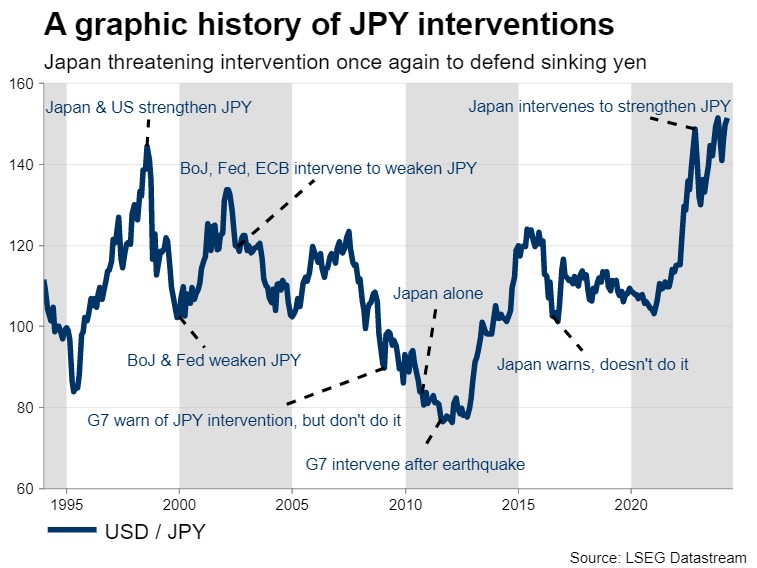

A trading playbook on Japanese FX intervention

Yen falls 7% this year to hit lowest levels in three decades

Japanese authorities threaten to intervene again to defend it

How likely is intervention, and what are the steps to get there?

Yen tanks, again

The Japanese yen absorbed heavy damage this year, briefly falling to a 34-year low against the US dollar. Selling pressures persisted even after the Bank of Japan raised interest rates out of negative territory, leading authorities in Tokyo to threaten another round of FX intervention to defend the currency.

Several factors lie behind the yen’s collapse. First and foremost is the wide interest rate gap between Japan and the United States. Despite the Bank of Japan’s historic move, rate differentials are still extremely wide. As such, capital continues to flow out of Japan, searching for higher returns abroad.

Rising oil prices have been another thorn in the yen’s side, hitting the energy-importing currency through the trade channel. The euphoria in stock markets has further suppressed demand for the safe-haven Japanese currency.

What is the roadmap for FX intervention?

With Tokyo warning it could take action, it’s useful to examine the language officials have used in the past before intervening, and how those threats escalate before actual intervention takes place.

In Japan, the decision to intervene falls on the government, while the execution is done by the central bank. The speed of currency moves is extremely important in deciding whether to intervene. Authorities are more concerned about sharp and sudden FX moves, as those threaten economic stability.

So Japan is more likely to resort to intervention if the yen depreciates at a rapid clip, like it did back in 2022. If the currency is losing ground but at a very slow pace, the risk of intervention would be much lower.

Before actually intervening, Japanese officials will often escalate their verbal warnings in an attempt to scare away speculators that are shorting the currency. This ‘verbal intervention’ process has several unofficial stages.

Stage 1:

We are monitoring developments in the currency market

Desirable for FX rates to move in line with economic fundamentals

Stage 2:

Rapid FX moves can have negative effects on the economy

Excessive movements in exchange rates are undesirable

Carefully monitoring FX markets with a sense of urgency

Stage 3:

Recent moves are driven by speculation and don’t reflect fundamentals

Won’t rule out any options to combat disorderly currency moves

Yen losses have been “excessive” or “disorderly”

Stage 4:

Prepared to take “decisive” or “bold” action against speculative moves

Ready to act against “one-sided” and “excessive” currency moves

“Bank of Japan calls FX dealers to check exchange rates”

The finance minister is the final authority in intervention matters, so when these warnings come from him directly, their importance is greater. We currently seem to be in Stage 4, as finance minister Suzuki recently stressed the government is willing to take “bold measures against excessive moves”. This was his strongest warning so far.

Options market suggests intervention is not imminent

Language aside, the options market doesn’t seem very concerned about an immediate intervention. Implied volatility in short-dated USDJPY options remains fairly low, which shows that big investment funds are not panic hedging against any massive yen moves.

Therefore, options traders seem to view FX intervention as a low-probability scenario for now, perhaps because the speed of depreciation has not been as dramatic as in 2022, when Tokyo intervened twice.

Similarly, the fact that the Bank of Japan hasn’t “called FX dealers to check yen quotes” suggests authorities are not quite ready to take action yet. Of course, that could change if USDJPY slices through the 152.00 region and moves higher rapidly.

The risk of intervention would rise significantly in this case, although Tokyo might still refrain from pulling the trigger unless the pair goes all the way up to the 155.00 - 156.00 area. A lot will also depend on the rally’s momentum. The faster the move, the more likely intervention becomes.

Even if Tokyo steps in, it’s doubtful whether that would lead to a trend reversal in the yen as wide rate differentials would continue working against the currency. Hence, intervention might prevent deeper losses, but is unlikely to ignite a lasting rally in the yen.

Ultimately, the yen needs the global economy to weaken and foreign central banks to start slashing interest rates, before it can stage a sustainable recovery.

Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.