Dual milestone: down $1 trillion & below $8 trillion. Fed shed 26% of Treasuries it had added during pandemic QE.

By Wolf Richter for WOLF STREET.

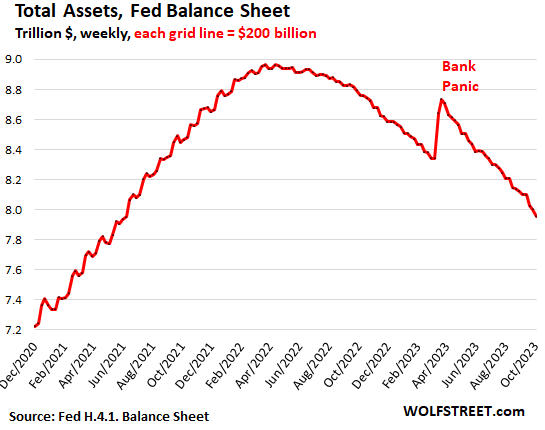

This is a big milestone of the Fed’s Quantitative Tightening (QT): Total assets dropped by $1.01 trillion since peak-QE in April 2022, to $7.96 trillion, the lowest since June 2021, according to the Fed’s weekly balance sheet today.

In September alone, total assets dropped by $146 billion as another big chunk of bank-panic support unwound.

Total assets have now dropped 11.3% from the peak.

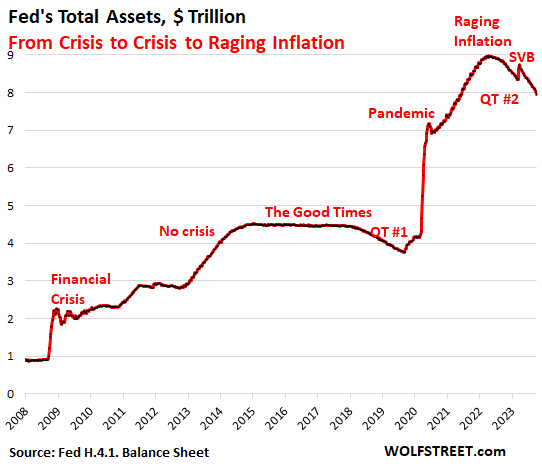

From crisis to crisis to raging inflation:

During QT #1 between November 2017 and August 2019, the Fed’s total assets dropped by $688 billion. During QT #2 so far, which started ramping up in the summer of 2022, the Fed has already shed $1.01 trillion.

But the Fed’s QE pile got huge during the pandemic, and there’s a lot more to take off the pile, and markets are finally waking up to it, with 10-year Treasury yields now closing in on 5% and the 20-year yield over 5%, after short-term yields have been over 5% for months.

And inflation is still about twice the Fed’s target, while during QT #1, the Fed was just trying to “normalize” its balance sheet with inflation at or below the Fed’s target:

QT on track.

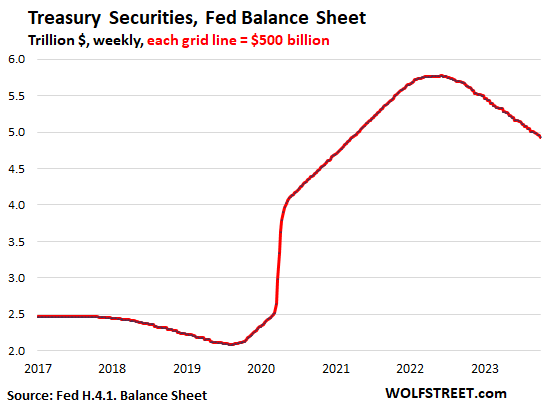

Treasury securities: -$58 billion in August, -$840 billion from peak in June 2022, to $4.93 trillion, the lowest since March 2021.

The Fed has shed 26% of the Treasury securities it bought during pandemic QE (of $3.27 trillion).

How the Fed’s QT works: Treasury notes (2- to 10-year securities) and bonds (20- & 30-year securities) “roll off” the balance sheet mid-month or at the end of the month when they mature and the Fed gets paid face value for them. The roll-off is capped at $60 billion per month, and about that much has been rolling off, minus the inflation protection the Fed earns on Treasury Inflation Protected Securities (TIPS) which is added to the principal of the TIPS.

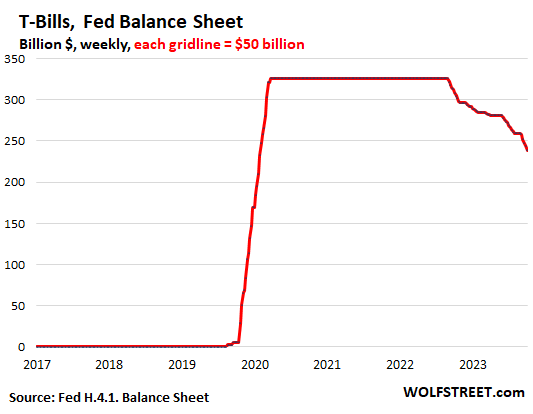

How short-term Treasury bills fit into it. In months when the roll-off of notes and bonds is less than the cap of $60 billion, the Fed lets short-term Treasury securities (1-year or less) roll off in the amount of the shortage to get to the $60-billion cap.

These T-bills are included in the overall Treasury securities of $4.93 trillion on the Fed’s balance sheet. But by looking at them separately, we can easily see which month, and by how much, the roll-off of T-notes and T-bonds is less than $60 billion.

When QT started, the Fed had $326 billion in T-bills that it constantly replaced as they matured by buying new T-bills at auctions (in the auction results, “SOMA” is the Fed). This is evidenced by the flat line in the chart below.

