The US unemployment report for August showed modest job growth, a slowdown in wage growth, and a relatively sharp jump in the unemployment rate, all clear signs that the US labor market is normalizing. It's challenging to expect inflation to accelerate in this context, so the likelihood of the Federal Reserve raising interest rates in September and possibly in November is diminishing.

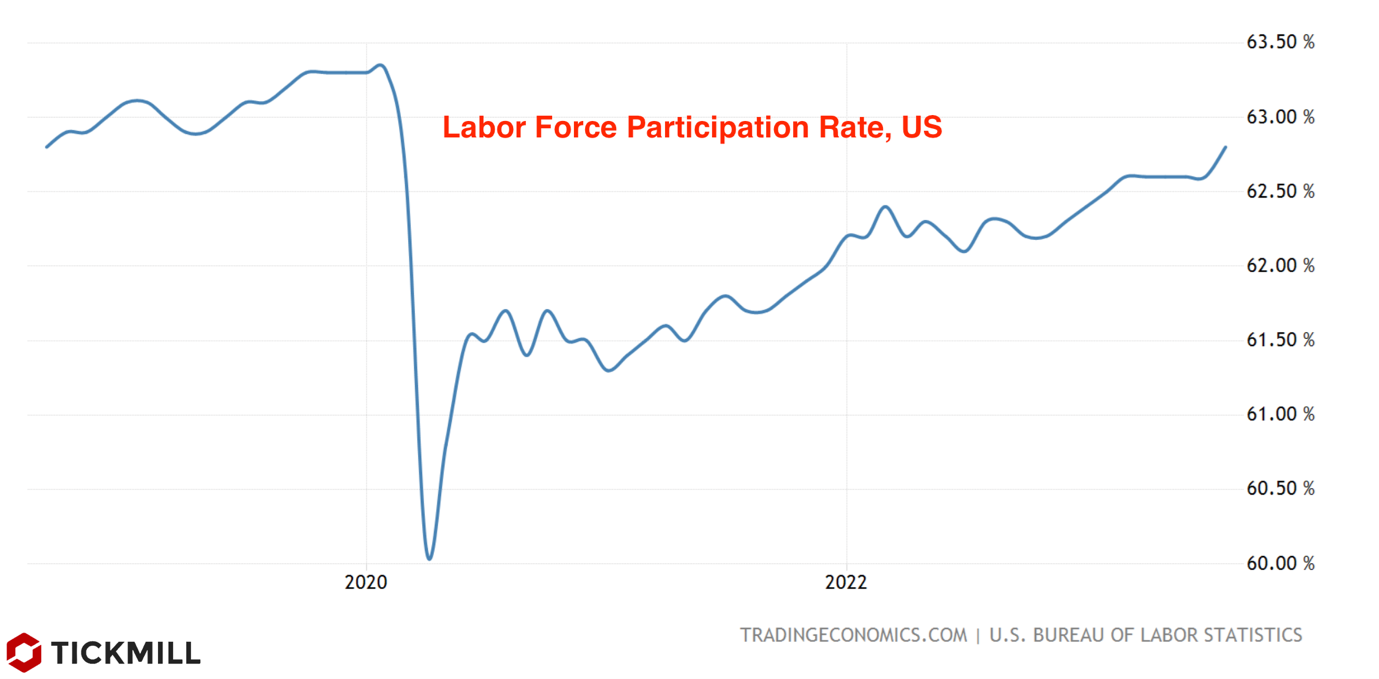

Job growth in the US in August reached 187,000, slightly surpassing the modest forecast of 170,000. However, the previous two months were revised downward by a total of 110,000 jobs. The report adds weight to the argument that there is a sustained trend of weakening in hiring. In the private sector, the increase was 179,000, with 102,000 of those jobs coming from the private education and healthcare sector. A positive development in terms of its impact on inflation is the increase in the labor force participation rate – a measure calculated as the sum of unemployed and employed individuals as a percentage of the total working-age population. An increase in this rate means a "net" inflow into the category of those who are either employed or actively seeking employment, which should exert downward pressure on wages and, subsequently, consumer inflation in the US. The decline in this rate in 2020 led to the phenomenon of sustained inflation pressures, which the labor market continues to generate. With its return to normal levels, this effect is likely to be a deflationary factor:

Along with the rise in the labor force participation rate, wage growth is also starting to slow down, with August recording a 0.2% MoM increase compared to a forecast of 0.3%. This marks the first drop below 0.3% in over six months. The unemployment rate jumped from 3.5% to 3.8%, clearly indicating a slowdown in the pace of labor demand growth.

The probability of the Federal Reserve raising rates in September in the face of such soft figures is sharply decreasing, and the pause is likely to extend into November.

The markets did not see anything critical in the unemployment report in terms of recession risks in the US. Short-term Treasury yields returned to levels preceding the report release after a brief dip, and long-term bond yields even increased slightly, from 4.10% to 4.18% for 10-year Treasury bonds. Consequently, the report had no significant impact on the US dollar, which strengthened against major currencies after a brief bearish correction. The dollar index rose from 103.50 to 104 points, and the price formed a chart pattern rebounding from a support line, which previously acted as resistance, serving as a confirmation of bullish intentions:

This week, we can expect the release of the US ISM Services PMI on Wednesday, which will also include respondents' assessments of hiring conditions and price pressures and is expected to be closely watched by the market. In Europe, the third estimate of second-quarter GDP growth will be released on Thursday, and Germany's inflation report will be published on Friday.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 70% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.