US and European stock indices are on a slippery slope, the Dollar index found enough buyers to rebound from 101 level after the dip on Monday. The selling catalyst was disappointing report from the Dallas Fed regarding activity in US manufacturing sector. The corresponding index dropped to -23.4 points missing the forecast of -14.6 points. This is the lowest reading since July 2022:

Investors apparently opted to reduce risk exposure ahead of earnings releases of major US companies this week, such as GOOG, META, AMZN and MSFT.

Comments of the ECB representative Schnabel supported European currency. According the official, it is still possible that the ECB will raise rates by 50 basis points next week.

US Treasury yields are gradually drifting lower, as the scenario of a significant slowdown in the US growth in the second quarter (which the Fed also warned about) becomes more likely. The incoming data speaks in favor of these concerns. Specifically, retail sales and the Dallas Fed index, which turned out to be significantly weaker than expectations.

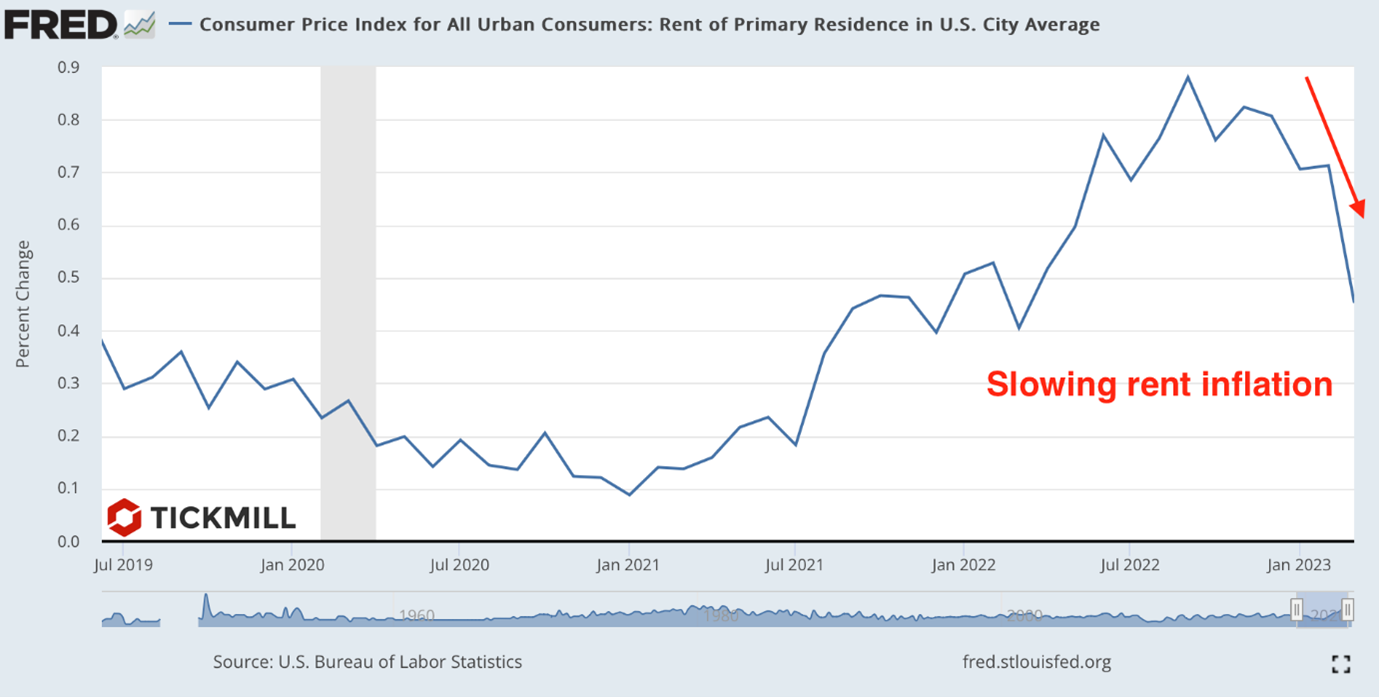

Investors' attention today will be riveted to the data on consumer confidence from the Conference Board, as well as the index of activity in the manufacturing sector from the Richmond Fed. Risks on both indicators are shifted towards weaker prints, which may further constrain the activity of buyers in the US stock market and increase pressure on the Fed to provide the markets with a more friendly forecast for the policy path at the upcoming meeting. Some interest may cause data on the real estate market in the US, in particular the price index from Case-Schiller. It is well known that consumer inflation, with a lag of several months, reacts to changes in housing prices (through changes in housing rental rates, from which, among other things, consumer inflation is calculated):

As for the Fed meeting next week, the main question is what the Fed will do after the May rate hike (which seems to be beyond doubt). And while future policy is once again heavily dependent on incoming economic data, shocks to the banking sector are back on the radar, with First Republic Bank reporting a larger-than-expected deposit outflow. The news pulled the US bank stock index down after five days of rally:

Tomorrow there is a risk of a fresh sell-off of the dollar after release of data on orders for durable goods in the US. After a 1% decline, a 0.7% rebound is expected, the market may not be prepared for a weak print and may shift Fed expectations towards a more dovish one in cases of a downbeat print.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 70% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.