- Dollar loses ground after dismal US payroll data.

- USD/JPY directionless until Friday’s NFP disappointment.

- US equity and credit markets recover after initial shock.

- Labor shortage may fuel wage inflation, Treasury yields resilient.

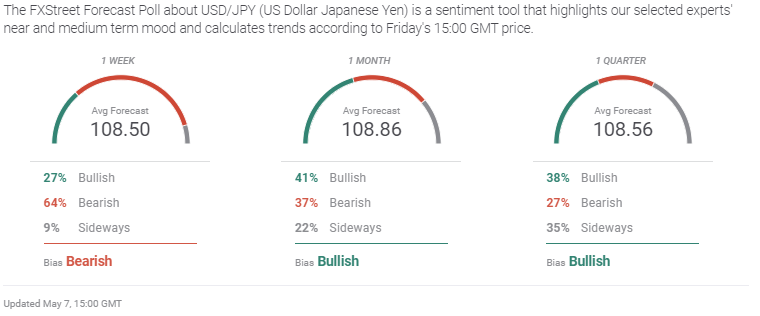

- FXStreet Forecast Poll is neutral on USD/JPY prospects.

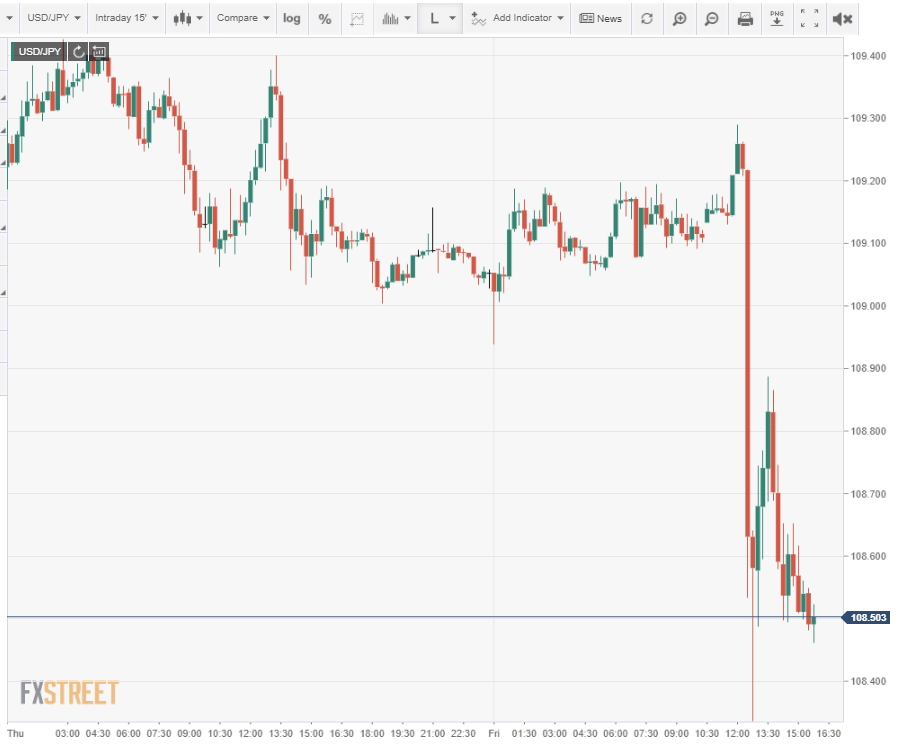

The USD/JPY dozed from Monday’s open at 109.36 to Friday’s 109.17 approach to the US Nonfarm Payrolls report (NFP), then woke with a start as the US economy added just one-quarter of the expected jobs.

