Swiss franc shines bright, but will SNB clip its wings?

Stellar year for Swiss franc, tied for best-performing major currency

End to negative rates, FX interventions, and safety flows helped

Next week's SNB decision and risk tone could decide franc's fate

Flying under the radar

Even though it hasn’t attracted many headlines, the Swiss franc has gone on a silent winning streak. It is virtually tied with the British pound as the top-performing currency of this year, while it has gained more than 3% against both the US dollar and the euro. Against the bruised Japanese yen, the franc has appreciated by around 15%, pushing the franc/yen cross to new record highs.

Several elements lie behind this impressive performance. First and foremost has been the Swiss National Bank’s exit from negative interest rates. With the central bank raising rates back into positive territory, global depositors are no longer penalized for parking their cash in Switzerland.

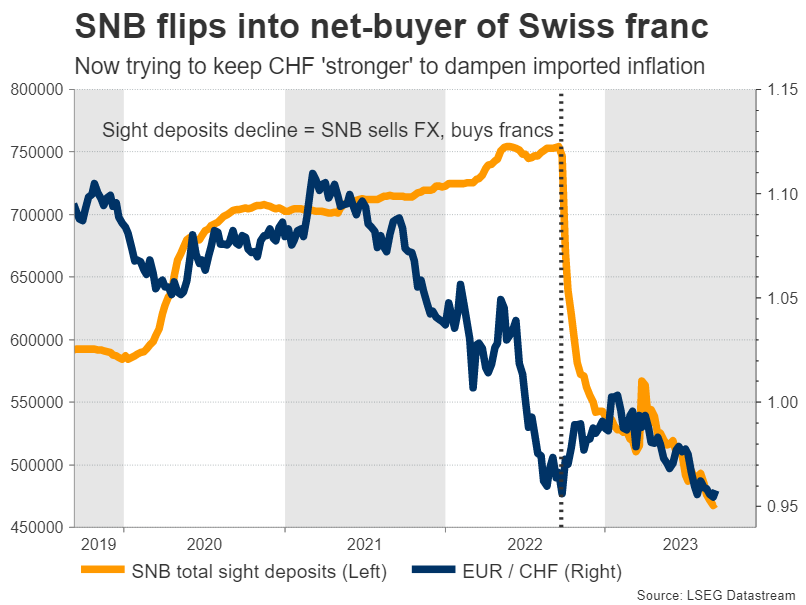

Direct FX interventions have also played a role. The SNB has been active in the currency market for a long time, but last year it flipped from a net-seller of francs to a net-buyer, in an attempt to strengthen the currency and exert downward pressure on imported inflation.

This can be seen through sight deposits at the SNB, which are considered a proxy for foreign currency purchases. Sight deposits have fallen sharply over the past year, revealing that the central bank has been actively selling foreign currencies and buying francs on the open market.

A quiet flight to safety likely helped the franc too. Because of Switzerland’s chronic current account surplus, the franc often acts like a safe haven instrument, especially when the Eurozone economy encounters trouble. With business surveys warning the Eurozone is headed for a mild recession, this dynamic probably came into play.

What’s next? All eyes on SNB

Looking ahead, there are both positives and negatives on the horizon. Arguing in favor of further franc gains is the worsening economic data pulse in Europe and China, which might continue to fuel safe-haven flows.

Any correction in high-flying US stock markets could have similar effects. That’s a real risk considering that equity valuations are stretched, earnings have been stagnant for three quarters now, and bond yields are trading near their highest levels of this cycle.

However, the Swiss economy has also started to lose steam, which in turn might give the SNB cold feet. In the second quarter, GDP growth was running at just 0.5% from a year ago, slowing down sharply as the stronger franc dampened demand for exports and capital investments stalled.

Similarly, inflation has cooled off. The yearly CPI rate clocked in at 1.6% in August, staying below the central bank’s 2% target for a third month. That said, the SNB anticipated this cooldown in its latest forecasts and still maintained a tightening bias, warning that inflation would reaccelerate next year because of higher electricity and rent prices.

Therefore, the immediate question facing the franc is whether the SNB will raise rates next week. Growth is losing power and recession risks cannot be ignored based on global trends, but at the same time, the recent spike in energy prices could make the SNB even more concerned about stubborn inflationary pressures.

That leaves the SNB with a difficult choice: keep rates unchanged to safeguard economic growth or raise them to eradicate inflation? Market pricing is currently leaning towards no action, assigning a 60% probability for the SNB to pause next week versus 40% for another rate hike.

Whether the European Central Bank raises rates on Thursday will be a key variable in this decision. The SNB usually follows in the ECB’s footsteps, mimicking the moves of its larger neighbor so that interest rate differentials don’t widen too much and put pressure on exchange rates.

Speaking of exchange rates, the SNB’s stance on FX interventions needs to be monitored closely. For now, the SNB is buying francs to dampen imported inflation, but that could change if inflation doesn’t reaccelerate. It’s probably too early for such a shift next week, but it’s a clear risk moving forward.

Big picture

Blending it all together, the franc’s fortunes will be tied mostly to FX interventions and the global economy. With global growth slowing while the SNB continues to boost the franc through interventions, the near-term landscape seems favorable, even if there is a setback next week in case the SNB holds rates steady.

That said, the franc’s performance will also depend on the currency it is matched against. For instance, the franc could outperform the growth-starved euro, and might also outshine the yen, which has been decimated by Japan’s refusal to abandon negative rates.

The catch is that the franc might struggle to record any further gains against the US dollar, which is backed both by a resilient economy and safe-haven qualities. A period of risk aversion in global markets would benefit both currencies, so the deciding factors might be interest rate and growth differentials, which seem to favor the dollar.

Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.