fundamental threat and the outright emergence of new opportunity for return. The scenario we were presented with this past session distinctly qualifies for the former rather than the latter. The distinction here is clear when we review the criteria. Removing a percentage of the Chinese imports from the tariff list is a material improvement from a ship capsizing quickly. On the other hand, it doesn't represent new opportunity or greater yield that could rouse global investors to push already richly priced assets to even greater heights. If a new speculative wind isn't realized, then we are in turn left with the prevailing environment to shape the investment landscape. As such, we revert to a period of historical restraint in both volume and volatility. These coming few weeks represent the absolute dearth of activity through the Summer Doldrums for the baseline S&P 500. Easing an active risk-off edge will promote a return to complacency which will reaffirm an appetite to let the market's coast.

Chart of S&P 500 Seasonal Monthly Average Performance

This is my contention for the short-term versus lasting response from the more popular risk assets this past session. The Dow led the charge across the range of favorite speculative benchmark. That blue-chip and related US equity indices earned a hearty rally for the session that pushes them back into easy range to retest record highs. It is hard to argue the value add that would justify new record highs given the general backdrop. Even when we remove the relative prospect of record highs, there are serious questions as to the lift for more explicit risk-dependent assets. Global equities for example may be a better value than their US counterpart (just look at the ratio of the SPX to VEU), but the absence of new return still calls into question the appetite for taking any new risk. The ratio hit a fresh record high this past session. A more tempting discount in the risk spectrum with technicals to be boot in my book are the Yen crosses. Carry trade have been far more reticent to follow the heavy swings in risk assets these past years, but they are still significantly discounted. USDJPY cracked a multi-year wedge pattern to start this week, but Tuesday's rally looked to put us back into that pattern. If there were an unrestricted risk drive, this is where I'd look.

Chart of S&P 500 to VEU Rest of World Index Ratio (Daily)

Dollar Crosswinds, Euro's Alternative Status and Pound's Brexit Fixation

Outside of the appropriate representatives for risk assets, we have the systemic players in the FX market. For the benchmark US Dollar, the escalation of trade wars with China seemed to benefit the currency against the likes of the Yuan and Australian Dollar. Then again, it didn't seem to translate into strength compared to its more liquid counterparts: Euro, Yen and Pound. Reversing the trend of deterioration is just as disconnected from the simple equation. An equally-weighted measure of the US currency notably lacked for lift through this past session. That likely has a lot to do with the complications of a relative growth question, the Fed's status with monetary policy moving forward and a host of additional fundamental conflicts.

Chart of Equally-Weighted Dollar Index (Daily)

The Euro isn't a paragon of simplicity itself. The ECB is far more aggressive with its monetary policy ambitions and makes no attempt to hide their interests. Regional growth prospects are troubled, but they are made materially worse against the political uncertainty sourced out of Italy. Add to that the blow-back risks from the Brexit situation and lingering threat from the United States casting its tariff gaze onto Europe, and there is a lot to work against the region and its currency. Yet, one of the key roles the currency is presently playing is the relatively unflappable alternative to an even more unsettled US Dollar. Note that the Euro has firmed broadly these past few weeks and EURUSD dropped - despite a listless Greenback - this past session.

Chart of EURUSD and 5-Day Historical Range (Daily)

Chart created using TradingView Platform

Meanwhile, neither GBPUSD nor EURGBP has established a particularly significant or clear move amid all of this volatility. The upcoming UK inflation figures will hold about as little weight over the primary fundamental interests facing the Sterling as this past session's employment statistics (jobless claims were still fairly large but wage growth accelerated). The indisputable focus for this currency remains the status of Brexit. This past session, the reports of a Prime Minister Johnson clash with Parliament over the ability to navigate a no-deal Brexit scenario continued at a furious pace. A little more interesting - though not at all surprising against recent history - was the report that a group of 20 senior Tory party members headed by Philip Hammond had sent a letter to the PM accusing him of pursuing a destructive path that automatically precluded a scenario that involves a compromise. We discuss all of this and more in today's Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.

What fundamental themes should you follow next week? How will the US CPI and Australian employment updates impact their respective currencies? How will they impact the markets at large? Sign up for our webinars to better evaluate how market developments are shaping markets. Sign up on the Webinar Calendar.