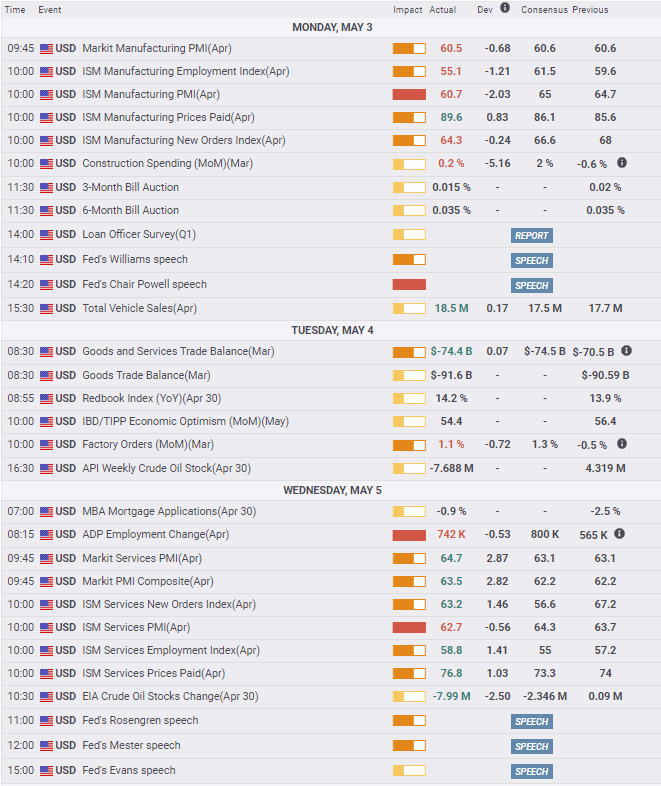

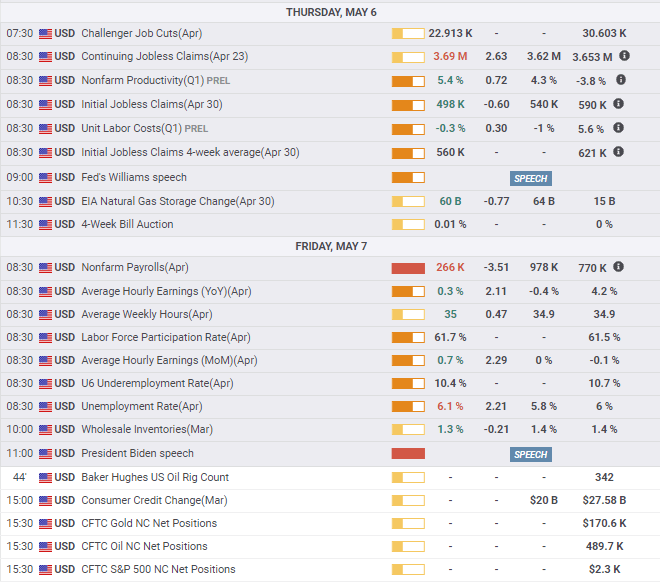

American firms hired 266,000 people in April and the unemployment rate rose to 6.1%, according to the US Department of Labor. A far better report had been expected with a 978,000 consensus estimate for payrolls and a 5.8% unemployment rate.

Initial reaction sent the USD/JPY cascading from 109.22 as low as 108.34 in the first 30 minutes following the 8:30 am EDT release. The USD/JPY rebounded to 108.89 before fading again.

Treasury yields mirrored the sell-off in the dollar. The 10-year yield fell from 1.56% to 1.52% but recovered its losses by the early New York afternoon.

US 10-year Treasury yield

CNBC

The NFP figures justify the Federal Reserve’s caution in cutting back on economic support. As Chairman Jerome Powell said after the FOMC meeting two weeks ago, “We have had one good jobs report, that is not enough.”

Equities rose with the Dow, S&P 500 and Nasdaq all higher in morning trading as the weak payroll report makes continued Federal Reserve rate and liquidity intervention a certainty.

The puzzle of April's job numbers may take a month to work out.

US economic growth was 6.4% in the first quarter. It is not projected to be any less in the second.

Many industries report shortages of workers, particularly in skilled manufacturing roles and in the restaurant and hospitality business. How can there be 8.4 million or more unemployed and shortages of waiters and waitresses?

Were payrolls weak because employers could not find workers to hire? How many jobs are going begging for lack of interest?

The unexpected rise in Continuing Jobless Claims in the latest week may offer a clue. Lower wage workers may be reluctant to return to jobs that do not pay appreciably more than unemployment insurance.

On the other hand the surprising April NFP numbers could be a statistical oddity, generated by Bureau of Labor Statistics seasonal adjustments.