In September, the Fed needed to let $20 billion in T-bills roll off to make up for the $20 billion by which the roll-off of T-notes and bonds was below the $60 billion cap.

Since the beginning of QT in June 2022, the Fed has burned through $67 billion of its $328-billion stash of T-bills to keep the roll-off at the cap of $60 billion. So just looking at the chart, we can guess that the Fed has enough T-bills to keep the roll-off at $60 billion for about two years. Once the T-bills are burned off, the roll-off will decline to whatever pace the then much smaller amounts of T-notes and bonds roll off.

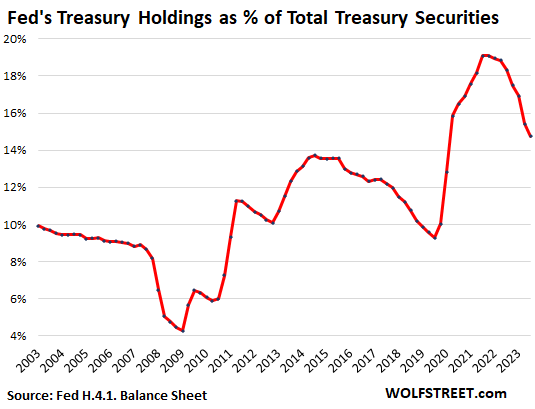

As % of gross national debt: The Fed’s holdings are now down to 14.7% of total Treasury securities outstanding at the end of September, down from 19.1% at the peak. The drop in the percentage is a result of the QT drop in Treasury securities on the Fed’s balance sheet, and the gigantic leap in the gross national debt to $33.4 trillion, amid a tsunami of new issuance of Treasury securities.

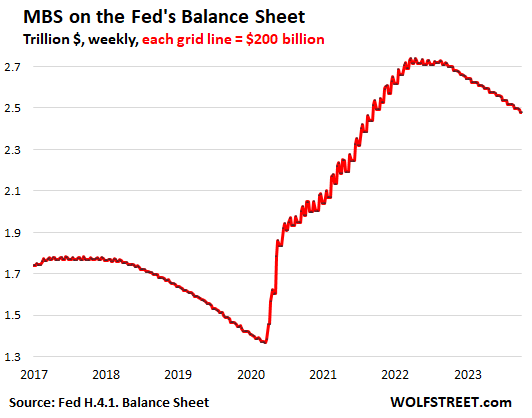

Mortgage-Backed Securities: -$19 billion in September, -$260 billion from the peak, to $2.48 trillion, the lowest since September 2021.

The Fed only holds government-backed MBS, and taxpayers carry the credit risk. MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made.

The spike in mortgage rates has caused home sales to plunge and refis to collapse, which slowed the mortgage payoffs, and therefore the pass-through principal payments to a trickle. So the MBS run-off has been between $15 billion and $21 billion a month, well below the $35-billion cap.

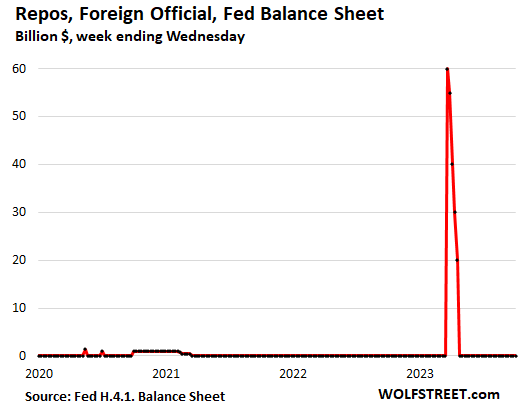

The bank-panic measures unwind.

Repos with “foreign official” counterparties were paid off in April. The Swiss National Bank likely used them to fund its dollar-liquidity support for the take-under of Credit Suisse by UBS.

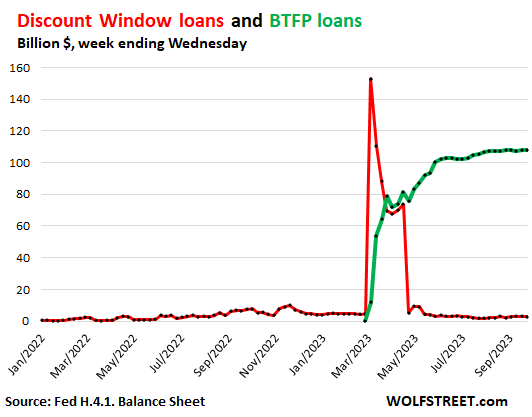

Discount Window: roughly unchanged in September, at the near-nothing level of $2.7 billion, compared to $153 billion in bank-panic March (red line in the chart below).

Discount Window lending to banks is as old as the Fed. This is expensive money: since the last rate hike, the Fed charges banks 5.5%, and banks have to post collateral under strict conditions and at “fair market value.” Banks pay off these Discount Window loans as soon as they can.

Bank Term Funding Program (BTFP): roughly unchanged in September and August, at $108 billion (green line).

The BTFP, created during the bank panic, is less punitive and more flexible than the Discount Window. Banks can borrow for up to one year, at a fixed rate, pegged to the one-year overnight index swap rate plus 10 basis points. And the collateral is valued at purchase price rather than at the lower market price.

This facility is tiny compared to the $22.8 trillion in commercial bank assets held by the 4,100 commercial banks in the US.

