May RBNZ preview: Not enough reasons to turn dovish

The Reserve Bank of New Zealand has little room to shift to a less hawkish stance as non-tradeable inflation remained too hot in the first quarter, despite a domestic recession and loosening jobs market. We think rate projections will still signal no rate cuts in 2024, but we don’t rule out some easing in the fourth quarter

The Reserve Bank of New Zealand is widely expected to maintain the official cash rate (OCR) at 5.50% at the upcoming 22 May meeting, so the focus will be on new economic projections and forward-looking language.

The RBNZ differs from other developed central banks in that it announces policy less frequently and can only rely on quarterly inflation and jobs data, which can ultimately lead to rapid changes in policy direction from the RBNZ. However, the latest indications from the New Zealand economy and modest expectations for Fed easing (50bp by year-end) suggest the RBNZ should be in no rush to pivot to dovish communication.

Inflation remains too hot despite a slowing economy

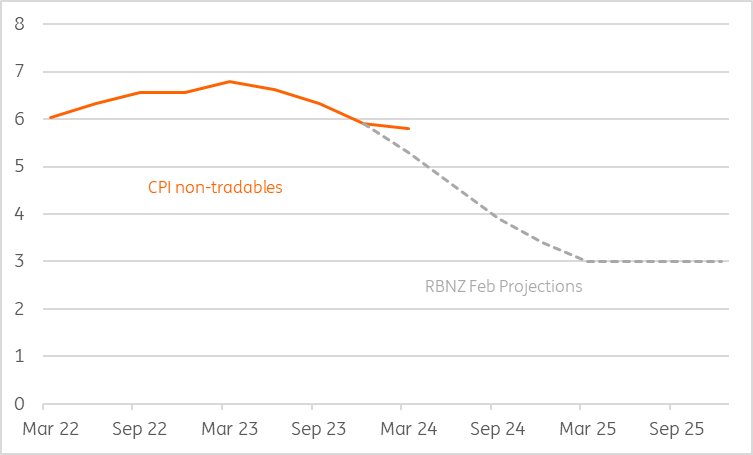

The resilience in non-tradeable inflation remains a key concern for the RBNZ: in the first quarter, it came in at 5.8% versus the RBNZ forecast of 5.3%. The headline rate was 4.0%, only slightly above the Bank’s 3.8% projections. Going forward, as the labour market starts to loosen, we expect headline inflation to fall in the second quarter to around 3.6% year-on-year. However, policymakers will watch the developments in non-tradeable inflation more closely, where there remain some upside risks.

Non-tradeable inflation overshooting projections

One key factor slowing the price deceleration could be incoming migration. Net immigration has risen substantially in NZ over the past couple of years, and while the RBNZ is still uncertain on its impact (upside pressure on demand and rents versus easing labour supply), we argued here that the risks may be skewed to the inflationary side. However, there are signs migration flows have slowed since the start of 2024.

While inflation remains too hot, growth and the jobs market have moved in the other direction. In the first quarter, the unemployment rate climbed to 4.3%, private wage growth slowed from 1.0% to 0.8% quarter-on-quarter, and the economy was in recession after GDP disappointed with a -0.1% QoQ. These economic developments do point to some disinflation ahead, but do not directly impact the RBNZ decisions after its remit was changed in December to only target inflation.

RBNZ should keep rate projections unchanged

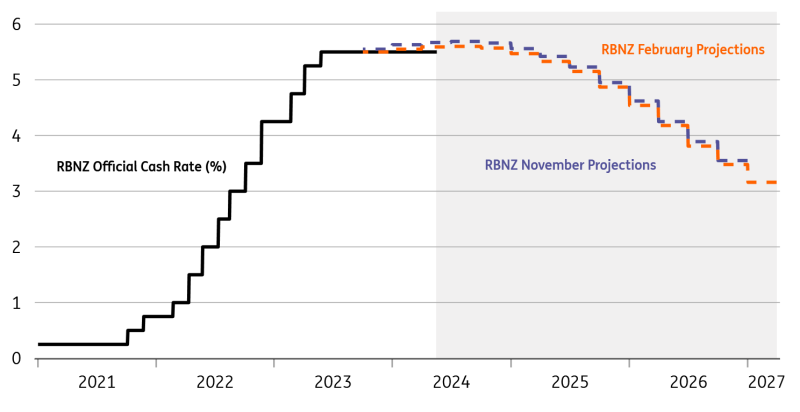

We think the RBNZ will remain hawkish in May, and leave the rate projection profile broadly unchanged. That would mean no rate cuts and a small chance of another hike in 2024, plus around 75bp of easing in 2025. In terms of forward guidance, we think the Bank will reiterate that “interest rates need to remain at a restrictive level for a sustained period to ensure annual consumer price inflation returns to the 1 to 3 percent target range”.

Looking ahead, we believe the RBNZ’s hope to see inflation back in the target range by year-end are justified, but given data lag and non-tradeable inflation risks, the chances of any cuts before the fourth quarter are slim. If we are right with our Fed call (75bp of easing in 2024), then one or two cuts by the RBNZ in 4Q (October and November meetings) are still a possibility.

Latest RBNZ rate projections point to no 2024 cuts

NZD may have jumped the gun, but RBNZ remains supportive

We do not expect a substantial market impact from the RBNZ May decision. The Kiwi dollar is the best performing currency since the start of May (+3.7%) thanks to its high sensitivity to lower USD yields and better risk sentiment, along with a domestic monetary policy outlook that still grants attractive carry.

If anything, a reiteration of a hawkish stance by the RBNZ can prompt some hawkish repricing in domestic rate expectations (47bp of easing priced in by November) and help NZD reinforce its strong position. The NZD curve should, however, remain highly influenced by Fed pricing in the foreseeable future, and crucially until new key data in New Zealand are released on 16 July (CPI) and 6 August (jobs report). There is another RBNZ meeting (10 July) before then.

The NZD/USD rally may have occurred a bit too early in our view, and there are risks that US data will not endorse another leg higher in high-beta currencies in the near term. However, the summer months remain a good window for NZD/USD to stage a new rally to 0.63 before the US election risk kicks.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more