The unadjusted figures show 1.089 million jobs gained in April. Seasonal revisions are based on historical models. If the adjustment to seasonal norms produced the swing, it could return in May.

In defense of the statisticians, there was nothing historical or normal about the past year and standard adjustments founded in prior year assumptions are likely to prove ungrounded.

There is no indication in other statistics that the US recovery is faltering, only that employers are having great difficulty finding help.

Good-to-excellent US data earlier in the week from the Institute for Supply Management and Automatic Data Processing turned out to be a poor guide for April’s Employment Situation Report.

Purchasing Managers Indexes in manufacturing and servics declined slightly in April from their pandemic, and for factory sentiment all-time, highs in March.

The dip in manufacturing outlook was related more to frustrations in supply and hiring than in any diminution of business. New Orders in both sectors remain exceptionally strong and what is more important have been so for six months and longer.

The Services Employment Index rose to its best score since September 2018 and the manufacturing measure though lower, remained firmly in expansion. Initial Jobless Claims, the forerunner last March of the oncoming economic storm, fell to their lowest pandemic level, below 500,000 for the first time in 13 months.

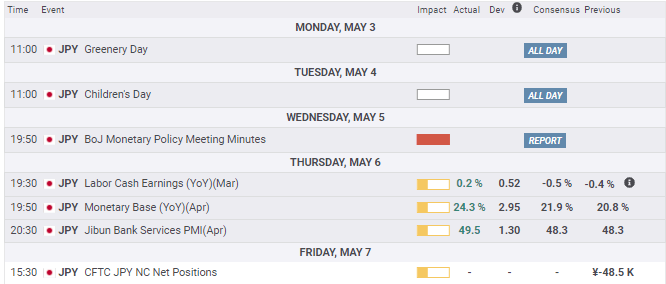

Japanese economic information was negligible this week and of no market impact.

USD/JPY outlook

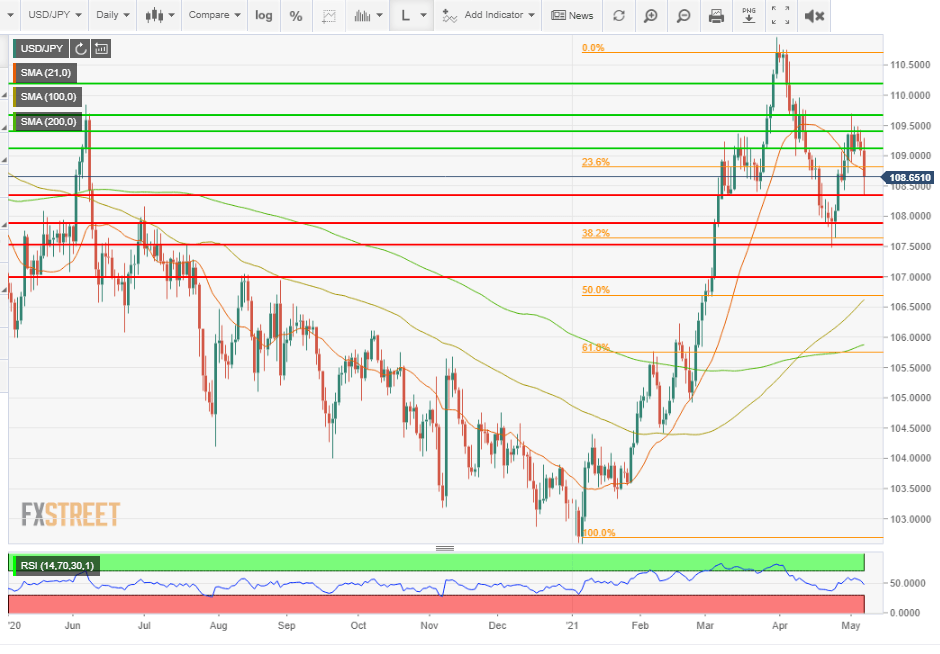

The USD/JPY remains dependent on Treasury rates and will be hard-pressed to regain the initiative until faster job growth and the premise of rising yields return. That said there is little case for a sharp drop in the week ahead with a gradual decline most likely.