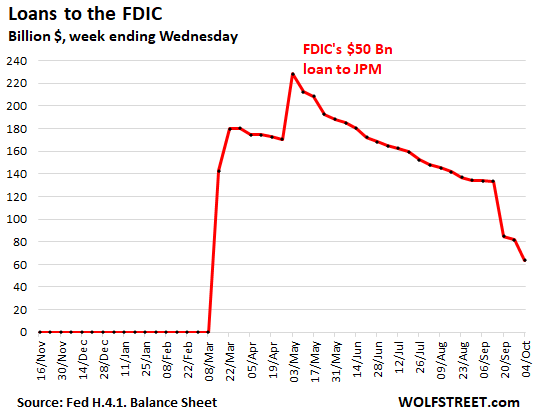

Loans to FDIC: -$70 billion in September, to $64 billion.

The FDIC is making progress in selling the assets that it took on with the takedowns of Silicon Valley Bank, Signature Bank, and First Republic. After the asset sales close, the FDIC sends the proceeds from the sales to the Fed to pay down the loan balance.

And here is my take on what this QT has already caused in the stock market, bond market, and Commercial Real Estate market — a lot of bloodletting — and what it will cause in those markets going forward: THE WOLF STREET REPORT: Stocks, Bonds & CRE Face QT

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

So at least 4-5 years more to go?

Who thinks we’ll make it anywhere near $4T or less before QE ramps up again?

Going once, twice? Sold!

who is buying? coz they arent tje only ones selling

When the yield is high enough, lots of people are buying. Yield solves all demand problems.

The current yield is high enough to attract lots of buyers, which is why the auctions are oversubscribed, and why every single Treasury can be sold in the market. You just have to offer a yield that is appealing. If the 10-year Treasury yield hits 5%, there will be a flood of buying. And then when those buyers are satisfied, and more sellers appear, then the yield may go to 5.1%, and there will be a flood of buying. I’m going to buy eventually when the yield is high enough.

You make it sound like there is always a buyer. Isn’t it logical that at some time the market can no longer absorb the old (rolling off) plus the new treasuries? QT is supposed to take away liquidity. And the interest due is no longer being ‘printed’ by the FED.That makes that saturation point to be reached sooner than later. Except when someone, like the FED, starts creating new buy-dollars again. As buyer of last resort.

Wolf, can you explain how it’s possible that the (TLT) 20 & 30 Year US Treasury ETF is down roughly 15% since around the 1st of July and the Fed has only had to make loans under BTFP of $4 Billion?

To me, it seems like BTFP should be exploding right now with rates sky rocketing (which means lower valuations for MBS and Treasuries.). Is it because these assets are held yo maturity and BTFP is only needed if too many depositors want their money back? And it seems like most large depositors have already moved their dollars to T-Bills, or is that still ongoing?

Also, do you really expect the banks to repay their BTFP loans in March when the 1 year loan is due and get their worthless collateral back?

Lastly, is BTFP available to just banks, or can pensions and insurance companies get these loans too?

Banks are in much better shape than what you read on sites that are praying for a financial collapse. The problem banks run into is that depositors yank all their money out all at once (run on the bank). If there is no run on the bank, banks are fine. Banks are paying more interest and are keeping their depositors. They figured it out. Bank profits are going to slide because they’re paying their depositors more, but that’s fine, not going to hurt anyone except stockholders.

“Yield solves all demand problems” is probably one of the most crucial concepts in investing.

As an axiom, it belongs beside Bernstein’s “In investing, risk and reward are joined at the hip” and Graham’s voting/weighing machine.

Wolf is it a good time buy US T-bills ? Do you have any hood source ( article or book) about it? Just wanted to see if we can invest in it for few years before starting to invest in stocks.

When I buy treasuries, the treasury has to repay me my principal, when the security matures. So, I get paid the coupon interest rate plus my principal back at the end.

When the Fed buys treasuries from the treasury, does the treasury have to pay back the principal to the Fed, when the security matures?

I assume it does not, and if so, then this is how QT causes the money that was injected into the economy to goes “poof”, correct?

Let me know if I’m wrong. Please point me to any article(s) you’ve written the really explains how the Fed’s QE works in reverse with QT, specifically as it relates to the money being sucked out of the money supply.

Thanks, Wolf!

It seems that it headed to under 7 trillion by end of 24 but would the fed ignore a permanently lower equity price if the inflation is under 3% a year from now and continue with the QT?

The Fed heads are already talking about letting QT continue even as they might cut rates in the future to keep them closer but above core PCE inflation — they’re assuming the best-case scenario that core PCE will continue to drop.

This is an important milestone. I hope the fed stays on this course, at least two more years. Contrary to the expectations of Wall Street, they must definitely let QT to continue even if they start cutting the rates. Otherwise the asset prices stay at ridiculous levels or even increase more. Inflating the balance sheet helps to avoid recessions (as in 2023 spring), but it manipulates the asset prices, resulting with consumer inflation and inequality.

Some people may feel richer, happier and feel that the economy is good when fed prints money and they see their home price increases every time they check zillow, but such kind of economies are unproductive and raises inequality badly. If you wonder, check out countries like Russia (even before the Ukraine war). A tiny apartment was as expensive as a house in U.S in a similar sized city. May be worse now. But they were not wealthy or happy. NO COUNTRY CAN PROSPER BY (JUST) BUYING AND SELLING DIRT (I.E LAND).

Where are you getting your numbers? Redfin says the median home price in the City of Moscow is $50,000 USD. I live in a small rural County of 16,000 people in the US and our median home price is $1.2M.

jr,

Redfin in Moscow? Moscow, Idaho? 🤣 People, you need to be a little more careful when just google around.

So there are apartments for sale in Moscow, Russia, and they’re expensive. Lots of them are over $1 million USD. Here is a cheap one that I found for sale: 2-room apartment 66 sqm (=710 sq ft) on the 11th floor, Moscow, Leningradsky prospect, 36 building 36: $480,000.

