Week Ahead – Focus on China GDP and US retail sales, more CPI data on tap

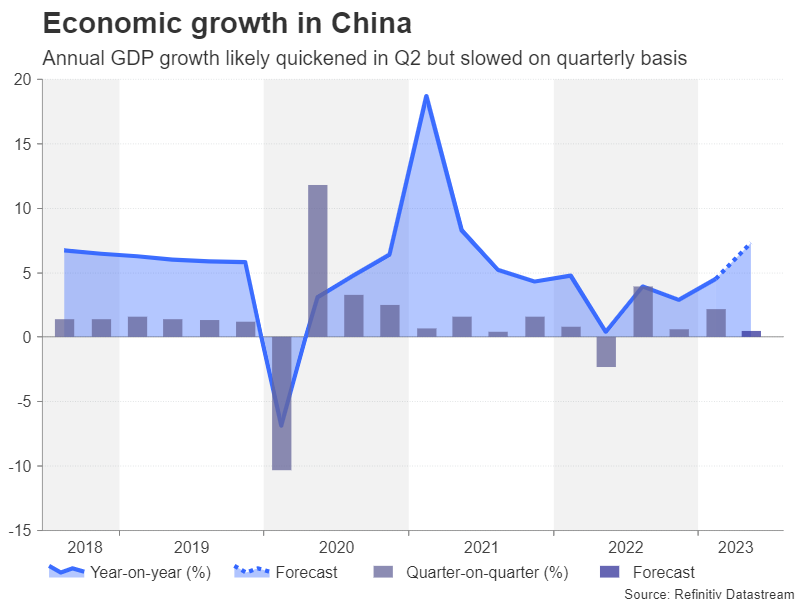

China is rarely out of the headlines these days amid persisting fears that the economic recovery is faltering and doubts about how far the government is willing to go to pump more stimulus. On Monday, when the second quarter GDP estimate is reported, investors will likely breathe a sigh of relief, at least initially.

The economy is expected to have expanded by 7.3% year-on-year, which would make it the fastest growth since the second quarter of 2021. However, GDP shrank in the same quarter of 2022 so this would flatter the annual comparison. Moreover, on a quarterly basis, growth is projected at just 0.5%, which is below China’s average and well below the pace that is needed to achieve yearly growth of around 5% that the government is aiming for.

The underlying weakness will also likely be on full display in the monthly prints on industrial output and retail sales. Industrial production growth is forecast to have slowed from 3.5% to 2.7% y/y in June, and retail sales from 12.7% to 3.2% y/y.

The elusive stimulusInvestors have become somewhat frustrated lately from the lack of policy response from Chinese authorities to tackle the slowdown. The measures announced so far have been very targeted and a large-scale stimulus does not appear to be on the cards. The People’s Bank of China cut its loan prime lending rates last month for the first time since August 2022, and even though it was only by 10 basis points, a further cut is not very probable when it meets again on Thursday.

The incremental steps to boost growth have failed to set markets alight, but the soft CPI report out of the United States has given investors something to cheer about. In light of that, a stronger-than-expected GDP reading could add fuel to the risk rally, whereas if it disappoints, risk-sensitive currencies such as the Australian dollar as well as equities could come under selling pressure.