Technically, support at 108.00 marks the lower boundary of the range since early March and should prove adequate to thwart an initial break. Below that there is scarce support until the next big figure at 107.00.

The promise of higher US Treasury rates as the economy heats up has been reduced but only marginally. Treasury yields for the 10-year bond rose despite the huge miss on payrolls.

Labor shortages highlighted by the jobs report will exacerbate US inflationary pressures already under strain from fast-rising commodity prices and consumer demand. Employers have been forced to increase wages to attract workers. However, with more than eight million unemployed, the worker scarcity should not last.

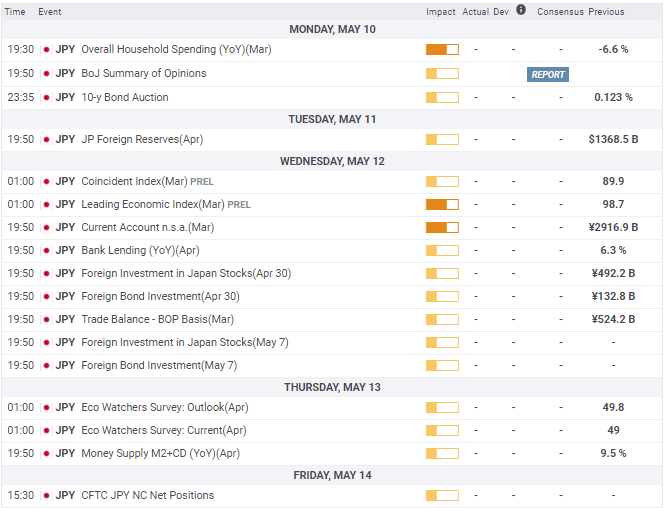

In the week ahead, overall Japanese Household Spending for March and the Eco Watchers Survey will give some indication of the directions of the consumer and domestic economies.

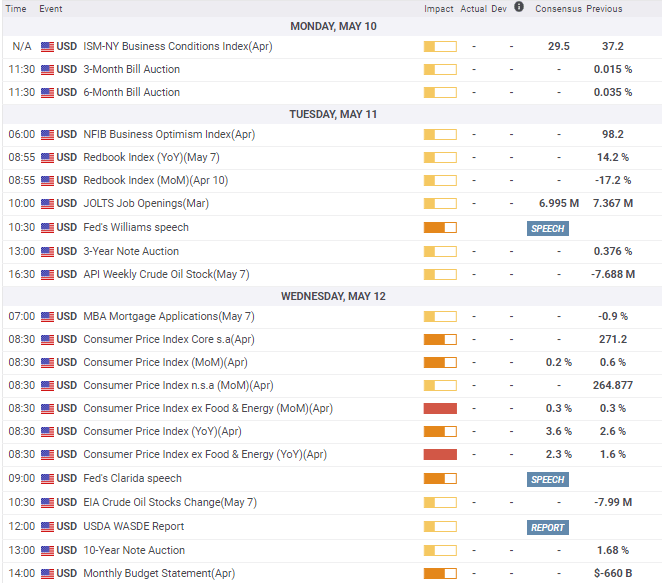

As is the case most weeks, currency markets will primarily attend to information from the US side of the pair.

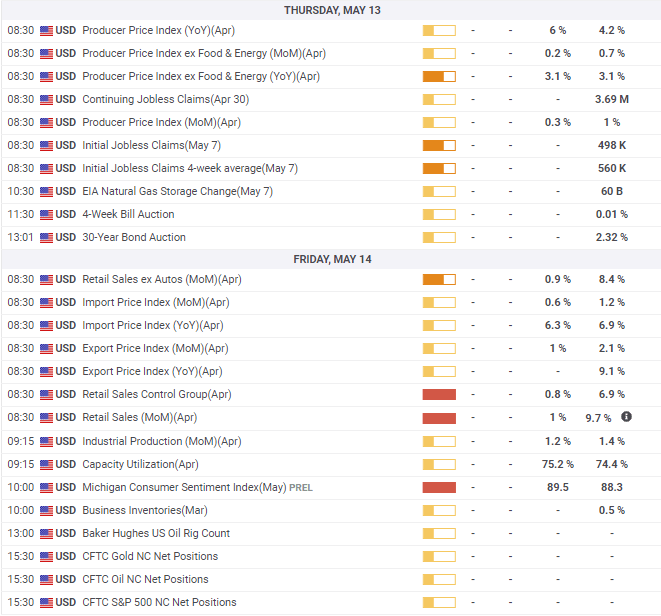

April US Consumer Prices on Wednesday followed by Producer Prices on Thursday will command even more attention after the NFP report.