You can google: Moscow Russia apartments for sale

…just for fun-

…back in the ’70’s when I was taking the long and working road to my degree in geography, much mirth resulted in viewing rendered ‘mental maps’ of the US by sundry New York City residents (the displayed ignorance of the larger world, sadly, not exclusive to NYC folk by any means…). Worth a look, along with more contemporary exercises depicting planetary views…

may we all find a better day.

may we all

As a resident of Idaho, there is no way houses in Moscow, ID are that cheap.

Wolf , if they cut the rate then wouldn’t housing prices go over the roof even when the house prices are already ridiculously high?

No, because mortgage rates run above the 10-year Treasury yield. The Fed’s policy rates are short-term rates, which are irrelevant for mortgage rates. QT pushes up long-term rates. The Fed can cut its policy rates to 4.5% and continue QT and push the 10-year yield to 5.5% and mortgage rates to 8%, no problem.

Come to Cuba. I can have a friend buy a nice 2 bedroom apt furnished for $5k USD. Then visit,6 months on a tourist visa free and add a family and friends visa for $24 usd every 90 days to be 100% legal.

My city, I live in a 24 hour power area, avg meal, etc is 1/5th USA prices.

Drawbacks? Hardly any medicine though medical care is top notch. Internet ok, super safe like anyplace if you know the area.

Shocked more web workers don’t come for the winter and live all in with rent included in a small city close to airports, 2 hours from ocean for all in$400usd a month..rent, food, transportation, minor entertainment, meals out.

Really.

@Wolf

Thanks that’s a great little concise explanation for exactly how QT plays into the mortgage rates. Easily misunderstood from all the noise in the media about it.

I respectfully disagree with the scenario that you suggested above, ie;

The Fed heads may continue to treat inflation as a nuisance rather than economic disease it is.

All of the asset bubbles that caused the inflation in the first place are fully inflated. How can the Fed heads say that monetary conditions are restrictive.

On the other hand, inflation is fully anchored and the timidity of the Fed is the reason.

They have no choice but to chase inflation that QE wrought. I’m not sure that 10 pct corporate A rated cost of borrowing is out of the question.

They need to increase the FFR as a first step to gain control of the inflation that the Fed caused. Get their thumb off the yield curve and reintroduce American business to competition. After their positions in China became untenable. And now they want too come home. God bless em

Take the Fed’s self authored acceptable inflation rate ..2%

Multiply it by the years we have had this inflation surge…..2.5 yrs

That’s around 5% sans compounding.

Even by the under stated metrics the govt uses, inflation for that period is circa 17%.

That’s about a 12% overshoot….

Yet victory will be declared if the YOY rate returns to 2%.

But what of the “over shoot” of prices? Baked in and never discussed.

Oh for some honest questioning of Powell at these hearings.

@dang I agree. And as Wolf points out – it isn’t inflation that is the danger… it is expectations of inflation that is the danger. People start building inflation into their budgets, into pay expectations, into bid quotes, and the next thing you inflation is no longer a logical thing – it becomes emotional and self-fulfilling. The Fed moved so slowly to try to tamp down inflationary expectations it was almost as if they were saying “ok, we’ll move, but only after we ensure that all of the inflation of the last two years is baked into the economic record and becomes part of pricing momentum moving forward”. It isn’t an asset bubble if it never pops.

In my view those MBS are coming off very slowly. Even more so with these rates. I wish they fast tracked them somehow.

MBS will come off faster when home sales pick up pace which is when the price drops become larger. Right now home sales are slow so the MBS stay on the books til they mature instead…

SeattleTechie,

Mortgage rates are already near 8%, thanks to QT. What else do you want? The housing market is already frozen. It’s like turning your freezer from -10℉ to -20℉. It doesn’t alter the food in the freezer; it’s already in deep-freeze status. I’m not sure if this was the worst analogy ever, but you get the idea.

Z33,

MBS won’t stay on the books till they mature. The pass-through principal payments at $20 billion a month = $240 billion a year would theoretically get rid of them in 10 years; but MBS get called when the pool of underlying mortgages has shrunk enough, and the remaining old mortgages get repackaged into new MBS. So this roll-off will take down most of the MBS in something like 7 years even without the Fed cutting rates. If the Fed cuts its rates, pass-through principal payments will turn into a torrent, and those MBS will fly off the shelf.

Thank you! I incorrectly left out the pass-through payments. The part of repackaging is good to know as well. Thanks for the article and comments’ section reply.

“It’s like turning your freezer from -10℉ to -20℉. It doesn’t alter the food in the freezer; it’s already in deep-freeze status. ”

Law of diminishing returns.

I’m not siding with Wolf…just pointing this out.

Thanks WR

I think it was criminal for Fed to keep buying mbs even though housing market was on fire.

I am sure it was done deliberately by fed to keep their assets elevated.

This has absolutely nothing to do with the FED’s balance sheet, but as someone who is half heartedly looking for a house to buy in a market that has shown somewhat modest declines (Las Vegas), I have been surprised at a recent uptick in foreclosures on the market.

I was surprised because I knee that there were lots of people who were “trapped” in 3% mortgages, but were likely not underwater (the price drop has been modest).

The only theory I can come up with is that 3-5 years ago a bunch of people signed ARMs whose rates are now coming due for adjustment and they cannot afford the new payments after they have been adjusted to new rates. So their houses are being foreclosed on. There are many people who stupidly thought rates would stay low forever so why would they take an ARM and get a really low rate?

I don’t know what this means for future house prices, but I do think it is a source of houses coming on to market. I don’t think it is a huge number of houses, but I do think it will make a difference (drop) in the price of houses because like anything else, housing prices are set on the margins and these are desperate sellers.

But a cut in the FFR wouldn’t turn MBS principal passthrough into a torrent, right? It would take a drop in *mortgage* rates to do that, which QT itself is preventing.