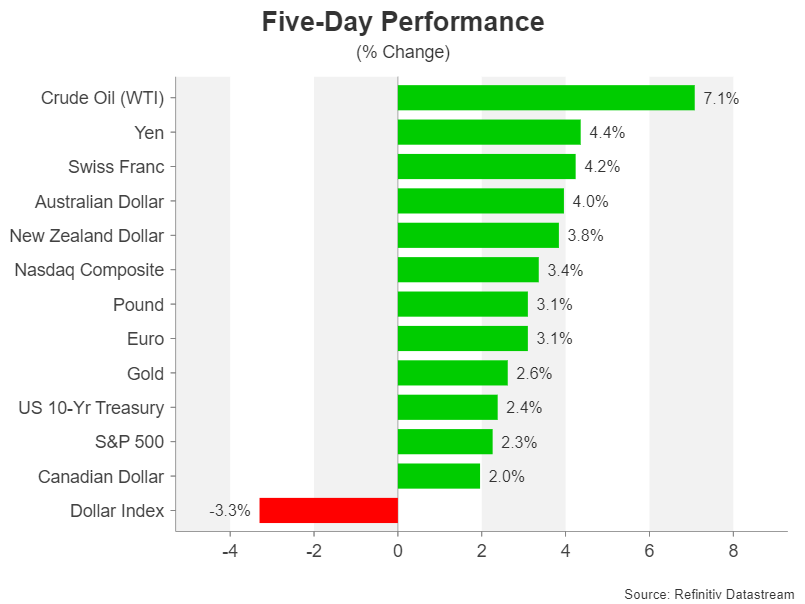

The aussie has already gained more than 4.0% in July so a lot is at stake if the US CPI-led euphoria evaporates. Aussie traders will also be watching domestic employment numbers on Thursday in addition to the minutes of the RBA’s July policy decision on Tuesday when the Bank went back into pause.

US data will have a hard time lifting the dollarA central bank that will likely ‘unpause’ at its next meeting is the Federal Reserve. There seems to be a strong consensus among Fed officials that some further tightening is still required. But after the downside surprise in CPI, markets are more convinced than ever that a July hike would be the last. More crucially, investors have ramped up their bets of aggressive rate cuts in 2024, hammering the US dollar in the process.

It’s therefore going to be tough for next week’s US releases to switch those expectations around, meaning the dollar’s woes might not lessen anytime soon.

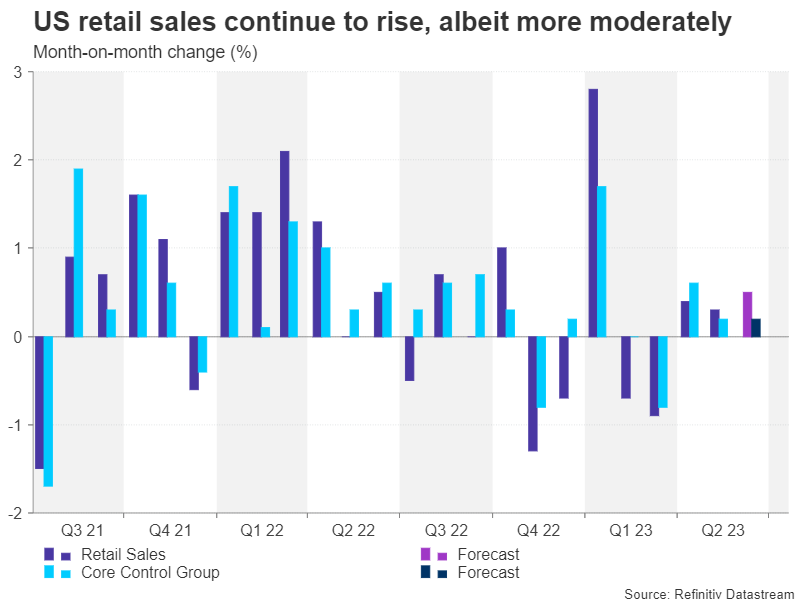

The data flurry will begin on Monday with the Empire State manufacturing index, followed by retail sales and industrial production on Tuesday. Growth in retail sales is expected to have quickened slightly to 0.5% month-on-month, suggesting consumer spending remains healthy while the summer season is in full swing.

Building permits and housing starts are due on Wednesday, with existing home sales coming up on Thursday, along with the Philly Fed manufacturing index. The US housing market is displaying some tentative signs of a recovery and a further indication of that next week might aid the greenback claw higher.