The Federal Reserve has stated repeatedly that any increases in inflation will be limited and temporary and the product of base effects from last year's lockdowns.

While that may be true, fast rising commodity prices, production shortages and consumer demand are now joined by the increasing probability of wage inflation as businesses struggle to find workers.

Either way, a 1% jump in the headline CPI rate in one month is eye-catching, especially as it reinforces what consumers are seeing every day.

Higher US inflation is a plus for the dollar.

Japan statistics May 3–May 7

US statistics May 3–May 7

Nonfarm Payrolls were a huge miss but except for the lower dollar generated surprisingly little negative market reaction. Equities rose and the yields curve steepened. The payroll weakness appears to have been produced by an inability to fill the plentiful open jobs not by any economic downturn.

FXStreet

Japan statistics May 10–May 14

The Eco Watchers Surveys for April are the most timely but will have scant trading impact.

US statistics May 10–May 14

Nonfarm Payrolls have underlined the vulnerability of wages to rising expectations as employers struggle to find workers. April CPI on Wednesday and PPI on Thursday will speak to the inflation dilemma with higher results supporting the dollar. Retail Sales for April should remain healthy though resuming a more normal aspect after the rampant first quarter.

USD/JPY technical outlook

The 38.2% Fibonacci level of the 2021 USD/JPY gain (102.70-110.71) is still the most important long-term technical point suggesting the pair remains bid despite the recent drop from 109.50. Support at 108.35 provided a quick turnaround after the surprise NFP result. The Relative Strength Index has dropped to neutral hinting at a somewhat equivocal immediate future.

The 21-day moving average (MA) is minor resistance at 108.76. The 100-day MA at 106.62 reinforces the 50% Fibonacci at 106.69 and the 200-day MA at 105.88 is out of the current picture. The multiple and recent resistance lines assist the overall lower bias brought on by weakening US Treasury yields.

Resistance: 109.10, 109.40, 109.65, 110.20

Support: 108.35, 107.85, 107.50, 107.00

USD/JPY Forecast Poll

The FXStreet Forecast Poll reflects the fundamental advantage of the US dollar over the yen as long as US rates keep their upward bias.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

EUR/USD: The first upside target is seen at the 1.0710–1.0715 region

The EUR/USD pair trades in positive territory for the fourth consecutive day near 1.0705 on Wednesday during the early European trading hours. The recovery of the major pair is bolstered by the downbeat US April PMI data, which weighs on the Greenback.

GBP/USD rises to near 1.2450 despite the bearish sentiment

GBP/USD has been on the rise for the second consecutive day, trading around 1.2450 in Asian trading on Wednesday. However, the pair is still below the pullback resistance at 1.2518, which coincides with the lower boundary of the descending triangle at 1.2510.

Gold price struggles to lure buyers amid positive risk tone, reduced Fed rate cut bets

Gold price lacks follow-through buying and is influenced by a combination of diverging forces. Easing geopolitical tensions continue to undermine demand for the safe-haven precious metal. Tuesday’s dismal US PMIs weigh on the USD and lend support ahead of the key US data.

Crypto community reacts as BRICS considers launching stablecoin for international trade settlement

BRICS is intensifying efforts to reduce its reliance on the US dollar after plans for its stablecoin effort surfaced online on Tuesday. Most people expect the stablecoin to be backed by gold, considering BRICS nations have been accumulating large holdings of the commodity.

US versus the Eurozone: Inflation divergence causes monetary desynchronization

Historically there is a very close correlation between changes in US Treasury yields and German Bund yields. This is relevant at the current juncture, considering that the recent hawkish twist in the tone of the Fed might continue to push US long-term interest rates higher and put upward pressure on bond yields in the Eurozone.