Why? Don’t you like all of America getting rich based on fake price of their houses. Let the illusion continue.

Nobody is getting rich. Its the illusion of being rich. If they sell, they will have to buy equally or more expensive house.

And if they had a mortgage at low %, forget it…

Wrong. They cash out hugely when they downsize or rent. Consider it a funded retirement, courtesy of the Fed, which has stolen the wealth from younger generations.

how much of the decline is just the reduced value of the fed’s holdings of low coupon paper? i assume they are showing the current market value, not the face value of their inventory.

Zero. The Fed doesn’t mark to market its Treasury holdings and its MBS.

Instead it discloses its unrealized losses in a footnote (a table actually) on its quarterly financial statement, like all banks do. At the end of Q2, it showed $1.08 in cumulative unrealized losses. Its entire portfolio of securities was valued at market at $7.35 trillion. So that was Q2.

By the end of Q3 (now), the market value of its portfolio might have dropped below $7 trillion on this additional QT, and on the additional losses on its bond holdings.

But it will hold those bonds to maturity, when it will get face value, so it doesn’t matter to the Fed, and there won’t be an actual loss. And the Fed (which creates and destroys money on a daily basis) can never run out of money and can never become illiquid or insolvent.

Hi wolf,

I am just thinking a little bit in future. At these yields at the long end of the curve, I am sure a credit event is going to hit sooner rather than later. May be bank crisis 2.0 is already in progress. When that happens, yields and rates drop, probably for good. At that moment, it is the trickling MBS that keep mortgage rates high. May be they will roll off faster then, but I don’t think that is enough to keep it at 8 percent then.

Seattle

Remarkable that with the 10yr at 3.7% there were banks on the ropes….

but now with the 10yr approaching 5%….zip.

It would be reasonable to assume there are some big things being kept under the rug.

Yellen’s decree to cover all deposits set a very far reaching precedent……perhaps the largest move in our financial history decided how, exactly?

“And the Fed (which creates and destroys money on a daily basis) can never run out of money and can never become illiquid or insolvent.”

Move over Jesus, we have a new savior in town called Jerome…HA

One of my brain minions says “Tell me more!”, another says “This seems to good to be true”. Thus why I have to turn off my brain minions most of the time to invest with any success in the stock markets…as it all just seems too good to be true most of the time…

The lending conditions are again approaching a level where something in the financial system must break. We don’t know what will break (the weaknesses are hard to know) and we don’t know what the Fed will do, but it’s coming soon.

High-yield is still on cloud 9. Junk bonds and leveraged loans both. That’s the weak underbelly of corporate lending, and in this area, the financial conditions have remained loose. Look at the BB spread. It’s at 3 percentage points. During the best of times, it was 2.5. During the Financial Crisis, it went to 15!

I will buy 100 Wolf Beer Mugs if at the next crisis whatever they decree it to be , Fed doesn’t go berserk again and increases its balance sheet to above 10 trillion.

You’re counting on another pandemic, and on another monetary overreaction to a pandemic. There has been only one in my lifetime so far, and I date back a bunch of decades 😎. And if there is ever a second pandemic in my lifetime, there likely will not be another monetary overreaction like this because by now everyone can see what that did: unleashing the long-contained furies of inflation that will take a long time and a lot of wealth destruction to get back into the bottle.

They will totally double it to $16-18 Tril. Wolf beer mugs will be going for $300 for uncirculated item. The original – $500, if you can find it.

You need to look at the March bank panic for inspiration: they continued hiking their rates, they continued QT, and they threw $400 billion in short-term liquidity at the banks that they then withdrew within two months. That’s how they used to do it before QE. That’s what they did after 9/11. That’s what the BoE did last September when the gilt market went haywire due to the pension funds blowing up. And it worked fine, and everyone saw that it worked fine. And now that’s their new old model again.

Weren’t you, andy, one of the QE-mongers around here in March, saying that QE had started all over again, and to the moon? I explained to you what the Fed was doing — short-term liquidity as QT continues — and you pooh-poohed it. Are you gonna pooh-pooh it next time too? 🤣

I was bailout-monger 😂

We have leaders that “solve” problems only one way – printing money. That is self-evident.

There does seem to be a tacit promise to bail out people who “matter.” What was the significance of the quarter million dollar limit?

I think they canceled that limit thru precedent. Unless one lives in Oklahoma or something.

Unlike Sumner, who would say inflation would come down because base money has come down, Alan Blinder would say that because oil is coming down, so will inflation.

Blinder is *obviously* correct here.

Until such time as we find ourselves billed for the very Oxygen we breathe (don’t rule it out) – it’s hard to identify a commodity more basic to supply chains than oil.

BigAl – freshwater…

may we all find a better day.

Assets cannot be less than liabilities.

QT is woefully inadequate but this truth prevails. Even if it were faster, there is a limit.

With the Fed, they can. They simply make up an asset (“deferred asset”) equal in size to their losses. Voila.

I did not see that one in Wolf’s reporting.

“They simply make up an asset (“deferred asset”) equal in size to their losses.

Incorrect: they don’t “make up an asset,” that account is a LIABILITY (the amount the Fed owes the Treasury) with a negative value. Read my article linked below; it explains this.

“I did not see that one in Wolf’s reporting.

Just because you didn’t see it doesn’t mean I didn’t write it, LOL. Here is one of them, including charts, and great explanations too, so you don’t need to post this kind of nonsense again:

https://wolfstreet.com/2023/09/18/feds-cumulative-operating-losses-exceed-100-billion-rate-of-weekly-losses-begins-to-slow-as-qt-drains-rrps-and-reserves/

Saying you did not see it so it didn’t happen is a terrible way to argue. You are making an argument from ignorance. Your problem is that it requires you to ignore something that is obvious.