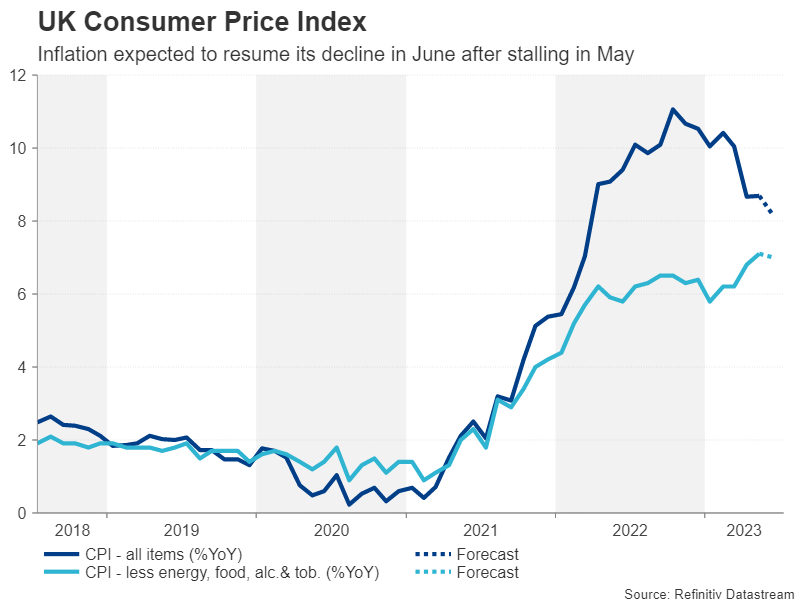

Will UK CPI resume its decline?One of the currencies riding high on the back of the dollar’s drubbing is the pound. The British currency has stormed above the $1.30 level for the first time since April 2022. However, the rally will be put to the test on Wednesday when the latest UK inflation figures are published.

The consumer price index has repeatedly beaten expectations this year, causing a headache for the Bank of England. The most striking feature of the UK’s stubbornly high inflation problem is that core CPI has yet to peak after almost 500 basis points of rate increases.

There might be some reprieve for policymakers, though, if inflation drops to 8.2% y/y in June as expected from 8.7% in the prior month. Core CPI is projected to moderate too, but only negligibly to 7.0% y/y.

Retail sales data due Friday will also be watched.

Having already jumped by over 3.0% in July alone, the pound is at risk of a sharp correction should the CPI numbers miss the forecasts for once. However, even in this scenario, sterling’s prospects would remain significantly more bullish than its peers’ as the Bank of England would still have a longer tightening path ahead of it than other big central banks like the Fed and ECB.

Japan, New Zealand and Canada awaiting CPI reports tooThe Reserve Bank of New Zealand kept its cash rate on hold at its July meeting, signalling that rates have likely peaked. The quarterly CPI readings out Wednesday are anticipated to support that decision as inflation is forecast to have fallen from 6.7% to 5.9% y/y in the three months to June.

But like the pound, the perked-up New Zealand dollar is in danger of a pullback should inflation decline more than expected.

The Bank of Canada on the other hand decided to raise interest rates this week and kept the door open to more. However, with inflation hitting a two-year low of 3.4% in May, investors are unsure if the BoC will hike again.

On Tuesday, the June CPI numbers are due and may stir things up for the Canadian dollar if BoC bets are blown in a particular direction.

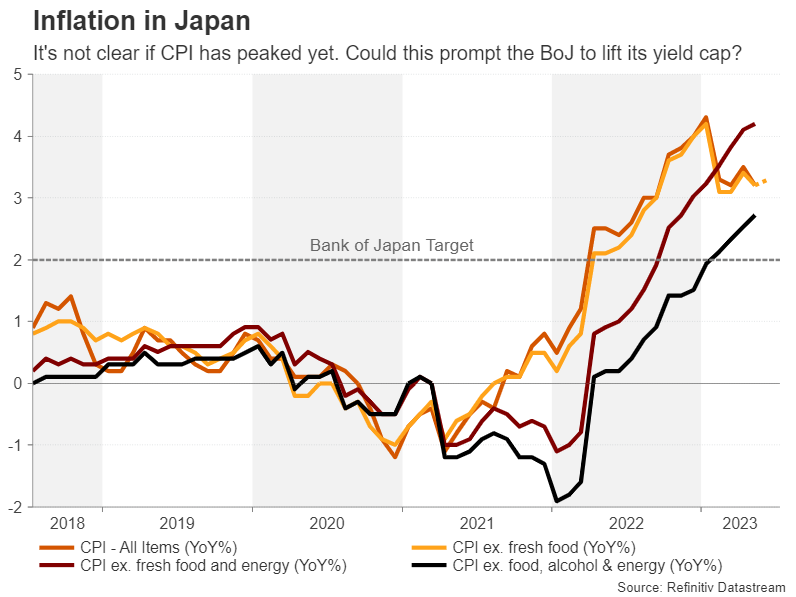

The inflation releases will wrap up on Friday in Japan where speculation is growing about a possible tweak in policy by the Bank of Japan. Friday’s data could be important in helping policymakers make up their minds if they should lift or remove the upper limit on the 10-year JGB yield.

Headline and core CPI appear to have plateaued in Japan but the so-called ‘core core’ rate continues to climb. Thus, any upside surprises in the June figures could fuel speculation of a July move, boosting the Japanese yen, which is having its best week since November last year.Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.