Willful ignorance is even a worse form of argument because not only is it often wrong, it makes the person making it look silly for willfully ignoring the obvious.

Hi Wolf! Great article. Curious if you will give your analysis on this “Greedflation” that is appear in MSM (NPR, Forbes, The Hill, etc). I would love your take from a financial perspective. I am curious over the Pepsi, Co example. I look forward to your insight! Thanks.

I cancel subscriptions to, or stop reading publications that use that clickbait term.

We have inflation because companies raise their prices, by definition, and because consumers and other companies are willing and able to pay those prices, by definition. It takes those two.

If consumers refuse to pay those prices and go on buyers’ strike, inflation is over. So what caused consumers to suddenly trample over each other to buy new and used vehicles at ridiculous prices when most of them could have just as well driven what they already had? The “inflationary mindset” when consumers and businesses pay whatever.

How do you beat this “inflationary mindset” out of consumers and businesses? You push up interest rates until they trigger a deep enough a recession that forces laid off consumers to spend less and watch what they spend, and it forces struggling businesses to cut their expenses and watch what they spend.

The risk is that you get this recession, and inflation doesn’t go away because consumers and businesses have gotten used to it and have adjusted to it. And then you need to trigger an even deeper recession (see Volcker).

“If consumers refuse to pay those prices and go on buyers’ strike, inflation is over”

Yes, for anything that is not required for survival. Not the case for energy, housing, and food. Especially considering how much food and energy is already subsidized.

You shift and substitute between companies. If this company raises prices, you switch to another, and if EVERYONE does this (= buyers’ strike) then that company doesn’t get away with raising prices because its sales collapse. “Food” is not one thing. It’s made up a gazillion products sold by a gazillion companies — it is very competitive normally, and you can switch to different stores and different products. When a landlord wants to increase rent by 10%, ALL tenants need to move out or threaten to move out (= buyers strike), and the landlord will default on his mortgage. You can do this with gas stations. You can do it with everything where there is some competition. The only thing you cannot do it with are your regulated utilities (electricity, gas, water). But you can do it with broadband (I do every few years).

Buyers’ strikes — and consumers — are very powerful, and that’s the ONLY thing that keeps companies from jacking up prices. When consumers abandon those efforts and just bend over, inflation surges because companies get away with big price increases.

And then there are quasi monopolies, like the meatpacking industry.

Yes, that’s a problem, and the government needs to do its job. It has abrogated that job many years ago. So that problem existed long before this bout of inflation.

I always laugh when people say “Greedy companies charge as much as they can to pad their profits!” as if that’s some profound discovery.

No sh*t sherlocks! That’s what all businesses do, from the largest S&P 500 companies down to the barber or solo plumber.

Amazon is sued by feds for raising prices so looks like somebody thinks free market is criminal. I don’t have to buy anything at all from Amazon.

Services inflation is out of control. Quotes for labor to stain my modest house were over $4,000. That’s before the cost of materials, which are half that amount. My solution? I’m doing it myself! I bought a nice airless sprayer for a few hundred bucks, and I’ll rent a bucket lift to get the higher parts of my house for another few hundred bucks, and now I have the tools and knowhow to do it again in a few years.

Wolf,

A few years ago I would have *absolutely* agreed with you 100% about how to combat inflation.

Now? I’m not so sure. Most businesses are far more leveraged than they were in Volcker’s time and I fear that there is a real possibility that increased financing costs not only are at risk at becoming a pass-through expense to customers…they may also dissuade productive investment in the real economy.

It is fascinating to see how much easier it’s been for non-financialized economies like Mexico and Brazil to control inflation with rate hikes than the so-called “advanced” economies.

Businesses are leveraged because they have had access to under-3% money for so long. Using borrowed money to reduce corporate stock (buybacks) is what most of them have done in the past decade. Corporate finance guys aren’t stupid… a profitable company has two sources of capital… stock shares or debt. Stockholders want an ever-bigger portion of the profits… but bond holders can only get the percentage they agreed to. Now that the party is over they will switch back to selling shares of the company when they need to raise capital.

Frankly we should ALL have followed their lead in the past ten years. Load up on nearly zero-interest debt and trust that in the future we will have the means to pay it off with inflated dollars.

What % of the Fed’s balance sheet are TIPS?

When CPI inevitably re-accelerates later this year, those TIPS will presumably see the inflation premium that gets added to their principal go up as well.

Tips are not an attractive investment, In My Opinion. They are long term investments that pay a paltry return above inflation.

MM,

The Fed holds $365 billion in TIPS plus $111 billion in accumulated inflation compensation (added to the principal) for a total of $476 billion in TIPS. That’s about 6% of its total assets.

That difference between the $58 billion or $59 billion roll-off every month and the $60 billion cap is the inflation compensation.

Thanks Wolf. Sounds like that inflation compensation is a miniscule % of the overall balance sheet.

I disagree. Tips can be had that are 2% or more above inflation. For parking some of your money in safe options, inflation plus 2% is a pretty nifty deal. It even keeps your money above inflation after you pay taxes. The money doesn’t loose purchasing power. It probably even gains a little on a very safe investment.

Now it probably does not match stock returns long term, but for a portion of what you own to safely gain a little that is pretty attractive.

For individuals, I think series I bonds are a better asset to hold for long term savings/inflation protection.

When looking at your next to last graph, Discount Window loans and BTFP loans, is that showing loans made each week, or the loans outstanding (in other words, total amount currently being borrowed). Loans outstanding would be more interesting to me. As you say, banks can borrow from BTFP for up to one year, so weekly activity is of less interest to me than the total amount currently being borrowed. Sorry if this is a dumb question. I did RTGDFA, but maybe missed it.

It’s Loans Outstanding.

Wolf: The FED has no history, business and probably authority to buy anything except Treasury securities. They intentionally influenced and subsidized the real estate industry buying MBS. Inappropriate.

Next, the FED in monetizing the annual deficits have allowed the flakes in Congress to avoid reality. Make them raise taxes or cut spending. They have indirectly allowed weak politicians to create the national debt.

Politicians are now weak, no backbone people. Make voters happy by saying yes,yes,yes. FED should say no. Markets are starting to say no. The ELITE are still controlling the politicians to shit on American society. It’s a uniparty. The puppeteers are laughing as they control the strings to the politicians. They love political fights over irrelevant issues and giggle as the masses and the sheep constantly fight 50-50 over nonsense .. all while we blow up USA.

Wolf.. you are bright. You have big picture knowledge. Direct your readers to want is happening.

It definitely is a dysfunctional system that, at the same time, seems to crush a segment of the population while funding the offshoring movement with zero percent interest rates to build their Chinese factories.

This is not a political (or any) advocacy website.

Countrybanker

All true.

“.They intentionally influenced and subsidized the real estate industry buying MBS. Inappropriate.”

That is probably the biggest “bad move” the Fed has made. One must ask “Why?” and “Who was the great beneficiary?”. (Who had the Fed’s “ear”?) I have my thoughts.

Former Fed Pres Fisher admitted that the Fed pushed long rates down (all time lows) to “Force” the investor to take more risk. A curious mission, IMO. A dangerous power hungry disregard for free markets and normal risk return considerations.

I don’t totally agree. They have no business buying treasury securities on a permanent basis either.

Since residential MBS is largely government guaranteed, I’m having a hard time seeing a philosophical distinction between buying treasuries and buying agency MBS.

The problem is not that the Fed bought MBS specifically. The problem is that the Fed is buying any securities for QE and that Congress guaranteed mortgages in the first place.

Well there must have been a pretty good reason that for decades they never touched mortgage backed securities.

Are they Treasury backed? Guessing no. And I believe there is a distinction ….the Fed is only (allegedly) to deal in Treasury backed issues. (they went off the rails in 2009)

I agree with your final comments.

It is fine that the Fed is the lender of last resort for banks, and that they can tweak liquidity and rates here and there, but to expand the money supply by 38% , so rapidly , is overboard, IMO.

“They intentionally influenced and subsidized the real estate industry buying MBS”.

No. That was Fannie and Freddie. You can blame the Fed for a lot of things, but not for that. They just mopped up the mess afterwards.

If you are unable to see the difference between political parties, that relect more on you that it does the political parties.

Also, the biggest weakness of democracy is that it requires informed voters. Unfortunately it seems like nowadays there is a large percentage of voters who are not informed. Not only are they uninformed, they are deluded. For example, they are not informed enough to tell the difference between political parties. They get distracted by shiny things and miss the important differences.

If RRPs dropped $220B between the 1st business day of Sept and the 1st business day of Oct, doesn’t that offset the $146B drop in assets during the month of Sept?

No, it’s not that simple. There were shifts on the liability side too. For example, the TGA (Government checking account) jumped $200 billion over the same period. Both RRPs and TGA are liabilities. They sort of balance each other out.

1) Eight months ago, in Mar 2023, the regional banks lurched lower. Some flipped in Feb 2023.

2) In Apr and in May total borrowing from the Discount Window and from

BTFP reached $160B. In Oct the total is $110B, down $50B, a tiny portion of commercial banks total assets.

3) CDs in commercial banks and MM accounts are growing. Stock market investors who cashed in parked their money in CDs. Boomers who sold expensive houses and moved to other areas parked their money in CDs. The front end of the yield curve is loaded. The bottom of the hump is shifting to the left. It will drag the long duration down.

4) The strike pandemic is growing. Working people have no money in

their bank account by the end of the month, while the upper middle

class and the rich can’t stop spending.

5) In a few years the labor force might be growing. Gen Z is moving in. The prime age, the black market, the sticky boomers who refuse to retire, new immigrants packed in one room like sardines, Ukraine women and children… The total might approach 200M. Add AI, bankruptcies and gov shutdown to the mix ==> deflation.

6) In recessions the saving rate is growing. The upper middle class and

the rich stop spending. The poor stay poor, become poorer.

Regarding #3: Your point about CDs is very timely….but the interpretation is questionable.

Special CD rates from 6-18 months collapsed by about 100-125 BP around Boston this past week. Obviously, banks are comfortable with the amount of deposits they have. But I think their motivation is that they are becoming scared to lend due to the rising prospect of loan non-performance.

Regarding #6:

“In recessions the saving rate is growing”.

Not during stagflation it isn’t.

Thanks Wolf, let’s all hope The Fed continues it’s QT. Mish Talk did a nice job of outlining the current situation in real estate. The bottom line is that the Fed knows very well that it has blown another real estate bubble. Also, remember that housing, energy, and food “don’t count” in the Fed’s analysis of inflation, something that we all know is complete BS. In my opinion, the Fed knows that this is BS, and they are doing their best to send a strong message to congress that fiscal policy must get in line with monetary policy. Just my two cents.

Politics get interesting now. Interesting times gentlemen, hedge accordingly.

“Also, remember that housing, energy, and food “don’t count” in the Fed’s analysis of inflation,”

That’s very wrong. The Fed looks at all measures of inflation. But when it gauges “underlying inflation” – inflation entrenched in the economy – it looks at measures that eliminate the volatile components of food and energy. For example, energy prices started plunging in mid-2022, and overall inflation measures came down a lot because of it, and the Fed ignored that, rather than saying, “See, inflation is vanquished.” Only the morons in the news media got fogged over by the plunge in energy prices and said inflation was “vanquished” when energy prices plunged, while the Fed kept harping on underlying inflation and services inflation still raging. The Fed never excludes housing, but it also wants to see services inflation beyond housing.

If the Fed were to send a strong message to congress that its fiscal policy must get in line with monetary policy…the independence of that institution would be at an end.

The Fed tightening has had no obvious effect on calming the housing prices. If the situation in Metro Boston is indeed indicative of the rest of the country…then that is nothing to marvel at because the buying is mostly being done by pockets of institutional investors who are doing their buying with unalloyed cash. Credit? No thanks, PPP funds and capital gains were enough for us, thank you. As I correctly predicted two years ago – the current housing market can get by quite nicely on a few (very) well-heeled buyers.

I am having a drink(coffee) to celebrate breaking below 8,000,000,000,000. Yay. I knew they could do it.

Thanks for the great insight.

Question: Is it the amount of injected liquidity that is restrictive/expansionary or is the change in the amount of injected liquidity?

In other words, when QT eventually stops (and presumable doesn’t become QE), will its associated monetary policy then be “neutral” because money is no longer being added or removed from the economy, or will it still be “restrictive” because the outstanding balance in the economy is low?

Hello,

I am studying in collage and bit confused. What is the impact on Stock market with this article?

Please share the knowledge.

Thanks/

You can listen to my podcast, which discusses precisely your question, and which I linked at the bottom of the article. Here it is again:

https://wolfstreet.com/2023/10/01/the-wolf-street-report-stocks-bonds-cre-face-qt/

VJ – am guessing that you are not a student at a US or Anglophone ‘college’ (of course, it may be a typo, or you may be majoring in art and looking for advice on investing your works’ future profits…). If you are at an Anglophone institution, for your own long-term benefit, please take an English 101 refresher (gawd knows it’s a difficult language. I’ve never mastered it and I’m a native speaker…). -best.

may we all find a better day.

Labor report burning hot………that recession is around here somewhere……anybody see it?…….now who misplace the recession?

In Eccles its total caution while the wild rabbits decide their next policy move……..should they make another bold move of a quarter point or sleep til noon. Pass the port.

My hypothesis is that boomers continue to retire at an increasing rate, and this, at least in part is explaining some of the labor shortage. In addition, due to QE and ZIRP for almost 15 years, we have had massive capital misallocation and malinvestment (massive speculation). The latter means energy, food, housing (basically anything you need for survival) is going to continue to get expensive.

I guess we should have been investing that free money in developing fusion reactors and/or bringing new energy options online instead of developing a million different crypto “currencies”… LOL.

The real economy requires tremendous energy inputs to keep it going.

Interesting times…

WB….it’s very complicated with the boomers and millennials but…….everything you stated is right on. Short term anything can happen….especially as rates jump higher but long term…..the boomers will be putting pressure on costs because they produce nothing and are going to hog the medical systems and other things like travel. Their retirements are also going to pressure inflation because as the most experienced workers productivity is going to suffer. Meanwhile the millennials are going to become more productive but it will take time…..and their earnings are just starting to take off. Lots of demand in the pipeline due to both these huge generations but the fed continues to believe we have a lack of demand…..which is just plain incompetence.

That. was from 2006 to 2022…..it’s the opposite problem now……but the idiots don’t see it with all their degrees.

Fusion reaction ain’t coming to save us.

Even if the USA does manage to produce more hydrocarbons in the coming years…it’s going to have to export a larger (potentially *much* large) percentage of them to stay solvent.

It will become politically impossible to continue to export those hydrocarbons in short order.

Again, interesting times.

Wolf, you stated “The Fed’s policy rates are short-term rates”.

This is past tense guidance. The reason the Fed is doing substantial QT is to manipulate long term rates higher.

And there are other reasons, besides inflation, for driving long term rates higher for longer.

///

Dear FED,

please stop stress eating every time there is a crisis. Let the dice roll, keep an eye on the situation and stop intervening.

By the way, I like your diet…Keep it up.

Yours truly

///

Something that I think bears watching just occurred in Metro Boston.

This past Monday, about half of our banks (whether community, regional, or national) just lowered the rates on their promotional CDs by 100-125 basis points for the 6, 9, 12, 18 month durations.

That’s a whopper of a move in the absence of Fed action. And there is no other explanation I can think of other than banks aren’t looking for deposits because they are becoming scared to lend.

It will be interesting to see what the remaining banks do next Monday.

The only “higher for longer” that seems credible to me is the one that concerns the size of the Fed’s balance sheet.

If the FED reduces its balance sheet by 1T and the FED gov runs a 2T deficit, how do they effect each other?

Yields rise until there is sufficient demand. Yield solves all demand problems. High yields are the only discipline that might get Congress to take the deficits seriously.

Very good analysis.

QT minus 1 trillion, losses up 1 trillion.

End of story.

BS. what ignorant blogger out there is telling you this idiotic BS?

QT = $1 trillion

PLUS unrealized losses = $1 trillion

QT and unrealized losses = $2 trillion

Total assets after unrealized losses = $7.35 trillion, as per the Fed’s quarterly financial statement for Q2.

By now (Q3), total assets after unrealized losses will likely be below $7 trillion. So check the Fed’s Q3 financial statement when it comes out later this year.

Smattering of applause….

“Loans to FDIC: -$70 billion in September, to $64 billion”

Per the chart I think it was -$17 billion in September.

Each black dot is a week (weekly balance sheet). At the last balance sheet for August (released Sep 6), the balance was $133.7 billion. The Oct 4 balance sheet was $63.7 billion. Difference $70.1 billion.